Over the past week or so there was a lot of tense negotiations and confusion about whether or not ConnectiCare, the 2nd largest carrier on Connecticut's exchange and the largest in CT's individual market overall, would bail on participating on AccessHealthCT next year. They bumped up their rate hike request not once but twice, from 14.3% to 17.4% to 27.1%, and when state regulators stuck with 17.4% and refused to budge any higher, they threatened to file a lawsuit and drop out of the exchange. As of last Friday, it looked like they were indeed pulling out.

Days after declaring it would leave the state’s health insurance exchange, ConnectiCare has decided not to drop out of the marketplace, much to the relief of many — including Gov. Dannel P. Malloy.

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

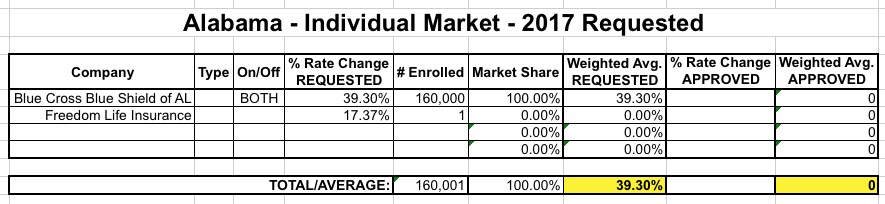

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

As noted by Nicholas Bagley, Richard Mayhew and myself several times over the past year, Marco Rubio's Risk Corridor Massacre, which cut the ACA's risk corridor program off at the knees back in December 2014, has caused a tremendous amount of damage to the country in the form of helping kick 800,000 people off their healthcare policies, putting several hundred people out of work and could potentially cost taxpayers several billion dollars more than it would have cost if the program hadn't been interfered with in the first place...for no reason whatsoever. Rubio can't even argue that it was worth it for his own personal gain, since his stunt didn't even gain him the Republican Presidential nomination.

I know, the headline is clickbait, but hear me out; lemme play Devil's Advocate for a moment here.

Last week, when writing about Phoenix Health Plans becoming the latest carrier to drop out of the Arizona exchange, I noted that...

Ironically, this may prove to have a silver lining, according to one expert:

If Cigna decides to stick with the exchange marketplace, it will have access to a solid mix of healthy and unhealthy patients, said Jim Hammond, publisher of the Hertel Report.

"The first question is, will Cigna stay in," Hammond said. "If Cigna bails, then we have a real problem and the state and federal officials are going to have to figure out what to do about it. They've made this mandate and there's no way for people to actually meet the mandate."

Once an insurance carrier gets a decent mix of healthy and unhealthy patients, and targets the unhealthy patients with special programs, then it should be fine, he said.

I didn't really make a big thing out of it, but thought it was an interesting perspective.

The Massachusetts Health Connector has posted their latest monthly enrollment report (through the end of August), and the news is good. As I note every month:

Unlike most states, the Massachusetts Health Connector has not only seen no net attrition since the end of Open Enrollment, but has actually seen a net increase in enrollment...mainly due to their unique "ConnectorCare" policies, which are fully Qualified Health Plans (QHPs) but have additional financial assistance for those who qualify and which are available year-round instead of being limited to the open enrollment period.

The amount of the increase depends on which "official" number you start with; the MA exchange claimed 196,554 people as of 1/31/16...while the ASPE report gives it as 213,883 as of the next day....yet their March report claims 208,000 effectuated enrollees as of February.

In light of Hillary Clinton's "half of Trump supporters belong in the racist/bigot basket" brouhaha, I figured since I'm known as a data/numbers guy, let's do some quick math:

Taking Clinton's "half" literally (which is of course unbelieveably silly), that's 50% of his supporters, or around 32.2 million registered voters.

32.2 million / 324 million = appx. 10% of the total U.S. population.

In other words, if you take Hillary Clinton's statement literally, she's effectively saying that 10% of the U.S. population is racist.

This is hardly a controversial statement.

If you turn that around, the real reason Trump supporters are getting all bent out of shape this morning (hey, I thought they hated it when people are too "PC"!) isn't so much that Hillary said that a lot of Trump supporters are racist...it's because she (effectively) said that pretty much all racists are Trump supporters.

The cost of health insurance plans offered under the Affordable Care Act will jump 20 percent or more next year under rates to be announced Friday by Maryland regulators.

His remarks came as the Maryland Insurance Administration approved double-digit rate increases for the four companies that sell health plans through the state exchange, an online marketplace set up under the law for people who cannot buy coverage through their employer.

...CareFirst, which holds 68 percent of the market, received an average hike of 31.4 percent on its PPO plan and 23.7 percent on its HMO — the highest increases of any insurer.

...Rates in Maryland also have been typically lower than those nationally under the Affordable Care Act, so there could be some normalizing going on, said John Holahan, a fellow in the Urban Institute's Health Policy Center.

"Maryland rates have been lower than the rest of the nation so it seems some catching up should be expected," said Holahan.

Over the past few days I've been doing some serious number-crunching in an attempt to break out the entire individual market between exchange-based, ACA-compliant off-exchange, grandfathered and transitional plans. For the most part, I believe most of my data is pretty close...but there's still some pieces of the puzzle missing here and there.

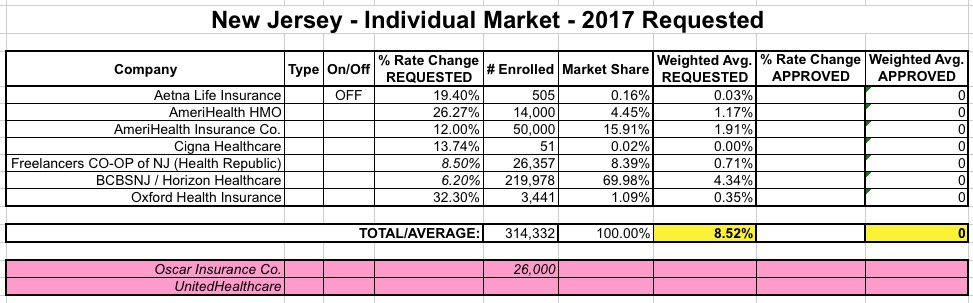

For New Jersey, my current numbers (as of March 2016) are: