Christopher Koller, president of the Milbank Memorial Fund, recently provided a SHOP exchange enrollment summary in written testimony submitted for a state legislature hearing in Hawaii.

Out of curiosity, I took a look at his presentation, hoping to find some updated numbers out of Hawaii (I don't have anything for the Aloha State since 2/21). Instead, on 3 different slides, I found...ACASignups.net listed as a data source.

Yup, I've now been repeatedly cited in an official presentation to a Joint Committee Meeting of the Hawaii State Legislature.

The numbers are in: It appears that Oregon consumers were fairly price sensitive when it came to choosing health plans this year.

LifeWise had the lowest rates, at $222 a month for a 40-year-old Portlander on a silver plan. Probably not coincidentally, it more than doubled its individual membership in plans that comply with Affordable Care Act guidelines.

As of March 31, LifeWise has nearly 37,000 members in ACA-compliant plans, up from 4,735 last year, according to the Oregon Insurance Division.

The article goes on to tally every single one of Oregon's individual policy QHP enrollees. The bad news is that they don't break them out by exchange vs. off-exchange. The good news is that they specifically clarify that these are all ACA compliant policies (ie, no "grandfathered" or "transitional" numbers included):

Last year, after a bunch of different piecemeal data points and surveys came in, I estimated off-exchange (that is, directly via the insurance companies) private insurance policy enrollments were likely around 8 million or so, of whom perhaps 7 million paid at least their first premium, plus another 4-5 million or so "grandfathered" or "transitional" enrollments. Add these to the 7 million (paid) exchange-based enrollees and you had perhaps 18-19 million people on the private individual market for 2014.

This year, I actually have less hard off-exchange data to work with so far (only a handful of states), but since early February I've been operating on a rough estimate of around 80%. That is, whatever the exchange-based QHP figure is at any given time, I'm pretty sure that the off-exchange QHP tally is somewhere around 80% of that number.

If you look at The Graph lately, you'll notice that in addition to extending the projections out for the full calendar year, I've also recently added the Effectuated Enrollment line, which hovers around the 10.0 - 10.1 million enrollee mark for most of the year.

I've explained this several times before, but with the recent confirmations from states like Idaho and Massachusetts that the 2015 payment rate is likely higher than the 88% "rule of thumb" that I've been using for nearly a year now, yesterday's data showing that the #ACATaxTime enrollments appear to be roughly 3,000/day nationally (I overestimated by a lot), and today's confirmation out of California that my estimate of at least 7,000 additional QHP selections per day during the "normal" off-season is likely underestimating things a bit, it seems like a good time to modify things.

With that in mind, here's 2 tables which lay out how I expect the rest of 2015 ACA exchange enrollments and attrition to play out. The first table assumes that 88% of enrollees pay their 1st premium; the second table assumes 90%. Other than that, both are identical and assume:

Sally Pipes, according to her byline in Forbes, is the President of the Pacific Research Institute (another one of those "free market think tanks" along the lines of the American Enterprise Institute, Heritage Foundation, bla bla bla).

I want to be clear about this up front: I have no problem with private insurance exchanges (at least no moreso than I have a problem with private, for-profit health insurance in general). Companies such as eHealth Insurance and it's brethren are perfectly fine, and I wish them well.

Having said that, Ms. Pipes has written an unbelievably disingenuous essay. Let's take a look, shall we?

The federal government is desperate for Americans to enroll in Obamacare’s exchanges. But most people have refused.

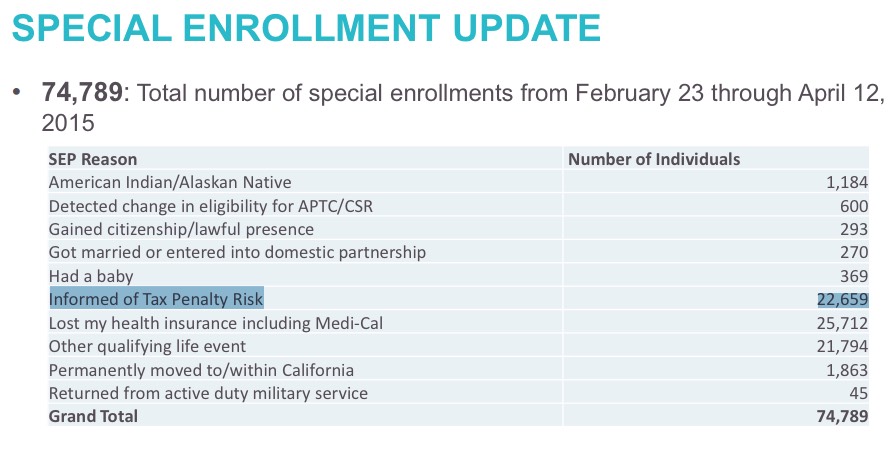

A huge thank you to Hannah Recht for the link to last week's Covered California board meeting dashboard report, which contains this crucial slide:

This is incredibly useful! Not only have they given an updated #ACATaxTime tally (22,659 as of 4/12, up from 18,000 as of 4/05), but they've also given the other off-season QHP enrollments for California since Open Enrollment ended. As a bonus, they've even broken out those other QHPs by the specific reason, which is a first for any exchange report, I believe!

Earlier I posted about a new Bloomberg News poll which shows that only 35% of the population wants to repeal the ACA, while 63% want to either keep it as is or give it a few years to see how it goes with only minor tweaks.

As you'll recall, in every state but 3 (CO, MA & ID), the ACA exchanges are allowing people who a) had to pay the "shared responsibility penalty" last year; b) missed the 2/22 deadline for enrolling in healthcare coverage this year and c) "didn't know" about the penalty until after the deadline (honor system!) were given a roughly 6-week period to go ahead and enroll for the rest of 2015.

A couple of weeks back I reported that I had seriously overestimated the number of people who were likely to take advantage of the ongoing tax filing season Special Enrollment Period, which I've shortened to #ACATaxTIme. The time window for most states is from 3/15/15 - 4/30/15, although a few states started a bit earlier/later.

I had made a very rough "spitball" guess that perhaps somewhere between 600K - 1.2 million people might select exchange policies during this SEP, based on extremely vague information about just how many people actually qualified.

A few months later, I again laid into her for a rather lame "Obamacare Raised My Rates 36x!!" tweet that she sent out which, while not actually proven false, certainly didn't include any supporting evidence, details or context whatsoever.