The Department of Insurance receives preliminary health plan information for the following year from insurance carriers by June 1 and reviews the proposed plan documents and rates for compliance with Idaho and federal regulations.The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

Back in July, I warned that my original projections from earlier in the year of how much net ACA enrollee premiums will increase starting in January 2026 in all 50 states +DC if the enhanced premium tax credits are allowed to expire would have to be revised & updated due to two major changes which had taken place since then:

This page contains proposed health plan rate information for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2026.

The District of Columbia Department of Insurance, Securities and Banking (DISB) received 188 proposed health insurance plan rates for review from CareFirst BlueCross BlueShield, Kaiser Permanente and United Healthcare in advance of open enrollment for plan year 2026 on DC Health Link, the District of Columbia’s health insurance marketplace.

The three insurance companies filed proposed rates for individuals, families and small businesses for the 2026 plan year. Overall, 188 plans were filed, compared to 198 last year. The number of small group plans decreased from 171 to 161, and the number of individual plans remained at 27.

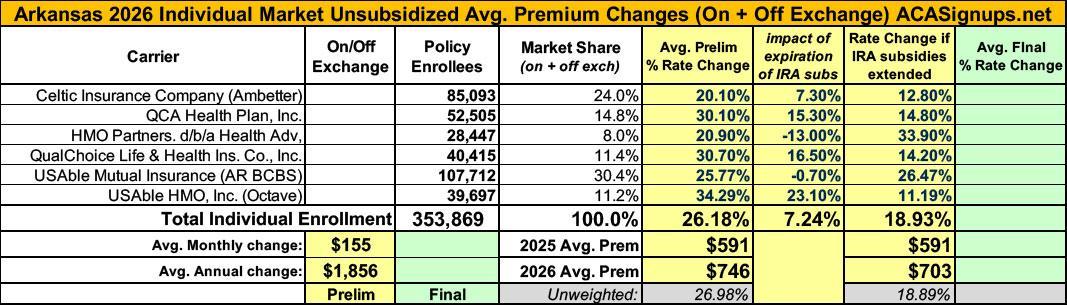

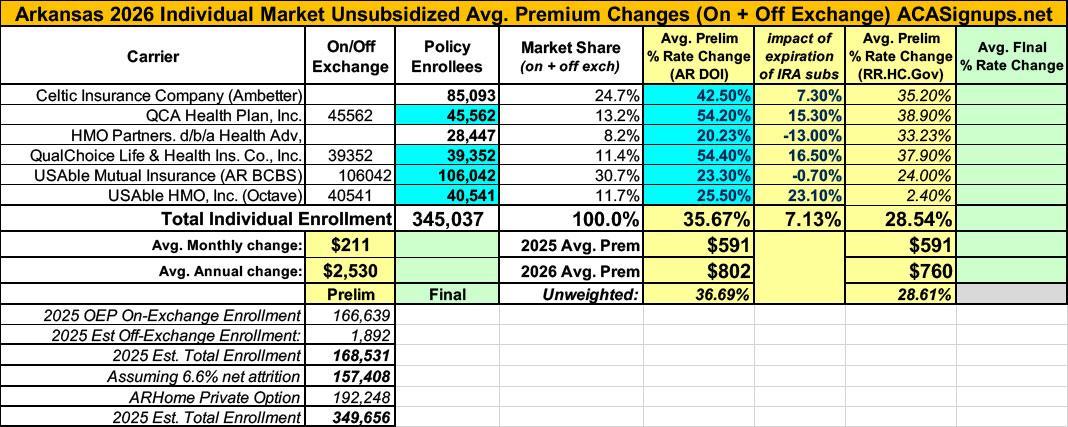

Back in July I posted my analysis of the preliminary 2026 rate filings by the 6 Arkansas insurance carriers participating in the individual market. At the time, they looked like this:

...This letter is formal notice that Aetna Health Inc. (“AHI”) intends to exit from the Individual health insurance market in Virginia effective January 1, 2026. Subject to the Department’s review, we will mail the 180-day notices of discontinuance to covered individuals.

As of May 2025, our records show that AHI has 9,810 subscribers and 13,721 total members in Virginia.

Health Carriers Propose Affordable Care Act Premium Rates for 2026

Anticipated loss of federal enhanced premium tax credits leads to highest individual market rate increases proposed since the start of Maryland’s reinsurance program

BALTIMORE – The Maryland Insurance Administration has received the 2026 proposed premium rates for Affordable Care Act products offered by health and dental carriers in the individual, non-Medigap and small group markets, which impact approximately 502,000 Marylanders.

Neighborhood Health Plan of Rhode Island (if IRA subsidies are extended):

Weighted Average Rate Increase: This represents the average rate increase, including modifications to prior year benefits and other pricing adjustments. The average premium increase to consumers, before reflecting changes in age is expected to be 16.3%.

The range of rate changes, before reflecting changes in age, which consumers will experience, is approximately 15.0% to 17.5%.

Neighborhood Health Plan of Rhode Island (if IRA subsidies AREN'T extended):

Weighted Average Rate Increase: This represents the average rate increase, including modifications to prior year benefits and other pricing adjustments. The average premium increase to consumers, before reflecting changes in age is expected to be 21.2%.

The range of rate changes, before reflecting changes in age, which consumers will experience, is approximately 20.1% to 22.2%.

Blue Cross Blue Shield of RI (if IRA subsidies are extended):

Maryland Insurance Administration Approves 2026 Affordable Care Act Premium Rates

Despite increases, Maryland remains a national leader in affordable rates; new state subsidy to offset loss of enhanced federal tax credits

BALTIMORE – Maryland Insurance Commissioner Marie Grant today announced the premium rates approved by the Maryland Insurance Administration for individual and small group health insurance plans offered in the state for coverage beginning January 1, 2026.

(Aetna/CVS is pulling out of the ACA individual market in every state; I've made an educated guess as to their current enrollees, who aren't counted as part of the weighted average as they'll have to shop around for a new carrier this fall. See below.)

Antidote Health Plan:

(Antidote's actuarial memo is heavily redacted so I don't know their current enrollment; I've had to make an educated guess. See below.)

I just finished writing up a deep dive into the Arkansas Insurance Dept's move from laissez faire-style Silver Loading to fully-regulated & maximized Premium Alignment in an attempt to mitigate the massive net premium damage about to be caused if the enhanced ACA premium tax credits expire at the end of 2025.

However, it's not just Arkansas which has finally seen the light and joined about a dozen other states in putting full-bore Premium Alignment (PA) pricing into place to help reduce the financial burden on ACA individual market enrollees in 2026.

Other states which have already done so in the past include Colorado (sort of), Texas, New Mexico, Maryland, Pennsylvania (somewhat), Illinois, Vermont and Wyoming.