Virginia’s Republican-led legislature is on the verge of doing something that would’ve been almost unthinkable just a year ago: approving legislation that would use money from the Affordable Care Act to expand Medicaid to as many as 400,000 people.

That coverage expansion would come at a price for Democratic legislators, progressive activists and low-income Virginians, however. Any Medicaid expansion bill that makes it out of the General Assembly will carry with it new work requirements for Medicaid enrollees, a priority for the GOP at large and for President Donald Trump’s administration.

Democrats in the Virginia legislature have tried in vain for six years to persuade their GOP counterparts that accepting federal dollars to extend Medicaid coverage to poor adults is the right thing to do. Accepting a work-requirements policy that would create bureaucratic obstacles to eligible Virginians appears to be the compromise needed to win the bigger fight.

OK, I'm just seeing this now so I could be seriously misreading the article, but if I'm not, this is quite the eye-opener:

Virginia is on the cusp of expanding Medicaid to 400,000 low-income residents, after a veteran Republican state senator said Friday that he is willing to split with his party and help Democrats realize a goal they have been chasing for years.

Virginia state Sen. Frank Wagner (Virginia Beach) said he supports allowing more poor people to enroll in the federal-state healthcare program on two conditions.

He wants the plan structured so that Medicaid recipients do not suddenly lose coverage if their earnings rise. And he wants a tax credit or some other help for middle-income people who already have insurance but are struggling to pay soaring premiums and co-pays.

Last November, along with voting to keep a Democrat in the Governor's office, Virginia voters also swept a huge wave of Democrats into office in the state legislature. They didn’t quite take a majority, but they came within a single vote of getting a 50-50 tie in the state Assembly. Instead, they have a two-vote shortfall (51-49), matching the same two-vote shortfall (21-19) in the state Senate.

A prominent Republican state legislator from southwest Virginia announced his support Thursday for expanding Medicaid, an about-face that could make it easier for other rural conservatives to get on board after four years of steadfast opposition.

Maine voters on Tuesday decided to expand Medicaid to cover more low-income adults, becoming the first state to do so through a referendum.

Support for the ballot measure was up by more than 18 points with 64 percent of precincts reporting about 10 p.m. when it was called by NBC affiliate WCSH and The Associated Press.

The results in Maine, one of 19 states that rejected Medicaid expansion under the Affordable Care Act, comes as other Republican-led states like Utah and Idaho eye similar ballot measures.

Advocates of Medicaid expansion in Maine successfully petitioned the state to include a question on this year’s ballot following several failed legislative efforts to expand the program.

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

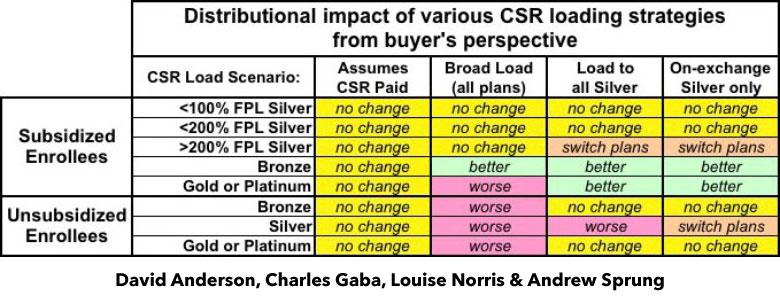

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

(sigh) When I last checked in on Virginia, things were looking up a bit (relatively speaking), as Anthem Blue Cross Blue Shield (aka "HealthKeepers") had announced that they were jumping back into the state in order to cover the 60-odd counties which would otherwise be left bare by Optima Health Insurance dropping out of half the state a week or so earlier.

As many see their options for health plans dwindle down to one insurer, premiums are simultaneously set to rise by an average of 57.7 percent next year in Virginia’s individual marketplace.

The increase is “unquestionably the highest we’ve ever seen,” David Shea, health actuary with Virginia’s Bureau of Insurance, told lawmakers Monday.

