Warning: This isn't just gonna get deeply wonky, it also requires digging deep into hisory. You've been warned.

Chapter 1: The (simplified) Backstory:

The ACA includes two types of financial subsidies: Advance Premium Tax Credits (APTC), which reduce monthly premiums; and Cost Sharing Reductions (CSR), which cut down on deductibles, co-pays & other out-of-pocket (OOP) expenses for low-income enrollees.

In 2014, then-Speaker of the House John Boehner filed a lawsuit on behalf of Congressional Republicans against the Obama Administration, in part because they claimed that CSR payments were unconstitutional because they weren't explicitly appropriated by Congress in the text of the Affordable Care Act.

A long legal process ensued, the end of which resulted in a federal judge ruling in the GOP's favor and ordering that CSR payments stop being made...but also staying that same order pending appeal of her decision by the Justice Department (then still run by the Obama Administration).

If you've been following my state-by-state 2026 avg. rate change project, you may have noticed that after filling in the final, approved rate filings for a bunch of states over the past month or so, these tapered off to just three more last week (Illinois, Washington and Connecticut).

The Connecticut Insurance Department has posted the initial proposed health insurance rate filings for the 2026 individual and small group markets. There are 8 filings made by 7 health insurers for plans that currently cover approximately 224,000 people (158,000 individual and 66,000 small group).

Anthem has filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange. ConnectiCare Benefits Inc. (CBI) and ConnectiCare Insurance Company, Inc. have filed rates for the individual market on the exchange.

Before I continue, note that yes, I'm aware the 17.8% average shown below doesn't match the 22.9% average in the headline above. There's a reason for this which should be obvious if you read on:

The 2026 rate proposals for the individual and small group market are on average higher than last year:

Last week I noted that Colorado legislators passed (and Gov. Polis signed) legislation to scrape together up to $100 million in emergency funding to backfill perhaps 40% or so of the federal tax credits the state expects their ~225,000 subsidized enrollees to lose in 2026 when the enhanced IRA credits expire this December:

...The Senate then approved House Bill 25B-1006, which would sell tax credits to bring in money for the Health Insurance Affordability Enterprise fund. That pays for programs to reduce individual insurance market premiums.

The bill aims to raise $100 million for that enterprise to soften the impact of the expiration of federal enhanced premium tax credits. Health insurance premiums for people who buy insurance on the individual market are expected to face an average of a 28% increase next year, with higher increases along the Western Slope.

OLYMPIA, Wash. — Fourteen health insurers have requested an average rate change of 21.2% for Washington state's 2026 Individual Health Insurance Market. Insurers base their requested rate changes on assumptions they make about the services their policyholders will use and the cost to deliver that care. The health plans and proposed rate changes are currently under review by the Office of the Insurance Commissioner.

Wellpoint Washington, Inc. is new to the market and plans to sell in Grays Harbor, King and Spokane counties.

The good news is, the Illinois Insurance Dept. now provides a handy, simple table with the actual average rate changes as well as direct links to the actuarial memos & other filing forms for every carrier, which made it easy for me to plug in the effectuated enrollment & calculate the weighted average rate hikes for every carrier in both the individual and small group markets.

The bad news is, some of the actuarial memos themselves are heavily redacted, meaning I'm unable to see how much of the rate hikes are due to the IRA subsidies expiring, CSR payments being reinstated or Trump's tariffs.

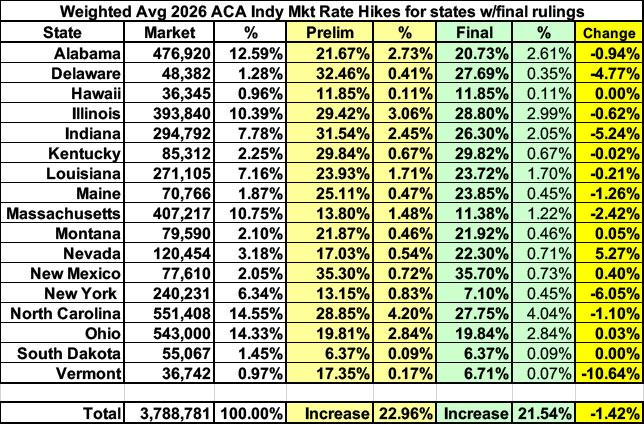

As of this morning I've confirmed final/approved filings across 17 states. Across these state the weighted average year over year increase is 21.5%, down about 1.4 points from the preliminary increase of 23.0%.

I expect final filings for at least a dozen more states to come in over the next week or so, but unless a couple of large states like Texas or Florida have dramatic reductions in their rate increases along the lines of New York or Vermont, I'd still expect the overall national average to and up over 20%.

Each year insurers that sell Individual and Small Group plans in Maine's pooled risk market must submit their proposed forms and rates to the Bureau of Insurance, using the System for Electronic Rate and Form Filing (SERFF). Details of the filings submitted to the state since June 10, 2010 can be viewed in the system.

Anthem Health Plans of Maine:

The proposed rates have been developed from 2024 Individual and Small Group ACA combined experience, and the proposed average annual rate change at the Merged Market level is 18.0%.

The proposed annual rate changes by product for Individual range from 17.9% to 20.6%, with rate changes by plan from 10.1% to 30.0%. These ranges are based on the renewing plans, and are consistent with what is reported in the Unified Rate Review Template. Exhibit A shows the rate change for each plan.

Factors that affect the rate changes for all plans include:

As I noted last month, Colorado's ~321,000 individual health insurance market enrollees are currently staring down the barrel of massive premium hikes less than four months from today:

Every state government is handling this situation differently. In Arkansas and New Hampshire, the strategy seems to be to either shout at or beg carriers to re-file with lower gross premium increases for 2026. New Mexico, California and New Jersey, in contrast, are all retooling their existing state-based supplemental subsidy programs to help cushion at least some of the impact.

For the individual market, this is actually slightly lower than the national average (23.4%), and New Hampshire will still end up with the 2nd-lowest avg. premiums in the country (Idaho should be slightly lower next year), but 22.4% is still pretty steep, and the state insurance dept. isn't happy about it:

New Hampshire Insurance Department Urges Health Carriers to Submit Revised 2026 Premium Rates Reflecting Current Economic Conditions