Until today, I operated under the assumption that my home state of Michigan was among the 18 states which took the "Silver Load" approach to dealing with the Cost Sharing Reduction (CSR) cut-off by the Trump administration. Reviewing the SERFF rate filings of the various carriers participating in the individual market, it looked like most of them were loading the CSR cost onto both on and off-exchange Silver plans. I didn't check every single carrier, but that seemed to be the trend, so I filed the state under "Silver Load".

I'm signing up for a plan off the exchange with Priority Health in Michigan. ON-Exchange, the plan is $365 a month, but off exchange (directly from their website), the price is $300 per month. I don't qualify for a subsidy, but it's still cheaper than my 2017 plan with BCBSM. That was the Multi-State Plan in Region 7 with Dental and Vision.

Hey there, I called again and I was able to talk to a more knowledgeable agent who found out what the issue was and was able to enroll me in a plan!

Apparently, the Marketplace renewed automatically my application based on my 2016 income, which was enough to receive a tax credit in 2017, but is no longer enough to receive one in 2018.

Luckily, my income has increased since then, so I reported the change and was able to get a credit applied to the premiums

Still need to send copy of my green card for verification, but I can use the tax credit immediately

So I'm not sure why the person I talked to earlier today told me the rules had changed

Sorry for the confusion

OOF. OK, this pretty much torpedoes the entire basis of this blog entry. I'm going to leave it up in the interest of letting documented immigrants know that they ARE eligible to enroll AND for tax credits, but it sounds like the original concern may be unwarranted after all.

To summarize (again), this is where someone whose household income is too high for them to qualify for ACA tax credits (400% of the Federal Poverty Line) chooses an ACA-compliant off-exchange Silver plan instead, which is either identical or nearly identical to the same on-exchange policy in every way except that the additional CSR load hasn't been tacked onto it.

Here's a perfect example found by Louise Norris...ironically, this is via Priority Health here in Michigan, which (until today) I thought was a "Silver Load" state, not "Silver Switcharoo". I'll have to do some more research to be sure, but it sounds like at least one MI carrier (Priority) is going full Switch:

In the other 11 states (+DC), the deadline to enroll for 2018 coverage is later...but the final dates range from Dec. 22nd (CT) to as late as Jan. 31 (CA, DC & NY).

UPDATE: As of January 2nd, 2018, there are 7 states where Open Enrollment is still ongoing:

UPDATE: It looks like this issue may be limited to a single carrier in New Mexico; I've changed the headline and graphic accordingly...but it might be an issue in other states as well; if so I may have to change it back again...

Insurers That Filed Wrong Rates Told By CMS They Can't Sell Plans Through Mid-November

An issuer whose final CMS-approved rates don’t account for the loss of cost-sharing reduction payments is being told by the agency that they won’t be able to sell plans until healthcare.gov data is refreshed– even though this would mean the carriers are even more crunched for time to sell their plans during the shortened open enrollment period.

The very first bullet starts off ripping on the 37% average rate hike on benchmark Silver plans...

Benchmark Premiums: The average monthly premium for the second-lowest cost silver plan (SLCSP), also called the benchmark plan, for a 27-year-old increased by 37% from plan year 2017 (PY17) ($300) to PY18 ($411).

Premium Growth: For the first time, annual growth in the average monthly premium available to a 27- year-old for the SLCSP, at 37%, outpaced that of the lowest-cost plan (LCP), at 17%.

Of course, there's pretty obvious reason for that: Trump's cut-off of Cost Sharing Reduction (CSR) reimbursement payments. The ASPE report does go into this, but not until Page 6. Meanwhile, it's immediately undermined anyway (at least regarding subsidized enrollees) in the very next bullet:

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase isbetween 29-30%, ranging from as low as a 22% average premium drop in Alaska(thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

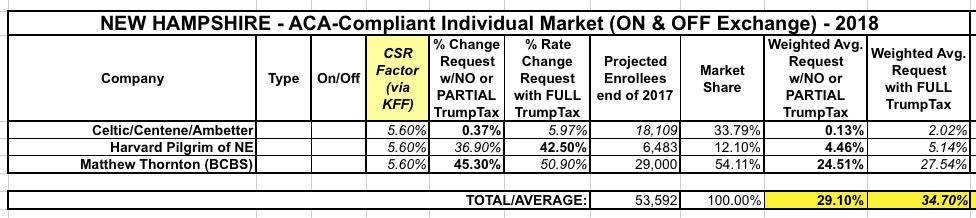

As noted earlier today, I've now managed to plug 48 states (plus DC) into my 2018 Rate Hike Project spreadsheet. This leaves just two states missing: New Hampshire and Texas. I'm still waiting to clarify some things for each, so this analysis could still change, but I really want to wrap this up, so here's what I have for New Hampshire right now:

When I first ran the numbers for New Hampshire'srequested 2018 rate increases, it seemed pretty straightforward: 3 carriers on the individual market. 2 listed rate changes assuming CSRs would be paid; one assumed they wouldn't. This gave the following:

Still, I don't like loose ends, and those 8 missing states are bugging me, so I still want to fill them in for completeness' sake. The only big state remaining is Texas, but I'm also missing Alabama, Hawaii, Iowa, Missouri, New Hampshire, Oklahoma and Wyoming.