As regular readers know, every spring/summer I spend countless hours poring over the annual insurance carrier rate filings, plugging in increases (and occasionally decreases) in ACA-compliant premium changes for every carrier in every state. I actually do this twice for most states (and occasionally even three times), as the process moves from preliminary/requested rate changes to "semifinal" rates to "final/approved" rates throughout the fall.

For 2018 and again for 2019, I've taken this one step further; instead of simply running the overall weighted average premium changes in each state, I've also attempted to break out what portion of the change is caused by various factors...in particular, what portion is caused by legislative or regulatory changes by Congressional Republicans and/or the Trump Administration.

OK, I had kind of forgotten about this. Back in early June, insurance carriers in Pennsylvania submitted their preliminary 2019 ACA market premium change requests. At the time, they averaged around a 4.9% increase statewide, which seemed pretty impressive under the circumstances.

Then, late July, the PA insurance department issued a press release stating that state regulators had modified the 2019 requests, and that the new, revised average was much lower...a mere 0.7% average rate hike. However, the individual carriers as well as the insurance department made it very clear that this nominal increase included a 6 point rate increase to account for the ACA's individual mandate being repealed and the Trump Administration's expansion of non-ACA compliant short-term and association plans.

However, the DC exchange board was also working quickly in an attempt to counter the Trump Administration's #ACASabotage factors, by voting to restrict short-term plans, to lock in DC's Open Enrollment Period at a full 3 months as in years past, and to reinstate the ACA's individual mandate penalty at the local level.

Premium Rates for Individual and Small Group Markets Individual plan premium rates may vary by age, rating area, family composition and tobacco usage. For example, a person living in Manhattan, KS (rating area 3) may pay a different rate than someone living in Pittsburg, KS (rating area 7) based on the claims data by rating area. A map of the counties included in each rating area is provided on the next page. Kansas is an effective rate review state, which means the actuarial review is conducted by the Kansas Insurance Department. KHIIS (Kansas Health Insurance Information System) claims data is utilized during the rate review process to verify the claims experience submitted by the companies. The following table provides details regarding the average requested rate revisions for companies writing individual policies in Kansas. Rate increases will be partially offset for individuals receiving a premium tax credit.