Anthem said Friday afternoon it planned to scale back statewide individual coverage in Virginia on the public exchange under the Affordable Care Act amid inaction by the Donald Trump White House on cost-sharing reduction subsidies.

Anthem, which operates under the Blue Cross and Blue Shield plan in 14 states, has already scaled back its Obamacare offerings in Indiana, Ohio and Wisconsin amid an unstable individual market for plans operating under the ACA.

“Today, planning and pricing for ACA-compliant health plans has become increasingly difficult due to a shrinking and deteriorating Individual market, as well as continual changes and uncertainty in federal operations, rules and guidance, including cost sharing reduction subsidies and the restoration of taxes on fully insured coverage,” Anthem said in a statement Friday afternoon. “As a result, the continued uncertainty makes it difficult for us to offer Individual health plans statewide in Virginia.”

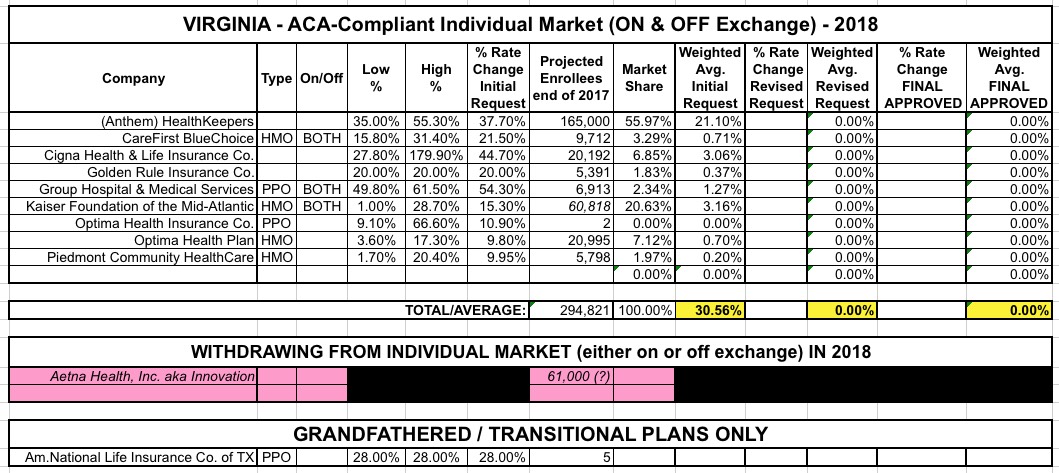

Virginia was the very first state whose 2018 rate filings I analyzed, way back in early May. At the time, the initial filings amounted to 9 carriers on the individual market with an average rate increase request of around 30%. At the time I hadn't started distinguishing between "with CSR payments" or "without CSR payments", so I don't really know which scenario that 30% reflected; it was probably a mix of both depending on the carrier. 61,000 Aetna enrollees would have to shop around for a new carrier since they had previously announced they were pulling out of the individual market.

For the past two years, Virginia has been the first state in the nation to post their initial rate filings for the following year. I originally compiled their individual market 2018 change requests back in early May, and came up with the following at the time:

UnitedHealthcare had previously announced they were dropping out of Virginia, but I didn't have an enrollee number for them, and Aetna had also just announced their withdrawl from the state. I hadn't yet finalized my "CSR/Mandate Penalty" factor layout yet; at the time I assumed the 30.6% weighted average requested assumed full CSR/mandate sabotage and reduced that number by 17 points based on the Kaiser Family Foundation's "19% national average CSR rate hike" estimate analysis, which estimated the CSR impact at 17 points for Virginia.

UPDATE: As I've been warning for months, at least one of VA's carriers has openly stated that perhaps 40% of their requested rate hike is due specifically to concerns about the Trump administration & the GOP's ongoing sowing of confusion and outright sabotage of the ACA and the individual market.

A couple of weeks ago I noted that Virginia is one of the first states to post their initial premium rate hike filings. At the time, they hadn't posted the actual filings but at least listed the insurance carriers which were planning on participating in the individual and small group markets next year, both on and off the ACA exchange: