Health insurance companies that want to raise rates more than 10 percent next year will get an extra dose of scrutiny from Alabama regulators this year – for the first time since the marketplace launched in 2013.

Under Obamacare, states were supposed to implement systems for reviewing, and in some cases rejecting, rate increases that exceed 10 percent. Alabama was one of six states that didn't create an effective rate review program, despite receiving a $1 million grant to bolster oversight at the Department of Insurance, according to the Centers for Medicare & Medicaid Services.

After crunching the numbers for the requested rate changes (OK, rate hikes) across 31 states & DC, it looks like it's gonna be awhile longer for the remaining 19 states to post their rate filings publicly. For instance, while Michigan's SERFF database has had a whole mess of rate filing stuff posted for weeks now, none of them appear to include the two pieces of crucial data that I need for this project: The actual requested average percentage rate changes and the actual number of current lives covered by those policies...and likely won't for at least another week:

2017 Rate Filings - Individual Products - ALERT

The 2017 Individual Product filings are not yet complete. Partial filing information was submitted by issuers on May 9, 2016.

By my count, Tennessee has a total of 6 companies offering individual policies this year (Aetna, TRH, BCBS of TN, Cigna, "Freedom Life" (hah!) and Humana. UnitedHealthcare is dropping out next year, leaving at least 37,000 people to switch to a different policy (this is based on this article in the Tennessean, which claims that United currently has 15.76% of the On-exchange individual market in Tennessee). TN had 269,000 people select exchange-based QHPs during the 2016 open enrollment period. Assuming around 13% net attrition since then, that leaves around 234,000 current enrollees on the exchange. If United holds 15.76% of those, that's around 37,000 poeple.

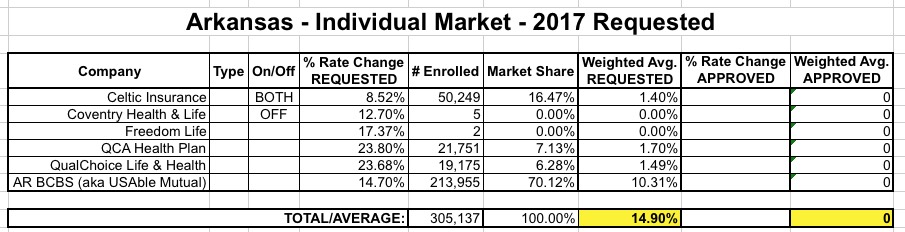

So just last Friday I posted the weighted average requested rate hikes for the Arkansas individual market; it came in at 14.9% overall, which is actually one of the lower statewide averages this year. As a reminder, here's what how the breakout looks:

OK, so 3 major carriers asking to jack up rates 15-24%, plus one at 8.5% and two others with just 7 enrollees between them (one of which is, once again, Freedom Life Insurance). So what?

As regular readers know, I'm currently in the thick of my state-by-state analysis of the requested, weighted average rate changes for 2017 by insurance carriers for the entire ACA-compliant individual market. As of this writing, the overall average looks like it's just a hair over 20% across 28 states + DC.

Does the first sentence above include a lot of clarifiers? Yes, yes it does...and with good reason. I try to be very specific when I discuss this stuff, because it's very easy to get confused about what a given number is actually referring to.

For instance, a few days ago, Avalere Health released their own analysis which concludes that the average requested/proposed premium rates are around 12%. If I left it at that, you might think that either my average is 8 percentage points too high...or that Avalere's is 8 points too low.

Thanks to commenter "Junaed S" who directed me towards this simple, cut 'n dry PDF from the Connecticut Dept. of Insurance detailing the requested rate hikes for the CT individual and small group markets for 2017:

In addition, Anthem has decided not to offer its PPO (Preferred Provider Organization) individual plans in 2017. In all, the Colorado Division of Insurance said Monday around 92,000 people with individual plans from Anthem, UnitedHealth, Humana, and Rocky Mountain Health Plans will have to find other coverage during open enrollment in the fall.

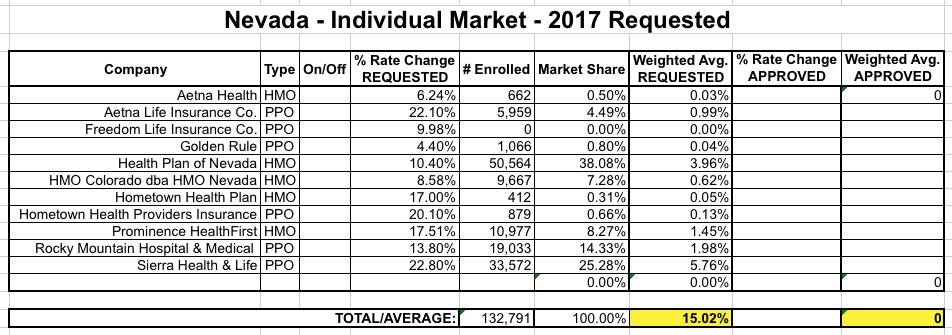

Can I first say that I absolutely love the way Nevada's rate filing database is set up, especially their (apparently proprietary and mandatory) filing format system?

Unlike the standard SERFF database, which is comprehensive but also can be confusing as hell, Nevada's system is simple, clean, easy to navigate and, most of all, every single carrier filing listed displays the number of current enrollees clearly.This is a huge pet peeve of mine, which is understandable given what I'm trying to do here!

OK, that said, here's what things look like in the Silver State:

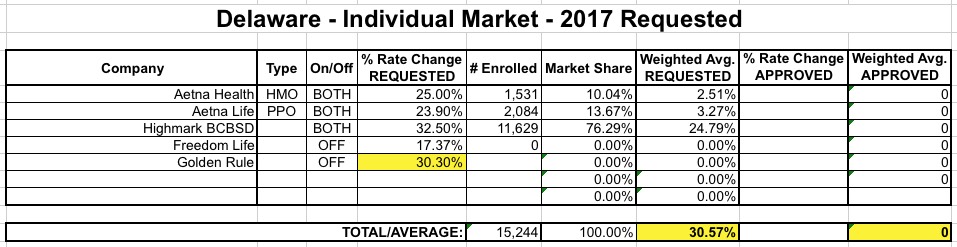

Delaware is a small state, and only has a total of 4 carriers offering individual polcies (2 on exchange, 2 off). One of those, however, is once again "Freedom Life" which, once again, is asking for precisely a 17.37% rate hike on their almost-certain-to-be-nonexistent enrollees. So...never mind them. That leaves Aetna (split into HMOs and PPOs) and Highmark BCBS offering policies on the exchange, and Golden Rule off the exchange.

Unfortunately, I can't find Golden Rule's actual current enrollment number, but as you can see below, it really doesn't matter:

As you can see, no matter how many enrollees Golden Rule has, their 30.3% average hike request is very close to the 30.6% average of the other carriers. The very most it could do is nudge the weighted average down by a tenth of a point or two, so let's call it 30.5%.