Just now, the MD Health Connection posted an update through this week:

Incoming exec director Michele Eberle of @MarylandConnect urges Marylanders to enroll in health coverage with 10 days left. New enrollments up 14% this year. Mobile app visitors up 140% Overall enrollment up 4% Keep it going! pic.twitter.com/75g2qu5PbC

I'm assuming these stats are as of December 4th. Last year MD's official QHP selection tally as of December 3rd was around 129,000; if they're 4% ahead of that as of the same date, that means they should have a little over 134,000 to date this year.

So @SenatorCollins sold out for bills which won’t help much and aren’t gonna happen anyway.@jeffflake sold out for a promise to attend a meeting which won’t happen.@lisamurkowski sold out for destroying her own environment.@SenJohnMcCain sold out for...nothing at all. Huh.

As I had previously noted, the Alexander-Murray bill would simply restore CSR funding into place which was already assumed to be there when the CBO made their "13 million losing coverage/10% rate hike" projection earlier, making passing it kind of a non-factor when it comes to the impact of repealing the mandate. That just left the reinsurance bill. Collins original proposal was a mere $2.25 billion/year (and only for two years at that)...which I estimated would fall short by a factor of anywhere from 3x to 7x, depending on which back-of-the-envelope math you use:

So one of the Big Deals on Twitter this morning was this tweet by Republican(correction: Former Republican) MSNBC talking head Joe Scarborough:

.@SenOrrinHatch talking about children's health care: “I have a rough time wanting to spend billions and billions and trillions of dollars to help people who won’t help themselves – won’t lift a finger – and expect the federal government to do everything.”

...which caused an immediate and understandable backlash uproar, including my own tweet (since deleted),

Holy crap. They're CHILDREN. Plus...didn't he used to brag about helping CREATE the CHIP program in the first place?

I hadn't actually seen the full clip at the time. My own tweet went semi-viral, with several hundred RTs and a bunch of Likes within a couple of hours.

However, shortly after that, Bloomberg reporter Steven Dennis correctly noted that...

It's not over yet, since the House of Representatives still has to vote on the bill again (either as is, or after hashing out the differences between the House and Senate versions of the bill), but assuming the final version of the bill includes mandate repeal and is indeed signed into law, this is what the ACA's 3-legged stool would look like when the dust settles.

Obviously I'll have much more to say about what happened last night soon, but for the moment I'll leave it at this.

Kelly said about 90,000 people were insured through the exchange at any given time this year. (People could enroll or cancel during the year.) And at the end of last year’s open-enrollment period, more than 100,000 were signed up for coverage.

This month, the exchange has renewed 86,300 customers for 2018 plans. The new sign-ups are much lower, in the hundreds. Kelly said total enrollment so far — 2017 customers being rolled over into 2018, plus the new sign-ups — exceeds 87,000.

“That number has grown every day in the last several weeks,” he said.

Less than 10 percent of people who were auto-renewed for 2018 plans have canceled so far, he said. More people could cancel by the deadline, though; last year, almost 30 percent of auto-renewed plans had been canceled when the dust settled on the enrollment period.

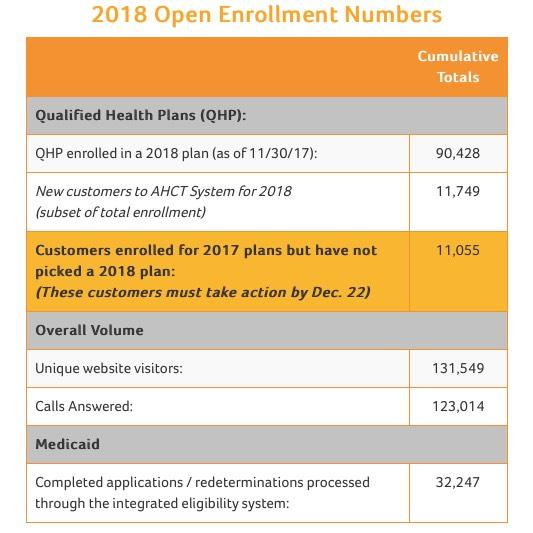

They've also done something interesting: They're listing the 11,055 current enrollees who haven't actively re-enrolled as of yet. If every one of them did so (they won't), that would bring the grand total up to 101.4K.

Connect for Health Colorado® Reports Increase in 2018 Medical Plan Selections

DENVER — More than 43,000 Coloradans selected healthcare coverage for 2018 through the state health insurance Marketplace in November, a rate 29 percent ahead of signups one year ago, according to new data released today by Connect for Health Colorado®.

“With only two weeks left to enroll for January coverage, I am pleased with the pace of plan selections,” said Connect for Health Colorado CEO Kevin Patterson. “I know people are busy this time of year but I encourage everyone who buys their own health insurance to check to see if they qualify for financial assistance, review the available plans, and complete an enrollment before the last-minute rush. Many will be surprised that they qualify for financial help.”