As previously disclosed, in the fourth quarter of 2015 the company recorded a PDR associated with its 2016 individual commercial ACA‐compliant offerings. Historically, this business has reported a profit in the first quarter of the year due to the related benefit designs. Because the company continues to anticipate a loss associated with this business for the full year 2016, the seasonal earnings generated in 1Q 2016 are offset by an increase in the PDR, resulting in a higher benefit ratio year over year. This first quarter seasonality was anticipated as the company developed its estimate of the full‐year PDR recorded in the fourth quarter of 2015.

Financial results associated with the wind‐down of the non‐ACA compliant (legacy) business, including the related release of policy reserves, as well as indirect administrative costs associated with ACA‐compliant offerings are included in the company’s 1Q 2016 financial results.

A few weeks ago, I got a heads up that Virginia was the first state out of the gate with their 2017 Rate Request filings. There were some confusing numbers which took awhile to sort out, but once the dust settled, the overall weighted average rate hike requests for Virginia's entire ACA-compliant individual market came in at around 17.9%.

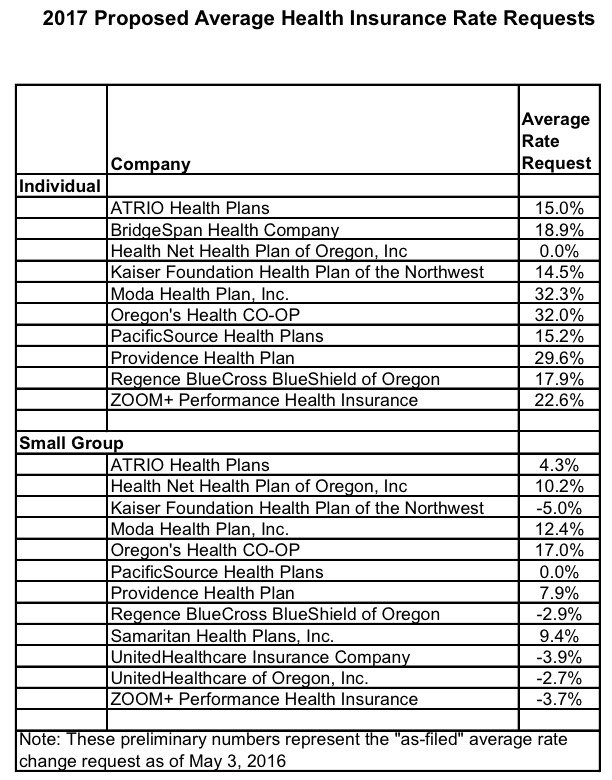

Some states make it next to impossible to track down this info. Others hand it to you on a silver plate. And then there are states like Oregon, who provide the average rate hike requests in a simple, easy format, but don't necessarily include the market share of those companies, making it difficult to compile a weighted average:

Back in January I noted that Moda Health Plans, which had plenty of self-inflicted wounds in addition to being kneecapped by the Risk Corridor Massacre, was dropping out of the Oregon exchange and likely the Alaska exchange as well, so today's news isn't a big surprise.

Even so, this is definitely a major problem for the Alaska individual market, which was already extremely expensive prior to the ACA and which now only has a single insurance carrier participating (h/t to Louise Norris):

The individual market in Alaska has just two carriers in 2016: Moda and Premera. Both have struggled with significant losses under the ACA, and Moda nearly exited the Alaska market altogether in late January (more details below).

Finally, on the Medicaid spreadsheet, I've gotten as close as possible to an accurate count of the number of new Medicaid/CHIP enrollees which are PURELY due to ACA Expansion. To achieve this number, I took the total number of new enrollees and first removed the 25 states which haven't expanded Medicaid at all. This leaves 26 states (including DC). Then, I used Washington State as a guideline for the split between "ACA Expansion Only" and "Out of the Woodwork" enrollees (ie, people who were previously eligible pre-ACA but didn't enroll until after October 1st for various reasons). Washington has had a pretty consistent ratio of 2/3 Expansion Only to 1/3 "Woodworkers". I have no idea if that's representative of the other 25 states, but it's the best I can do for now. Note that this still also includes those who are newly eligible...but under the old Medicaid rules (ie, someone who simply fell on hard times after October 1st).

After a year and a half of allowing the residents of Flint, Michigan to be poisoned, GOP Governor Rick Snyder, in response to growing public pressure, finally decided to do something decent for once:

Gov. Rick Snyder said Tuesday he will seek permission from the Obama administration to allow all young people in Flint the chance to receive publicly funded health care services for lead exposure amid the city's contaminated drinking water crisis.

...The White House and federal Department of Health and Human Services did not have an immediate response Tuesday to Snyder's initiative targeting Flint residents up to age 21 through the expansion of Medicaid.

Even then, he wasn't exactly in a big hurry to do so; he waited another 3 weeks to get around to actually submitting his request:

I was fascinated when I saw this phenomenon happen here in Michigan last year, but it's repeated itself in several other states since then. State and federal officials crunched their demographic data and came up with estimates of the maximum number of residents who they expected to be eligible for the ACA's Medicaid expansion provision a couple of years back, along with the number of those expected to enroll in the program in the first year. They're then caught offguard when not only does the actual number eligible turn out to be far higher than they expected, but far more of those eligible go ahead and sign up in the first year than expected.

In Michigan, estimates ranged from 477K - 500K being eligible; instead, the number broke 600,000 the first year, where it's hovered around ever since (as of last week it stood at 615,536).

A couple of days ago I noted that after two years of nothing but doom & gloom (and coming just a week after UnitedHealthcare pulled the plug on the individual market in over two dozen states) there seems to finally be some positive developments, with companies like Centene and Anthem reporting better-than-expected results. They may not be making a profit yet, but at least they aren't losing money hand over fist the way they did the first couple of years.

I also made a brief mention of the Maryland Co-Op, Evergreen Health, which reported their first quarterly profit since launching 2 1/2 years ago.

Consumer operated and oriented health plans in Maryland, New Mexico and Massachusetts will report profits in the first quarter, in a sign that some of the remaining Affordable Care Act-created nonprofits could be finding their footing on the state exchanges.

Thanks to Adam Cancryn for calling my attention to Molina's quarterly earnings report, which has this rather eye-opening section:

I've used Molina's Q1 2016 report, along with the Q4 2015 reports of Cigna and Humana, to further fill in the "Major Insurer" table I've been working on all this week; here's what it looks like now: