Plan year 2026 health and dental insurance rate filings, as proposed, are available for the companies listed below. These filings are subject to actuarial review. Additional companies will be listed as their filings are received. Any insurance filings already approved are available to the public through the NAIC’s System for Electronic Rate and Form Filing (SERFF) interface. There is no fee for using SERFF. Rate info can also be accessed at the Rate Review page at Healthcare.gov

AmeriHealth Caritas VIP Next, Inc:

Company Legal Name AmeriHealth Caritas VIP Next, Inc.

Market for which proposed rates apply (Individual or Small Group) Individual

Total proposed rate change (increase/decrease) 46.20% increase

Effective date of proposed rate change January 1, 2026

This actually came out a couple of weeks ago but ironically, I've been too swamped analyzing & posting 2026 rate filings for other states to get around to posting it here until now.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Hawaii Medical Service Association:

Our requested rates include only the amounts needed to cover the expected health care benefits of our members, the cost of administering their benefits, expected Affordable Care Act (ACA) fees, and a small charge to help manage the risk of offering benefits to this population.

We based our rate increase request on a review of past costs of benefits and other expenses. These historical costs are adjusted for trend, to account for expected changes in use of medical services, cost inflation, and other factors that affect the cost of care. We also adjusted costs for benefit changes, which were largely made to comply with government mandated plan designs. Administrative expenses have been relatively flat over the past couple of years.

Rate Watch is a convenient way for Hoosiers to access key data on Accident and Health rate filings submitted to the IDOI on or after May 1, 2010. Use it to determine which companies have requested rate changes, their originally requested overall % rate change, and the overall final % rate change approved. These are overall rate changes and are not individually specific. The table below is searchable and sortable. You can also download your filtered results by pressing the Save Excel File button at the bottom of the table. If you need the full data set, including a few additional columns, you can download the CSV file.

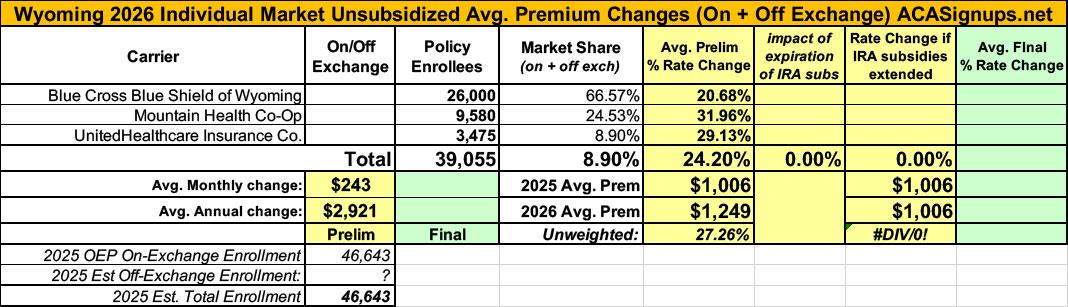

It was just a couple of weeks ago that the official (if preliminary) 2026 ACA individual market rate filings for Wyoming insurance carriers went live on the federal rate review website.

I published a writeup about these just 3 days ago; unlike some states, Wyoming was pretty easy to break out as they only have three carriers on the indy market, all of which also made their current enrollment data easy to find.

The landscape isn't pretty: BCBS is seeking average rate increases of 20.7%; UHC wants 29.1%, and Mountain Health Co-Op, which has around 9,600 enrollees, was asking for a whopping 32% average premium hike.

Keep in mind that Wyoming already has among the most expensive individual market policies in the country, with premiums averaging over $1,000/month.

Last winter, I initiated an ambitious project in which I generated graphics to illustrate just how much net ACA premiums are likely to increase starting on January 1st, 2026 (slightly over 5 months from today) assuming the enhanced premium subsidies provided by the Inflation Reduction Act over the past several years are allowed to expire.

This project took several months to complete, as I had to generate both tables and bar graphs for all 50 states (+DC), using 4 different households at multiple income brackets for each. All told, that's over 1,600 different examples.

I made sure to include various caveats for these projections. For instance, each of these examples assumes...

Insurance companies offering individual and small group health insurance plans are required to file proposed rates with the Arkansas Insurance Department for review and approval before plans can be sold to consumers.

The Department reviews rates to ensure that the plans are priced appropriately. Under Arkansas Law (Ark. Code Ann. § 23-79-110), the Commissioner shall disapprove a rate filing if he/she finds that the rate is not actuarially sound, is excessive, is inadequate, or is unfairly discriminatory.

The Department relies on outside actuarial analysis by a member of the American Academy of Actuaries to help determine whether a rate filing is sound.

Below, you can review information on the proposed rate filings for Plan Year 2026 individual and small group products that comply with the reforms of the Affordable Care Act.

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier: How many effectuated enrollees they have in ACA-compliant policies this year; the average projected rate change for those policies; and, ideally, a breakout of the rationale behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include:

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier: How many effectuated enrollees they have in ACA-compliant policies this year; the average projected rate change for those policies; and, ideally, a breakout of the rationale behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include: