As noted before, I'm really trying to move onto the actual enrollment part of the 2017 open enrollment period, but I can't resist doing some more final cleanup of my Rate Hike project:

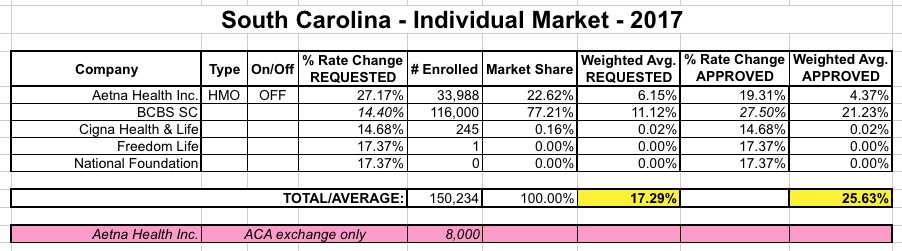

SOUTH CAROLINA: This is one of the 5 states which I still didn't have approved rate changes for. Today the RateReview.HC.gov site finally added in the final numbers for SC, so here's what it looks like:

Aetna was a bit tricky--the total enrollee number is actually 41,988. They dropped out of the ACA exchange but are sticking around the off-exchange market, so I had to figure out how many of those 42K are on vs. off-exchange. The answer is in this article which notes:

More than 220,000 South Carolinians rely on the federal health care law for insurance. This year, only 8,000 of them are covered by Aetna plans.

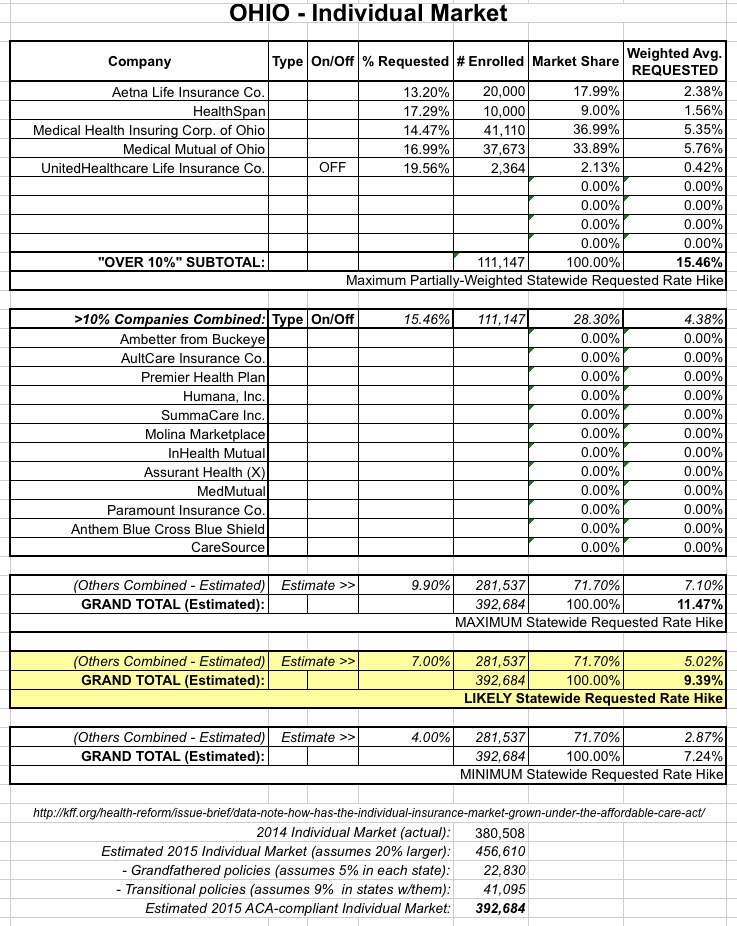

Here's some relatively good news! Ohio's 2017 requested rate filings have finally been published, and considering that some other states are looking at weighted average requested increases of 30%, 40% or even as high as 56%, Ohio's 13.1% average is actually refreshingly low by 2017 standards.

It's actually even better than that, because as you can see below, I haven't been able to track down the actual current membership number for "Buckeye Community Health" (aka Ambetter)...and Buckeye is asking to lower their rates slightly, by around 1% on average. To get an idea of how this could impact the statewide average:

Assuming 0 enrollees: No impact at all; 13.1% average.

Assuming 10,000 enrollees: Would reduce avg. to 12.4%

Assuming 50,000 enrollees: Would reduce avg. to 10.1%

Assuming 100,000 enrollees: Would reduce avg. to 8.1%

Again, without knowing how many people Buckeye/Ambetter actually has currently enrolled, it's impossible to say what the weighted statewide average is...but I can say that it's no more than 13.1%.

When the dust settled, there were 11 Co-Ops left standing, but most of them were still on pretty shaky ground, with all but a handful placed under "enhanced oversight" by their states (and I have to admit that the term sounds an awful lot like a euphamism, a la "enhanced interrogation technique").

Thanks to Richard Simpkins for bringing this to my attention.

A week or so ago, Akash Chougule, Director of Policy at Americans for Prosperity (you know, the Tea Party political outfit funded by the Koch Brothers), posted an Op-Ed piece at Forbes tearing apart Ohio Governor John Kasich's decision to expand Medicaid via the Affordable Care Act. From a Republican POV, of course, Kasich agreeing to accept ACA Medicaid expansion is blasphemous. The piece was posted just ahead of the Ohio Republican Presidential primary, so naturally it was intended to hurt his chances of winning his home state (it didn't work, of course; Kasich did indeed win Ohio, keeping his campaign alive awhile longer, if just barely).

Anyway, here's the part which made both Simpkins and myself scratch our heads:

Ohio Governor John Kasich has spent no small amount of time on the presidential campaign trail discussing his decision to expand Medicaid to 650,000 able-bodied adults under Obamacare. But policymakers in non-expansion states should take a closer look at what’s actually unfolded in Ohio before considering going down the same path.

I originally intended this to be an update to yesterday's post about the woman at the Ohio Democratic Town Hall in which a woman asked Hillary Clinton why her family's insurance rates have gone up from $490/month to $1,081/month since the Affordable Care Act was passed. However, that post had already gotten absurdly long and unwieldy, so I've split it off into a new entry.

In the comments yesterday, a man named Danny Robins posted the following. I've broken it up a bit for readability, and have included my responses; both his points and my responses lend some additional insight into both Ms. O'Donnell's dilemma as well as my own point about Clinton's response:

My Columbus Ohio based health insurance practice for the past 7 years has been focused on helping small employers offer more affordable health benefits outside of the employer sponsored health insurance market. It has been widely reported that up to 70% of small employers no longer sponsor a health plan because they can not afford it. As such, I have assisted with over 2,000 people obtain individual or family health coverage.

And then there are the portions of the law which have gone, well, not so great, to put it mildly...in particular the non-profit, public/private hybrid Co-Ops, which are the only remaining remnant of the originally much-hoped-for "Public Option". For a variety of reasons, not the least of which was an utterly unnecessary and ultimately pointless stunt pulled by Marco Rubio and other Congressional Republicans (aka the Risk Corridor Massacre), over half of the two dozen Co-Ops nationwide melted down in spectacular fashion last fall, leaving only 11 of them surviving into 2016 after the dust settled.

In light of this, I figured it would be worth posting some positive Co-Op news for a change. First up, Ohio.

I admit that given the carnage of the past couple of weeks, I'm almost afraid to post this entry...but I had to write something positive about the CO-OP situation.

With the ACA-created CO-OPs seemingly dropping like flies due to the #RiskCorridorMassacre, I thought this would be a good time to flip things around and look at which CO-OPs are doing well (or at least not badly).

This isn't much, but it'll do for now:

Wisconsin's insurance department says it has no intention of shutting down its #ACA co-op, which appears it will remain solvent next year.

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and mid-range requested average rate increase for the Ohio individual market:

Again, the full explanation is included here, but to the best of my knowledge, it looks like the companies with rate increases higher than 10% come in at a weighted 15.5% increase, but only make up about 28% of the total ACA-compliant individual market, with several other companies with requested increases of less than 10% (decreases in some cases) making up the other 72%.

This AP article provides snippets about a handful of states; it'd be nice if they just released the actual report so we could see the hard expansion numbers (as opposed to the total increase numbers, which are still obviously useful but don't distinguish between traditional Medicaid and ACA expansion enrollees):

In Kentucky, for example, enrollments during the 2014 fiscal year were more than double the number projected, with almost 311,000 newly eligible residents signing up. That's greater than what was initially predicted through 2021.

...At least 14 states have seen new enrollments exceed their original projections, causing at least seven to increase their cost estimates for 2017, according to an Associated Press analysis of state budget projections, Medicaid enrollments and cost details in the expansion states. A few states said they could not provide original projections.

David Ramsey has the full skinny on the unpleasant situation in Arkansas, where their "private option" Medicaid expansion program, which was always weird with a beard to begin with, is very much at risk of collapsing altogether:

Well, here we go again. The legislature is once again ready to debate the private option – the state’s unique version of Medicaid expansion, which uses funds available via the Affordable Care Act to purchase private health insurance for low-income Arkansans. Gov. Asa Hutchinson will take a long-awaited position on the policy in a speech at UAMS tomorrow morning. Then it will be up to the legislature. Health insurance for more than 200,000 Arkansans is at stake. Here are some keys to remember as the debate unfolds tomorrow and in the coming weeks.

The short version: The AR program has to be re-approved by the legislature every year, and requires a 75% majority to do so, so it's a wonder that it's survived this long, frankly.