Depending on the state & carrier, some of these can be found easily; others are either heavily redacted, partial, not available until later in the year; and some are never made available at all.

In addition to the filings for the upcoming year, however, the SERFF database also includes a mountain of other filing forms, from non-ACA compliant insurance policies (short-term, indemnity, etc.) and from previous years (I have no idea how far back they go, but I'm guessing it's at least since the turn of the century). This also includes "grandfathered" and "grandmothered" policies.

The total individual/family policy health insurance market was roughly 10.6 million people in 2013. This included people enrolled in either "grandfathered" policies (i.e., policies enrolled in prior to the ACA being signed into law in 2010) or in "transitional" policies (those enrolled in between 2010 and late 2013, just before the ACA required all new individual market policies to be fully compliant with the new healthcare law.

How many of those 10.6 million people are still enrolled in grandfathered (GR) or transitional (TR) policies today? Unfortunately, there seems to be very little available data about just how many people are still in these policies. The Kaiser Family Foundation gave a rough estimate of around 2.1 million people last year, which sounded about right to me. However...Kaiser didn't include a state-level breakout of their estimates, and of course it's a year later so that number, if accurate, has probably shrunk a bit more.

The total individual/family policy health insurance market was roughly 10.6 million people in 2013. This included people enrolled in either "grandfathered" policies (i.e., policies enrolled in prior to the ACA being signed into law in 2010) or in "transitional" policies (those enrolled in between 2010 and late 2013, just before the ACA required all new individual market policies to be fully compliant with the new healthcare law.

How many of those 10.6 million people are still enrolled in grandfathered (GR) or transitional (TR) policies today? Unfortunately, there seems to be very little available data about just how many people are still in these policies.

As you may have noticed, I'm on a bit of a grandfathered/transitional plan data kick this week (there's a reason for it which you'll understand next week). These numbers are tricky to hunt down, since they aren't tracked by the ACA exchanges. Most states either don't track them at all or don't make it easy for the public to locate, and it's even treated as a proprietary trade secret in a few states.

The Kaiser Family Foundation gave a rough estimate of around 2.1 million people still being enrolled in GF/TR plans last year, but they never broke it out by state. Plus, of course, that was last summer; since no one can newly enter these types of policies, their numbers continue to gradually shrink year after year.

Earlier today I wrote an extensive post about California's individual market, specifically breaking out the number of off-exchange policies, including a rare look at some hard grandfathered plan enrollment numbers.

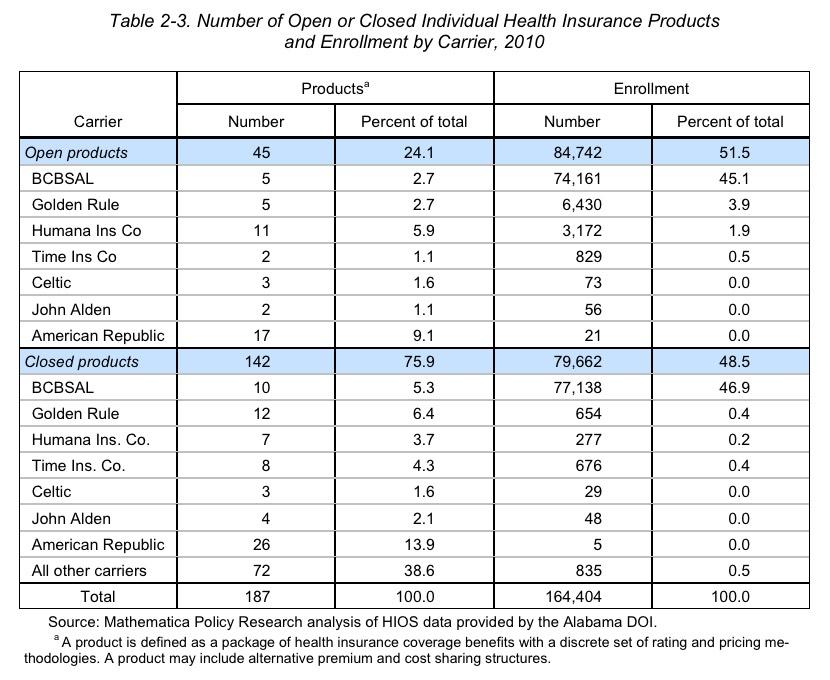

I've also managed to dig up a fascinating document from 2010 buried on the Alabama Insurance Department's website, which provides quite a bit of demographic insight into Alabama'soverall health insurance market. While all of this info is now 8 years out of date (and even precedes the first ACA open enrollment period), it does provide a few clues into estimating what's going on in Alabama today.

This first table shows exactly what Alabama's individual market looked like: 164,404 people were enrolled in pre-ACA "major medical" policies in 2010:

The California Health Care Foundation is a nonprofit philanthropic organization. From their About page:

The California Health Care Foundation is dedicated to advancing meaningful, measurable improvements in the way the health care delivery system provides care to the people of California, particularly those with low incomes and those whose needs are not well served by the status quo. We work to ensure that people have access to the care they need, when they need it, at a price they can afford.

This just in from the California Insurance Dept...

Thank you for signing up to receive email alerts when new health insurance rate filings are submitted to the California Department of Insurance.

This message is to inform you that we have posted new rate filing submissions to our health rate filing website. Please select the link below to review and/or comment on newly added rate filing submissions. The Department of Insurance does not respond to questions about rate review filings submitted through the rate website, but we do consider comments during our review process.

Last week I took the known 2016 Florida rate increase requests (around 14.7% weighted average for 10 companies with around 713,000 enrollees) and took my best shot at trying to estimate what the rest of Florida's ACA-compliant individual market might look like.

In order to do this properly, I'd need 2 pieces of data: First, the weighted average increase request for the 6 additionalcompanies which I didn't already have rate requests for; and second, the total ACA-compliant enrollment number for those 6 companies.