UPDATE x2: Virginia's new state-based #ACA exchange officially goes live...glitch FIXED!

Tue, 10/10/2023 - 5:36pm

10/11/23: SEE IMPORTANT UPDATES BELOW!

In August I noted that Amy Lotven of Inside Health Policy had reported that Virginia's brand-new state-based ACA health insurance exchange had been officially approved by the Centers for Medicare & Medicaid Services:

Virginia is slated to become the nation’s 19th state-based exchange now that CMS has given officials the greenlight to fully transition away from healthcare.gov starting Nov. 1 for the 2024 plan year. Meanwhile, the State Corporation Commission (SCC), which administers the exchange, has suspended the state’s reinsurance program that had lowered premiums by about 20% for 2023, so individual plan rates are set to increase by an average 28.4%, according to a presentation made during an Aug. 9 hearing on the 2024 rates.

Virginia’s Health Benefit Exchange (VHBE) was enacted in 2020 by former Gov. Ralph Northam (D) and has been operating as a state-based exchange reliant on the federal platform (SBE-FP) since plan year 2021. The state paused the transition activity in 2021 after the enhanced premium tax credits were enacted but restarted it the following year.

A couple of weeks ago I noted that the new site had launched...with just the domain name,exchange name and logo: Virginia's Insurance Marketplace.

Today it was brought to my attention that the rest of the website has now gone live as well:

One minor detail: VA's Insurance Marketplace's social media links include Facebook, Instragram and YouTube...but not Twitter, which I find mildly interesting...

UPDATE 10/11/23 1:30pm: Ut-oh...while the site looks professional and seems to work pretty straightforwardly, a friend of mine in Virginia alerted me to a rather important glitch in the window shopping tool: It appears to be cutting off all APTC (Advance Premium Tax Credit) subsidies for households earning more than 400% of the Federal Poverty Level!

The so-called "Subsidy Cliff" at 400% FPL is something which was eliminated for two years back in 2021 when Congress passed the American Rescue Plan Act, and then extended by another three years under the Inflation Reduction Act last year. APTC subsidies should be available for ACA exchange enrollees regardless of their household income as long as the benchmark Silver plan costs more than 8.5% of that income at full price.

However, when I plugged in a few sample households, I discovered that the Virginia Insurance Marketplace is cutting off all subsidies the moment the household income rises above 400% FPL.

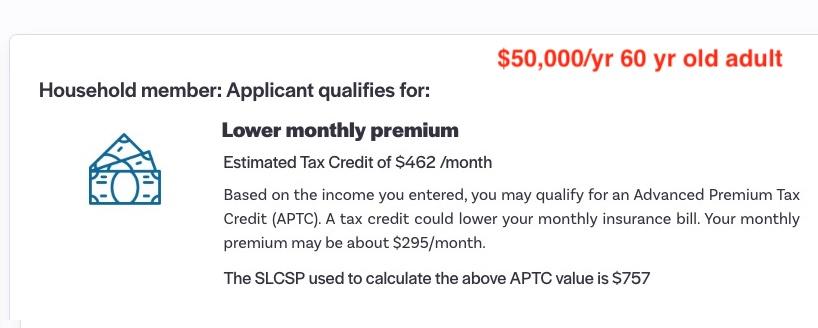

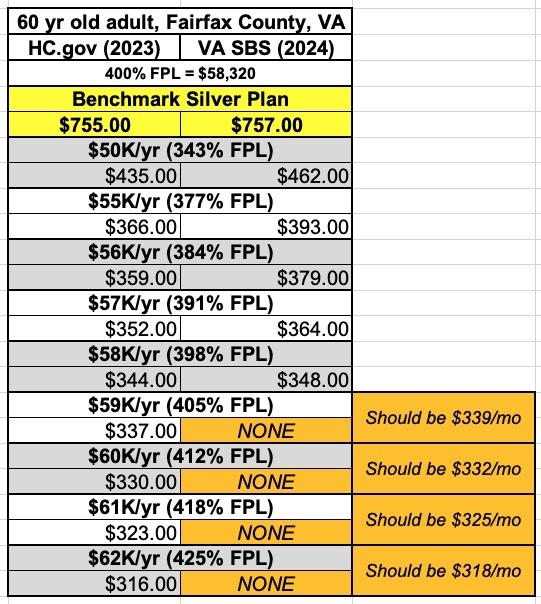

For example, here's a comparison of a 60-year old single adult living in Fairfax County, Virginia. For one person, the Federal Poverty Level is $14,580, so 400% of that is exactly $58,320/year.

Here's what happens when I plugged this example into the new Virginia state exchange (for 2024 coverage) at various incomes.

$50,000 is 343% FPL, so under the IRA's enhanced subsidy formula, this enrollee should only have to pay 7.08% of their income for the benchmark plan, or $295/month. Since the benchmark plan actually costs $757/month in 2024, they're eligible for $462/month in subsidies.

