NOTE 11/3/15: This post is actually from last spring, but given Marco Rubio's recent climb in GOP primary polling, I figured it was worth dusting off...

NOTE 6/17/16: OK, I'm dusting it off again in honor of Rubio's glorious return to the political scene after his humiliating defeat in the GOP Presidential primary...

Now that Florida GOP Senator Marco "Dry Lips" Rubio has officially launched his 2016 Presidential campaign, my long-time obsession with his ill-fated "Florida Health Choices" project from his days as the Speaker of the FL House has taken on a bit more relevance.

As I recently noted, I actually question the 16 million number; by my count it's actually more realistically like 14-15 million, so there's that.

I also noted in response that the fallout of the plaintiffs winning King v. Burwell will cause a lot more than 5 million people to lose their healthcare coverage. Technically speaking, here's the hard numbers:

"Hello, YouTube. I'm kinda having a difficult decision," Webb lamented in the 3-minute video. "I don't know which party to vote for. ... I don't know whether to go for a Republican or a Democrat -- and I'm serious. Because I asked myself, I said, 'Which party has helped me out the most in the last, I don't know, 15 years? Twenty?' And it was the Repub-, err, Democrat Party. The Democrats."

"I mean if it wasn't for Obama and that Obamacare, I would still be working," Webb continued. "With Obamacare, I got to retire at age 50. Because if it wasn't for Obamacare I would had to work till I was 65 and get on Medicare because health insurance is expensive."

Webb stressed how valuable it was that he'd been able to retire so early and still had health care coverage. He also noted that Obamacare reimburses him for his gym membership.

While this was screaming out as a big red flag, I grudgingly accepted it...only to have the rug yanked out from me when the official ASPE report came out in March, giving the official final number as 12,625...which is right in line with what I was expecting in the first place (around a 50% increase over their total in April 2014, and 17% over their total as of September 2014).

Historically, Medicaid (and to a lesser extent, the CHIP program for children) has carried a certain stigma, since it's traditionally been reserved for the very poor. Many people enrolled the program have been embarrassed/ashamed to admit that they needed the assistance, and many who qualified for the program even under the pre-ACA rules never actually signed up based on the "shame" factor (still others didn't enroll because they simply didn't know that they qualified or didn't understand the procedure/paperwork for doing so).

With that Affordable Care Act, that all changed (well, in the states which expanded Medicaid, anyway). Yes, it's still limited to the poor, but there's a difference between being "dirt poor" and "working poor" (and yes, I understand that many "dirt poor" people work their butts off...I'm talking about general societal perception here). Suddenly, millions of people who considered themselves "lower middle class" (or otherwise "not poor", anyway) found themselves being able to enroll in Medicaid alongside the "dirt poor".

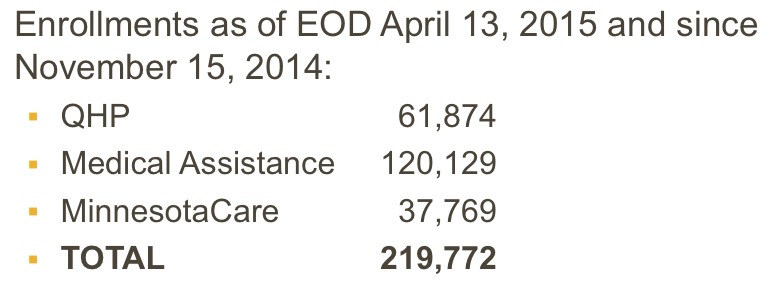

Hmmm...this is a bit surprising. The last report out of MNsure stated that they had added 1,405 QHP selections in the 15 days from 2/21 - 3/08, or 94 per day. I assumed that as today's tax filing deadline approached, this rate would increase as procrastinators scrambled to get their taxes filed under the wire. Instead, however, this is their latest report:

61,874 - 61,109 = Just 765 people enrolling over the 36 days since the prior report, or just 21 people per day. ACA exchange enrollments have actually slowed down substantially over the past month compared to the prior 2 weeks (which were after open enrollment ended). If this slowdown is representative of the whole country, then instead of several hundred thousand #ACATaxTime enrollees, we might be looking at fewer than 100K. However, this isn't nearly enough to draw any conclusions from yet.

So far there have been two comprehensive post-Open Enrollment Period reports released. The first was for Washington State, posted a couple of weeks ago; the second was for Massachusetts, posted last week. While both reports were chock full of all sorts of data-nuggety goodness, including updated paid QHP numbers, neither one included one crucial number: How many total QHP selections there have been in each state since Open Enrollment ended in February.

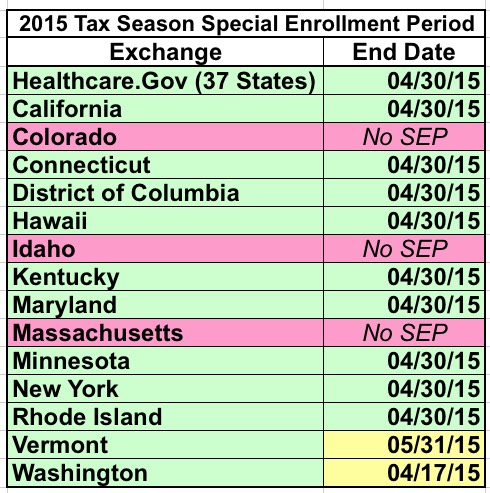

Since today is the official deadline for filing your taxes, I thought it'd be a good time to remind people that if you had to pay the non-coverage tax penalty last year (ie, the "Individual Shared Responsibility Provision"), were (somehow) unaware of it's existence and didn't find out about it until after 2/15/15, you can still enroll in healthcare coverage via the Tax Filing Season Special Enrollment Period (or #ACATaxTime as I put it) as late as April 30th in most states:

As noted above, 3 states aren't offering any sort of tax penalty-specific enrollment period, and 2 other states have different ending deadlines for the SEP: Washington State ends theirs on Friday the 17th, while Vermont is extending theirs all the way out until the end of May.

The ACA is not, by any means, a perfect law. As a single-payer advocate, I find it ironic and a bit absurd that I've received so much praise and attention over the past year and a half for meticulously tracking the enrollment numbers every day...when none of that tracking would even be necessary if we simply shifted to a single-payer healthcare system of some sort. I've made this point before, of course.

Still, the fact remains that the law is generally working, for the most part, and while parts of it are pretty confusing, there are some parts which quite simply aren't. Yes, the law should be as easy to understand as possible. Yes, there are plenty of situations where the government, the insurance companies, the exchange personnel, the brokers/navigators or even the hospitals/doctors are to blame for errors, but I'm not addressing any of those cases here.

However, at the end of the day, the actual enrollees do need to take some bare-minimum level of personal responsibility for their decisions.

Yeah, I know, this is the 3rd off-topic post I've made in as many days, but it's kind of a slow week and I'm procrastinating on my day job at the moment. Besides, this is kind of nagging at me.

Hillary Clinton's new campaign logo (the "Arrow-H" or whatever) has been the subject of way too much discussion already, but I'm a website developer (if not really a graphic designer) so I can get away with it to a point.

The other day I noted that the only major issue I have with it is that mashing the primary red & blue colors up against each other is always problematic because those colors tend to bleed into each other (either literally on a print job or figuratively when you're looking at them). It's not Hillary's fault that the U.S. flag happens to include 2 colors that clash, but it is what it is.

My suggestion was to simply add a thin white border around the arrow to add some space between the blue and red, but I didn't actually do so; here's how that looks, and I think that just this simple tweak improves it tremendously: