UnitedHealth Group Inc. plans to exit a third state Obamacare market as the insurer works to stem losses from its struggling Affordable Care Act business.

The insurer won’t sell policies through Michigan’s ACA exchange for next year, according to Andrea Miller, a spokeswoman for the state’s Department of Insurance and Financial Services. Georgia and Arkansas said last week that UnitedHealth will quit their exchanges for 2017.

...Fifteen insurers sold policies in the state for this year, U.S. data show.

Grandfathered Policies: These are non-ACA compliant policies which people were already enrolled in prior to March 2010, when the ACA was signed into law. Anyone enrolled in one of these can keep renewing them until the day they die if they wish (as long as they keep paying the premiums), or until the carrier chooses to (voluntarily) discontinue the policy.

Transitional (or "Grandmothered") Policies: These are non-ACA compliant policies which people enrolled in between March 2010 and October 2013. This category was created by President Obama and the HHS Dept. in November 2013 during the ugly "If You Like Your Plan You Can Keep It!" backlash. Basically, the ACA originally would have required that these policies be terminated as of 12/31/13. However, after a bunch of people received cancellation notices from their carrier, there was a massive backlash, leading Obama to announce an extension program.

The short version is that there were several extensions allowed, ultimately allowing insurance companies to keep these non-compliant "transitional" policies effective until as late as December 31st, 2017...depending on whether the state they operate in allowed the extensions, and if so, through what date. As a result, instead of all 5-6 million of these policies being cut off on 12/31/13, the cut-off date varies by state, by carrier and even by plan. Some states kept to the original 12/31/13 deadline; others bumped it out through the end of 2014, 2015, 2016 or took the full extension through 2017.

Don't ask me why, but I was thinking about the movie "A Few Good Men" this morning, and something has always bothered me about it.

As you'll recall, the reason Private First Class William Santiago was given the Code Red in the first place is because a) he broke the chain of command by begging everyone in the world to transfer him out of Guantanamo Bay, and b) he offered to squeal about the "fenceline incident" in return for the transfer.

OK, fair enough. But the scene which bothers me is the one above, which is also the introduction to Col. Jessup.

Here's my problem: As Jessup clearly states, PFC Santiago was, by all accounts, just a shitty Marine. He simply couldn't keep up with the training. Regardless of whether it was because of a legitimate medical condition or due to him "not being properly motivated", he couldn't hack it, end of story. Furthermore, no one liked him anyway.

Jessup doesn't want to transfer him because then he'd just be some other Colonel's problem, and he doesn't want to weaken the Marines by letting quality control slip. OK, I can accept that.

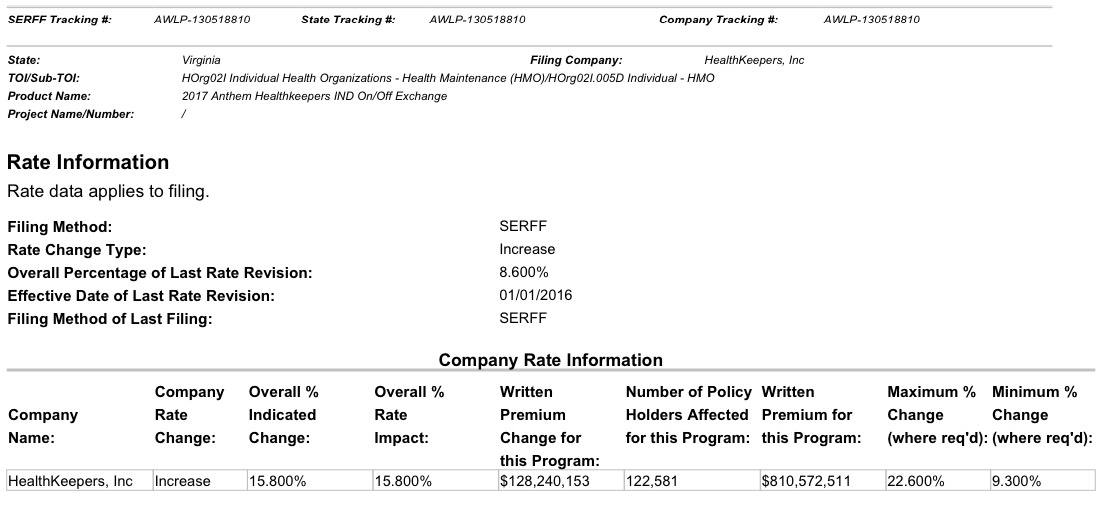

As you can see, while the requested rate increases stayed consistent throughout the various updates, the number of enrollees changed dramatically depending on which filing source I used. Case in point: Anthem/HealthKeepers Inc.

The first filing I found for Anthem HealthKeepers made it pretty clear that they're asking for a 15.8% average rate hike next year which is expected to potentially impact up to 122,581 policy holders:

Pretty cut & dry, right? Note that according to the filing that number covers current Anthem HealthKeepers enrollees both on and off the exchange, so it should cover all ACA-compliant policies.

In both cases, I've been criticized either here or via Twitter about the twin problems of high deductibles/co-pays and narrow networks. In response to the first story, people noted that the "actual" number who are uninsured is "a lot more" than 29 million because many people still can't afford the deductibles/co-pays or can't find a doctor/hospital in their network. In response to the second story, people claimed that I'm "hiding" the truth about how much policies cost for the same reasons.

In light of today's confirmation that the average 2016 premium rate increase ended up only being appx. 8% nationally on the individual market (as opposed to the headlines screaming about 40%, 50%, 60%+ rate hikes being "typical"), I've decided to get a jump on the 2017 rate changes. Someone gave me a heads up that Virginia appears to be first out of the gate this year, with requested 2017 rate filings having already been submitted by at least 8 carriers.

Now, for 2016 there are actually 13 carriers offering individual policies in Virginia (although some of these are available off-exchange only). I'm don't know if the 5 missing carriers have decided to drop out of the VA market or if they simply haven't submitted their 2017 filings yet (it looks like in Virginia the carriers technically have until July 15th to get their requests to the HHS Dept. in states which have their own rate review process, but the state itself presumably has an earlier deadline). It's also possible that some additional carriers might join the exchange and/or start offering policies in the state which don't this year.

In any event, here's what I've found so far for Virginia:

The 2016 rate-increase hysteria has already started. Before you freak out, here are four things to remember about premium-hike proposals.

May 15 officially marked the start of the 2016 rate review season. What that means for Americans is that over the next month or so, newspapers and web sites across the country will start running stories with scary-sounding headlines like this:

Some Oregonians could face major insurance rate hikes next year

Health plans request double-digit premium increases

...The articles will throw a bunch of numbers around, saying that the “average” premium rate increase for a given state is expected to be X percent, followed by examples of the highest and lowest increases. There may even be a few “Company Y will actually be reducing their rates!” thrown in.

Colorado lost their Co-Op...and CO is also one of only two states (Oregon is the other one) to drop their "transitional" policies as of the end of 2015. As a result, Colorado has a lot of people who could still potentially enroll by the end of February thanks to the 60-day Loss of Coverage Special Enrollment Period provision.

Louise Norris noted that there were around 39,000 ex-Co-Op members in Colorado (along with some others) who could still potentially enroll during February via the SEP option; I spitballed anywhere from 10,000 - 20,000 more Coloradoans might yet be added. There are also the normal SEPs for things like getting married, giving birth and so forth.