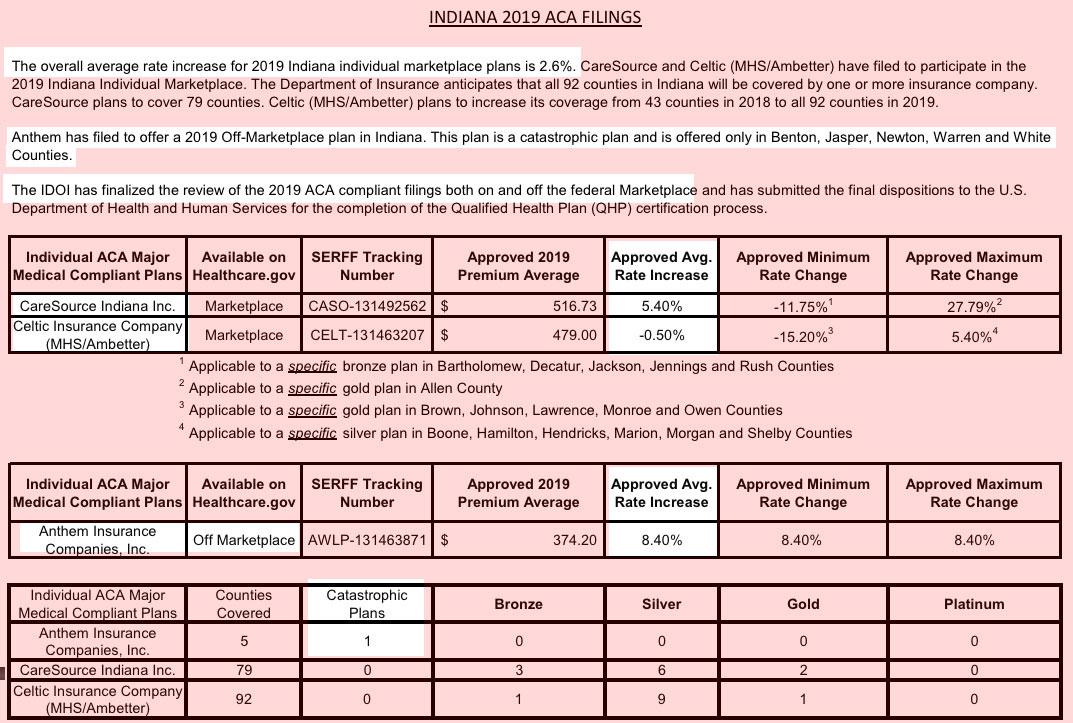

Back in June, Indiana's 3 individual market carriers submitted their requested 2019 ACA rate changes, which averaged around 5.1%. At the time I also pegged the impact of #ACASabotage on 2019 rates (mandate repeal + #ShortAssPlans) at around 13 percentage points.

The Department of Insurance received preliminary 2019 health plan information from insurance carriers on June 1 and began reviewing the proposed plan documents and rates for compliance with Idaho and federal regulations. The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate 2019 increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

Wisconsin has an interesting situation. On the one hand, the state has what should be a robust, highly-competitive individual insurance market,with over a dozen carriers offering policies throughout the state. Granted, some of them are likely limited to only a handful of counties, but in theory they should be doing pretty well compared to rural states like Oklahoma or Wyoming, which only have a single carrier on the exchange.

On the other hand, last year Wisconsin ahd among the highest average premium rate increases in the country. Rates were projected to increase by an already-awful 36%, but when the dust settled the average unsubsidized ACA enrollee in Wisconsin was paying a whopping 44% more than they did in 2017 (it was around 45.8% higher as of the end of Open Enrollment but later dropped a bit as the year has passed and net attrition has tweaked the enrollment base).

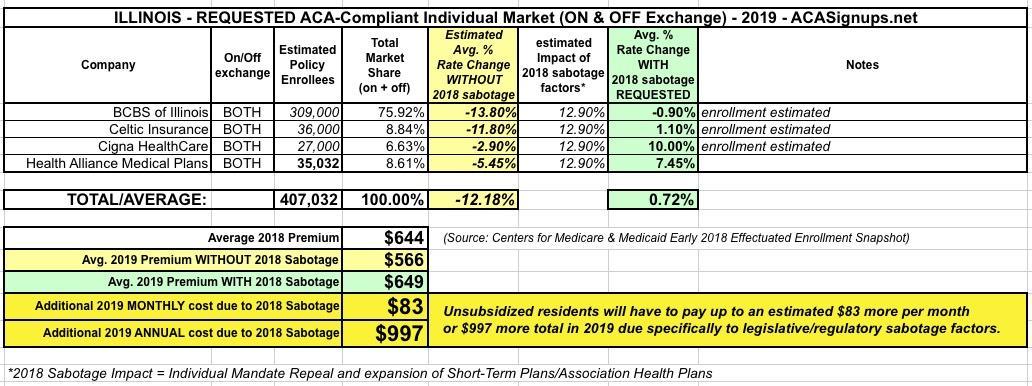

I ran the numbers for Illinois' requested 2019 ACA individual market rate changes back in August. At the time, the weighted year-over-year average was a mere 0.7% increase, with Cigna and Health Alliance's 10% and 7.5% being mostly cancelled out by Celtic's 1.1% and especially Blue Cross Blue Shield's slight drop of 0.9%. Since BCBSIL holds something like 3/4 of the state's individual market share, that alone mostly wiped out the other increases.

Unfortunately, I don't have access to the hard enrollment numbers, so this was a rough estimate based on 2017's breakout. Here's what it looked like at the time:

The final unsubsidized rates are down about one point more, down 6.3% from 2018 rates. However, as all three current carriers clearly noted in August, the repeal of the ACA's individual mandate and expansion of short-term and association health plans (aka #ShortAssPlans) still caused a significant premium increase, which means without those factors, 2019 rates would likely be down significantly more...likely nearly 20% instead of 6.3%: