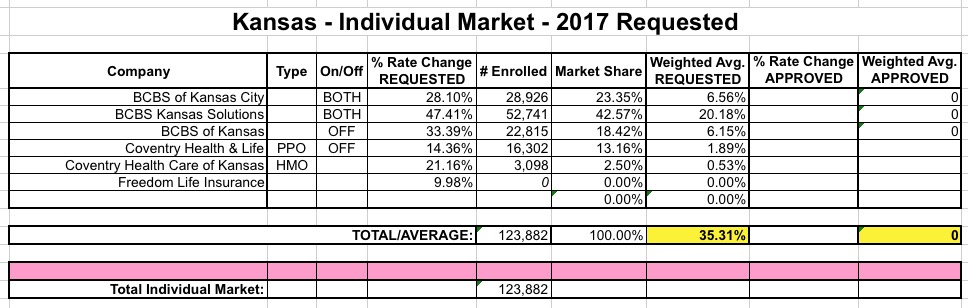

The good news about Kansas is that 5 of the 6 carriers which have submitted 2017 individual market rate filings included their current enrollment totals in a clear, easy to see format...and the 6th one is (once again) "Freedom Life" which, judging by the dozen other states they've popped up in, almost certainly has only 1 or 2 enrollees (or none at all) anyway.

The bad news is...well, the requested rate hikes are pretty ugly: About 35.3% on weighted average.

Also, is it really necessary for Blue Cross Blue Shield to operate under three nearly-identical names? Really?

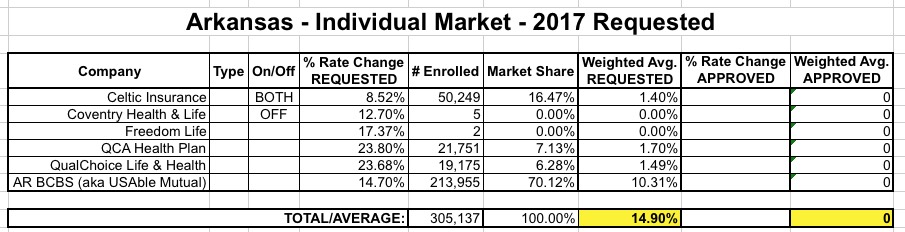

Arkansas was a little weird...while the rate filings for 5 carriers are listed over at RateReview.HealthCare.Gov, the carrier with the largest individual market share in the state, BCBS (aka "USAble Mutual") is nowhere to be seen (there's a sm. group listing for them, but not individual). However, when I went directly to the AR SERFF database, there they were--and it's listed specifically as "2017 Individual QHP Rates", so there's no question here about whether they plan on offering ACA-compliant policies in 2017.

Anyway, between the HC.gov site and the SERFF site I was able to cobble together pretty much all of Arkansas' indy market. The numbers seem about right; AR's indy market was around 303K in 2014; while it's likely up to 375K or so today, the "missing" 70K can easily be attributed to UnitedHealthcare dropping out and/or grandfathered/transitional enrollees.

At 14.9% on average, this is actually good news for 2017, relatively speaking.

Oklahoma's entire individual market (including grandfathered/transitional plans) was around 172,000 people in 2014. Assuming it's grown roughly 25% (in line with the national increase), it should be up to perhaps 215,000 people by today, of which perhaps 195K are ACA-compliant.

This is significant because there appear to be only 3 carriers offering individual policies in Oklahoma next year...one of which is the infamous "Freedom Life Insurance Co." which I wrote about last night. Since Freedom Life has (as usual) only a single enrollee in the state, it's really a nonfactor for calculating the weighted rate hike average.

That leaves Blue Cross Blue Shield of Oklahoma, which has a whopping 170,000 enrollees...and CommunityCare (which is in turn broken into HMO and PPO divisions)...unfortunately, their rate filing doesn't include their enrollment number; all it says is that it's "too small to be credible" to be used as the basis of their rate hike request. In addition, UnitedHealthcare is dropping out of the OK indy market; I don't know how many enrollees they actually have.

Throughout the summers of 2015 and 2016, the news media was chock-full of apocalyptic headlines screaming about MASSIVE DOUBLE DIGIT OBAMACARE RATE HIKES!!!, suggesting that rate hikes of 20%, 30% even 50% would be not just widespread but the norm nationally.

The reality, as I repeatedly tried to get through people's heads, is that while some carriers in some states were trying to push through massive hikes on some plans, the overall picture was far less dramatic. Many were seeking increases of under 10%, while some (not many, I admit) were even reducing rates. When you averaged out the rate changes by state and then weighted them by the number of people actually enrolled in those policies, it came in at around 7-8% in 2015 and around 12-13% in 2016.

Hmmm...last year Nebraska had 5 carriers offering individual policies, 2 of which were actually divisions of the same company (UnitedHealthcare). Since United is pulling out of Nebraska, this leaves only three companies...one of which is the mysterious "Freedom Life Insurance Co." which keeps popping up in numerous states as not having a single actual enrollee, and almost always asking for the exact same rate hike: 17.37%. What's up with that?

Anyway, Coventry (actually Aetna) appears to also be gone next year as well...or perhaps they simply haven't submitted their rate filings yet? I suspect the latter because Nebraska's total individual market was over 110,000 people as of 2014, and is likely up to over 130K this year (nearly 88,000 enrolled via the ACA exchange alone this year)...yet adding up the numbers from the official filings only totals around 30,000 people.

North Carolina's individual market, which only had 5 carriers participating to begin with this year, suffered a double blow recently when both UnitedHealthcare (155,000 enrollees) and Humana (3,272 enrollees) announced that they were dropping out of the market entirely next year (Celtic is also leaving the state, but they have literally just 1 person enrolled state-wide anyway). Fortunately, nature abhors a vacuum, so Cigna Health & Life Insurance decided to join the exchange for 2017. Cigna is already selling off-exchange individual policies, but only has fewer than 1,300 people enrolled in them at the moment. There's also a carrier called "National Foundation Life Insurance" which is raising rates 17.4%...but doesn't have a single person enrolled at the moment anyway, so I'm not sure what to make of that.

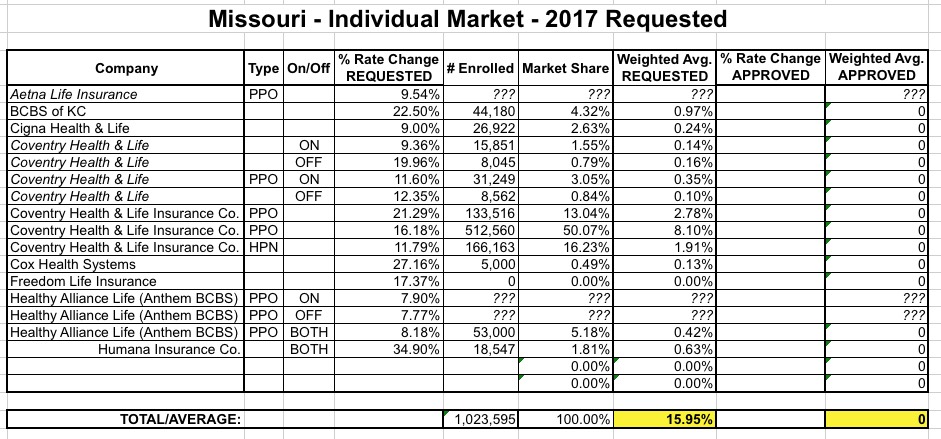

OK, there's something very odd going on with Missouri's 2017 rate filings for the individual market. According to the Kaiser Family Foundation, Missouri's entire individual market was around 344,000 people in 2014. While it's likely increased by around 25% since then, that would still only bring it up to around 430,000 people including both grandfathered and transitional enrollees, which sounds about right to me (290,000 enrolled via the ACA exchange, which would leave around 140,000 off-exchange).

And yet, when I plug in the official rate filings for Missouri's individual market for 2017, here's what it looks like:

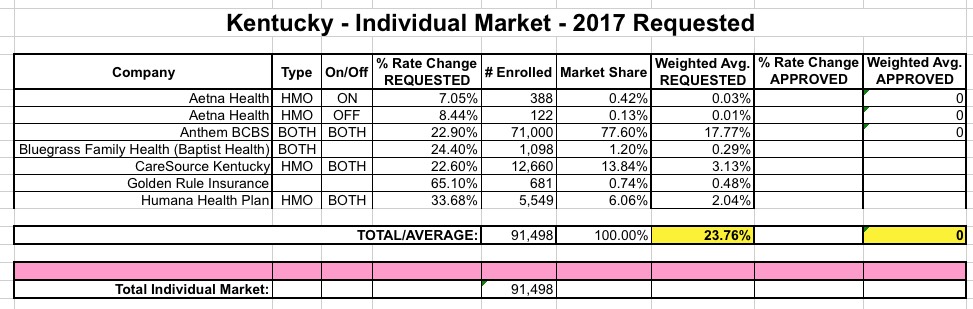

Not much to say about the bluegrass state...taken together, the 6 carriers offering individual policies in Kentucky appear to be requesting an average rate hike of 23.8%, ranging from Aetna's single-digits for a few hundred people up to Golden Rule's stroke-inducing 65% hike. One thing to note is that KY's total individual market was around 163,000 people in 2015, and is likely around 25% higher today (around 203,000), so over half of the market is likely missing from this table:

With only 584,000 residents, Wyoming is the smallest state, with a population over 10% smaller than even the District of Columbia or Vermont. Last year there were only 2 insurance carriers offering individual policies on the ACA exchange, Blue Cross and WINhealth. The average rate increase for 2016 was right around 10% even.

WINhealth sent along this release saying: As of October 8, 2015, WINhealth has chosen not to participate in the individual market, to include the federal exchange, for the 2016 plan year. The decision not to participate stems from a recent announcement from the federal government regarding the risk corridor program .