If you look at The Graph lately, you'll notice that in addition to extending the projections out for the full calendar year, I've also recently added the Effectuated Enrollment line, which hovers around the 10.0 - 10.1 million enrollee mark for most of the year.

I've explained this several times before, but with the recent confirmations from states like Idaho and Massachusetts that the 2015 payment rate is likely higher than the 88% "rule of thumb" that I've been using for nearly a year now, yesterday's data showing that the #ACATaxTime enrollments appear to be roughly 3,000/day nationally (I overestimated by a lot), and today's confirmation out of California that my estimate of at least 7,000 additional QHP selections per day during the "normal" off-season is likely underestimating things a bit, it seems like a good time to modify things.

With that in mind, here's 2 tables which lay out how I expect the rest of 2015 ACA exchange enrollments and attrition to play out. The first table assumes that 88% of enrollees pay their 1st premium; the second table assumes 90%. Other than that, both are identical and assume:

Sally Pipes, according to her byline in Forbes, is the President of the Pacific Research Institute (another one of those "free market think tanks" along the lines of the American Enterprise Institute, Heritage Foundation, bla bla bla).

I want to be clear about this up front: I have no problem with private insurance exchanges (at least no moreso than I have a problem with private, for-profit health insurance in general). Companies such as eHealth Insurance and it's brethren are perfectly fine, and I wish them well.

Having said that, Ms. Pipes has written an unbelievably disingenuous essay. Let's take a look, shall we?

The federal government is desperate for Americans to enroll in Obamacare’s exchanges. But most people have refused.

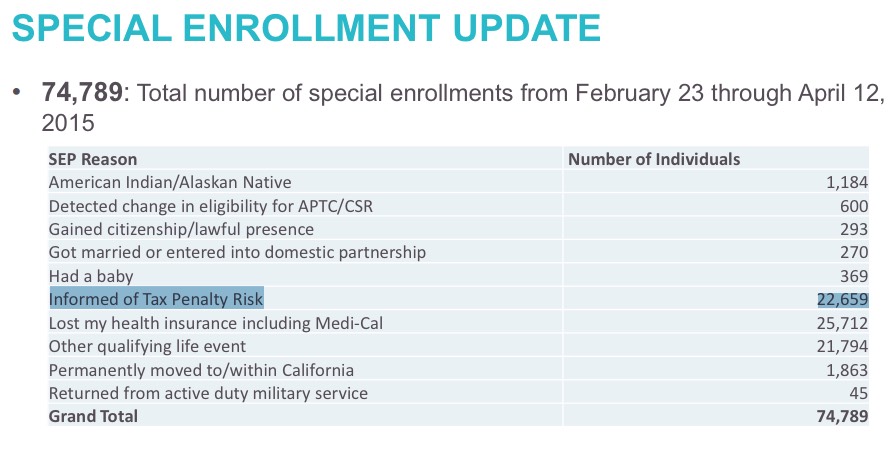

A huge thank you to Hannah Recht for the link to last week's Covered California board meeting dashboard report, which contains this crucial slide:

This is incredibly useful! Not only have they given an updated #ACATaxTime tally (22,659 as of 4/12, up from 18,000 as of 4/05), but they've also given the other off-season QHP enrollments for California since Open Enrollment ended. As a bonus, they've even broken out those other QHPs by the specific reason, which is a first for any exchange report, I believe!

Earlier I posted about a new Bloomberg News poll which shows that only 35% of the population wants to repeal the ACA, while 63% want to either keep it as is or give it a few years to see how it goes with only minor tweaks.

As you'll recall, in every state but 3 (CO, MA & ID), the ACA exchanges are allowing people who a) had to pay the "shared responsibility penalty" last year; b) missed the 2/22 deadline for enrolling in healthcare coverage this year and c) "didn't know" about the penalty until after the deadline (honor system!) were given a roughly 6-week period to go ahead and enroll for the rest of 2015.

A couple of weeks back I reported that I had seriously overestimated the number of people who were likely to take advantage of the ongoing tax filing season Special Enrollment Period, which I've shortened to #ACATaxTIme. The time window for most states is from 3/15/15 - 4/30/15, although a few states started a bit earlier/later.

I had made a very rough "spitball" guess that perhaps somewhere between 600K - 1.2 million people might select exchange policies during this SEP, based on extremely vague information about just how many people actually qualified.

A few months later, I again laid into her for a rather lame "Obamacare Raised My Rates 36x!!" tweet that she sent out which, while not actually proven false, certainly didn't include any supporting evidence, details or context whatsoever.

Apparently the answer to the question "How many times will they vote to repeal the ACA before giving it up already?" is "67" (or in the mid-50's, depending on your definition).

After five years and more than 50 votes in Congress, the Republican campaign to repeal the Affordable Care Act is essentially over.

GOP congressional leaders, unable to roll back the law while President Obama remains in office and unwilling to again threaten a government shutdown to pressure him, are focused on other issues, including trade and tax reform.

Less noted, senior Republican lawmakers have quietly incorporated many of the law's key protections into their own proposals, including guaranteeing coverage and providing government assistance to help consumers purchase insurance.

And although the law remains very unpopular with GOP voters, more than 20 million Americans now depend on it for health benefits, making even some of the most conservative Republicans loath to cut off coverage.

Thanks to Jesse LaGreca for the heads up on this piece of idiocy from The Daily Signal, aka "One of the heads of the Heritage Foundation Hydra":

Forcing States to Recognize Gay Marriage Could Increase Number of Abortions

In a nutshell: A reduction in the opposite-sex marriage rate means an increase in the percentage of women who are unmarried and who, according to all available data, have much higher abortion rates than married women. And based on past experience, institutionalizing same-sex marriage poses an enormous risk of reduced opposite-sex marriage rates.

So, my family finally got around to watching Monsters University, the completely unnecessary prequel to Monsters, Inc. Thoughts:

--It was actually a lot better than I was expecting. No, it's not in the upper echelon of Pixar's library, but it's a solid addition. I'd rank it about 10th out of the 14 Pixar movies to date (below Ratatouille and WALL-E, but above Brave, A Bug's Life, Cars or Cars 2).

--Pixar's biggest problem these days is twofold: First, they set the bar so high with masterpieces such as Toy Story 2 & 3, Finding Nemo, The Incredibles, Finding Nemo and Up that when they make a movie that's "merely" very good it seems "disappointing" by comparison.

At the same time, when Pixar was kicking ass and taking names, they also had very little serious competition; the other studios tried to ape Pixar technically, but without having the storytelling/character/dialogue chops. That's changed over the past few years, however; movies like How to Train Your Dragon, Tangled, the Lego Movie, (the first) Despicable Me, (the first) Ice Age and Wreck-It Ralph have proven that the other studios have seriously upped their game. That's good for everyone, but it also ups the ante further for Pixar these days.