Missouri's final/approved avg. 2020 unsubsidized premium rate changes have finally been posted by CMS. For the most part they're following the same pattern as most other states this year with modest increases or decreases and a statewide weighted average decrease of 2.0% year over year. On average, unsubsidized ACA enrollees should pay about $13/month less next year than they are today.

However, what is noteworthy is that not one, not two but three new insurance carriers are entering the MO individual market this fall, bringing the total up to seven operating statewide: Cox Health Systems, Oscar Insurance (which was cofounded by Jared Kushner's brother, FWIW) and SSM Health Insurance.

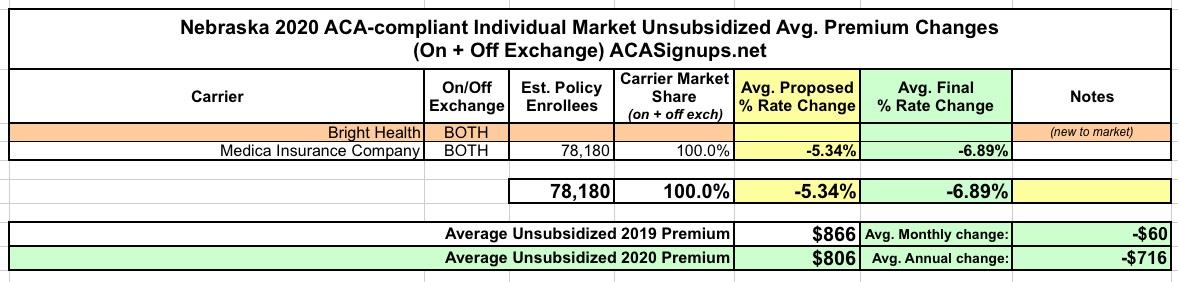

When I first ran the preliminary 2020 avg. rate hike numbers for Nebraska in August, the sole carrier offering ACA-compliant policies in the state (Medica) was planning on reducing their average premiums by 5.3%. Yesterday the final, approved rates were posted by CMS, and unsubsidized 2020 premiums will be even lower, by 6.9% on average.

For 2020, Bright Health is joining the Nebraska exchange.

I'm not sure how this happened, but it looks like I missed posting about South Dakota's requested 2020 premium rate filings. No matter, though, because the approved avg. rate increases (for unsubsidized enrollees) are exactly the same as what Avera Health Plan and Sanford Health Plan asked for anyway.

Statewide, South Dakota is looking at 6.5% average hikes for 2020.

Utah's final weighted average rate increase is a bit tricky. On the one hand, I have the hard enrollment numbers for three of the five carriers offering ACA-compliant individual market policies. On the other hand, I have no idea what the numbers are for the other two...both of which happen to have the lowest average rate drops in the state (BridgeSpan and Molina).

The weighted average of the other three carriers is a 2.3% reduction. Assuming the other two have, say, 20,000 enrollees apiece, that would knock it down another 1.5 points or so, but until I have a better idea of how many enrollees those carriers have I'll stick with the -2.3% figure.

Oklahoma has three carriers on the Individual Market these days. Once again, all three rate filing memos are redacted, but I was able to dig up the number of current policy holders for one of them (CommunityCare HMO).

The final/approved rate changes are exactly the same as the requested changes from a few months back, but I've managed to lock down the actual enrollment numbers for two of the three carriers. Assuming I'm close on the third one (Medica), the weighted average rate increase statewide should be around 2.7%:

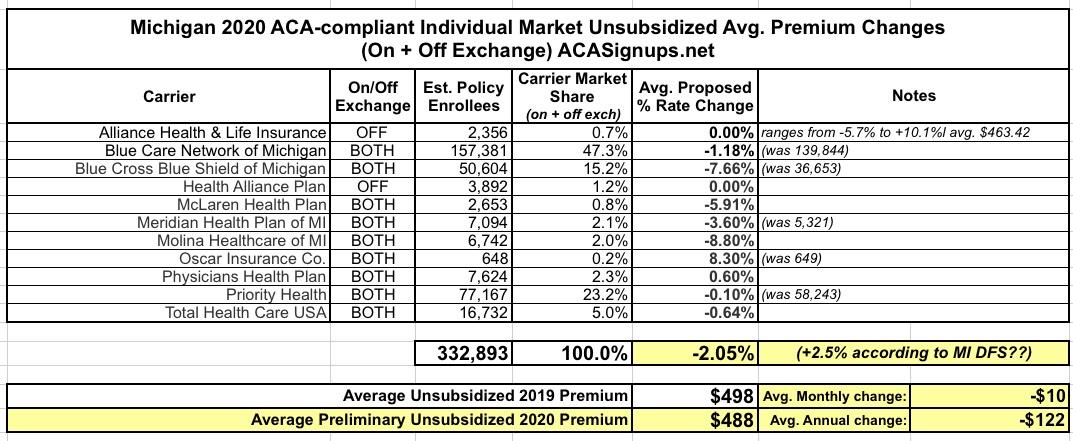

At the time, I concluded that the weighted average change marketwide was a 2.1% reduction in premiums compared to 2019, for around 333,000 Michiganders on the Indy market. This would mean roughly a $10 average premium reduction per unsubsidized enrollee per month, or $122 per year:

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has ten different carriers participating in the individual market. MA (along with Vermont and the District of Columbia) has merged their Individual and Small Group risk pools for premium setting purposes, so I'm not bothering breaking out the small group market in this case.

Getting a weighted average was a bit tricky. On the one hand, only one or two of the rate filings included actual enrollment data. On the other hand, the Massachusetts Health Connector puts out monthly enrollment reports which do break out the on-exchange numbers by carrier. This allowed me to run a rough breakout of on-exchange MA enrollment. I don't know whether the off-exchange portion has a similar ratio, but I have to assume it does for the moment.

There's only 3 states which are looking at double-digit average unsubsidized premium increases on the 2020 ACA individual market: Indiana, Vermont and Louisiana.

There's actually only 3 carriers offering individual market plans in Louisiana, but there's seven listings because two of the carriers have broken out their submissions into several different product lines. Overall, HMO LA, LA Health Service & Indemnity (Blue Cross Blue Shield of LA) and Vantage Health Plan are requesting average premium increases of 11.7% statewide.

I didn't have the actual enrollment data for the individual carriers when I ran the numbers for Kansas in August, so I had to go with an unweighted average unsubsidized 2020 premium rate change. At the time, that came in at a 3.1% reduction.

Since then, I've dug up the hard enrollment numbers, and just this morning CMS finally posted the final, approved 2020 rate changes. The weighted average comes in at a slight increase o 0.3% statewide:

When I ran the numbers for Iowa's preliminary avg. 2020 unsubsidized individual market rate changes, I had to use an unweighted average reduction of around 3.3%. However, knowing the relative market share of each carrier can make a big difference.

Case in point: It turns out that Medica holds something like 97% of Iowa's ACA-compliant market...whcih means the 11.3% rate drop by Medica heavily weighs the overall average. Wellmark is raising their rates by about 4.7%, but that only nudges the statewide weighted average to a 10.8% reduction overall.