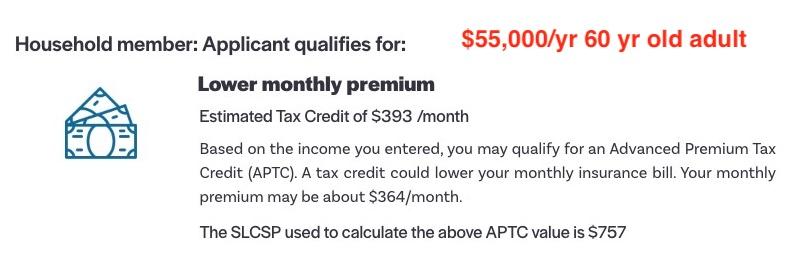

$55,000 is 377% FPL, so they should only have to pay 7.94% of their income for the benchmark plan ($364/month). This qualifies them for $393/mo in subsidies.

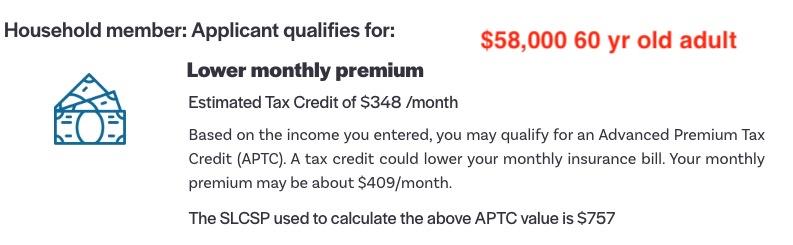

$58,000 is 398% FPL, so they should only have to pay just barely under 8.5% of their income for the benchmark ($409/month). This qualifies them for $348/mo in subsidies.

So far, so good.

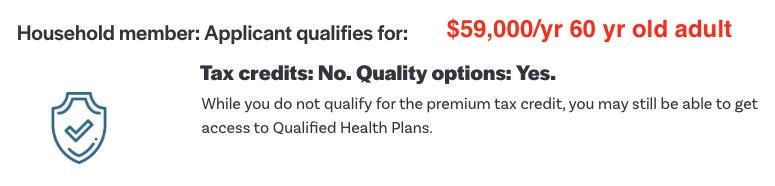

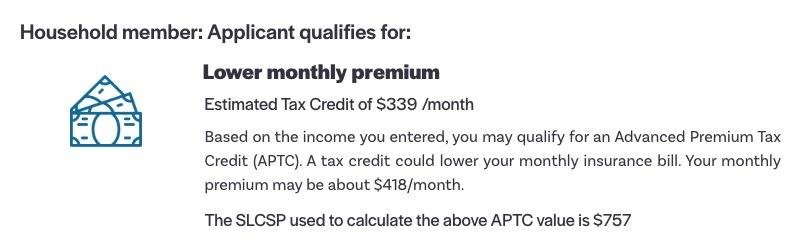

HOWEVER, $59,000 is 405% FPL. They should still qualify for $339/mo in subsidies, but the VA exchange calculator says they aren't eligible for anything!

Here's what it looks like compared against the 2023 APTC calculations according to HealthCare.Gov. The benchmark plans are nearly identical. The FPL for 2023 is slightly lower than it is for 2024, so the APTC calculations are slightly different as well, but the bottom line is that this 60-yr old enrollee should be receiving subsidies all the way up until their income reaches around $107,000/year ($757 x 12 = $9,084, which is 8.5% of $106,871).

I've already alerted the folks at GetInsured (the company which developed the VA exchange platform) and they're looking into the issue. Thankfully there's still 3 weeks to fix this and any other glitches before Open Enrollment launches on November 1st, but any Virginia resident who wants to test out the new exchange site before then should be aware that the subsidy calculator may have some tweaks required.

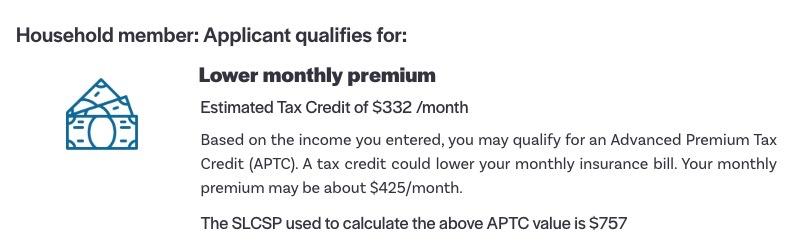

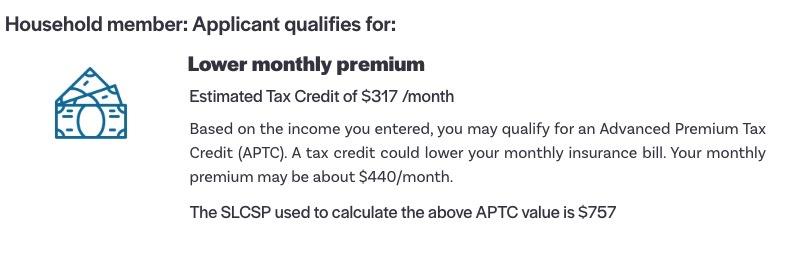

UPDATEx2 10/11/23 2:50pm: Wow, that was fast! It's been fixed already!

Here's what it looks like now when I plug in $59,000/year, $60,000/year and $62,000/year. I was off by $1 on the last one, however!

Advertisement