Today (Friday, Sept. 23) happens to be the deadline for insurance carriers to sign agreements with the federal government for participating in the exchange this Open Enrollment period (I'm not sure if today's deadline also applies to the state-based exchanges or not; they might be different). Until today, it looked as though there were going to be 3 carriers offering individual policies on the Nebraska exchange:

The figures compared 2016 and 2017 rates for Blue Cross Blue Shield of Nebraska, Aetna Health Inc. and Medica, the three companies that will offer policies to Nebraskans on the exchange when open enrollment starts Nov. 1.

However, as commenter M E noted, it looks like BCBSNE decided to wait until literally the last minute (last hour, anyway) to change their minds:

A couple of days ago, I noted that the latest development in House v. Burwell (the lawsuit brought by former Republican House Speaker John Boehner on behalf of the GOP caucus in the House of Representatives) could, in a worst-case scenario, end up resulting in millions of exchange-based policies being terminated with little notice. Basically, the HHS Dept. has included an "escape hatch" for exchange carriers in the event that the Supreme Court eventually rules in favor of the GOP House when it comes to Cost Sharing Reduction (CSR) financial assistance, although a final ruling wouldn't be likely to happen for at least another year or so.

Today, Michael Cannon of the Cato Institute has posted his own entry about the HvB "escape hatch" development, and while it obviously has an extremely anti-ACA spin, his conclusion is pretty much the same as mine (he assumes all 11 million enrollees would be kicked off their plans, while various state/federal laws could mean a much smaller percentage...but it would be pretty devastating no matter what).

Back in March, Bruce Japsen and Andrew Sprung noted that regardless of the financial woes many carriers are having on the individual market under the ACA, many of those same carriers are raking in big bucks in other divisions...particularly managed Medicare and Medicaid:

A snapshot of health insurers’ Medicaid windfall under the ACA could be seen in the earnings reports of Wellcare Health Plans (WCG) and Centene CNC +0.20% (CNC), which both beat Wall Street’s fourth quarter 2015 earnings expectations. These companies are an important measure of whether health insurers can find financial success providing Medicaid coverage to poor Americans under the health law President Obama signed six years ago even as the other key part of the legislation has growing pains.

Larger plans like Aetna AET +1.51% (AET), Anthem ANTM +1.31% (ANTM) and UnitedHealth Group UNH +1.08% (UNH) are also doing well in the Medicaid business, but their overall profit margins have been somewhat negatively impacted due to the private coverage on the exchanges.

For the two carriers that are expected to participate in the exchange in 2017, the proposed average rate hikes for 2017 are:

Blue Cross Blue Shield of North Carolina: 18.8 percent 24.3 percent (new rates were filed in late August)

Cigna: 7 percent (based on current off-exchange plans) 15 percent (new rates were filed)

Aetna had proposed an average rate increase of 24.5 percent, but that is no longer applicable for exchange enrollees, as Aetna’s plans will not be available in the North Carolina exchange in 2017.

First, it sounds like ConnectCare (the largest carrier on the CT exchange) is jumping on the "standardized plan" bandwagon, by offering what they call "Passage" exchange plans:

HMO-style, $5 co-pay for Primary Care Physician (PCP) visits (pre-deductible)

The Silver "Passage" plan would have a flat $50specialist co-pay

High-quality PC network included

Simple/easy to understand standardized plans

also offering "Passage" plans to small group / Medicare enrollees

--Standardized plans help but not enough; still lots of confusion about process, what's included/not included, etc; launching 4 retail "ConnectiCare Centers" to help people shop, enroll, member services, billing/payment issues, health/wellness assessments, education/outreach events

--CliniSanitas: Multicultural health delivery for hispanic/etc. members (3 centers; 100% bilingual services)

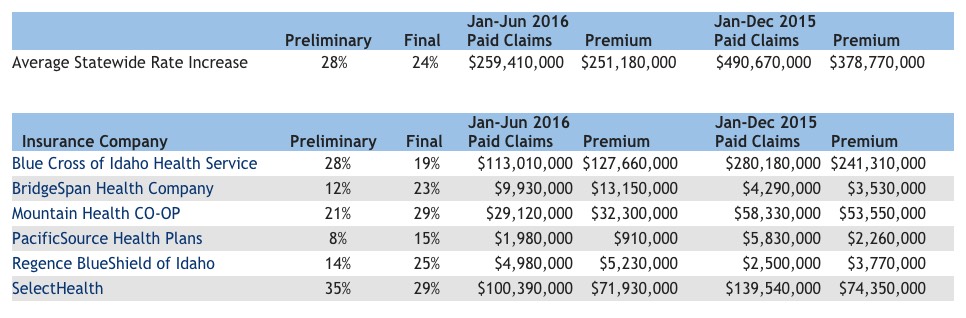

The final rate approvals for the Idaho indy market are either positive or negative, depending on your POV. On the one hand, the statewide weighted average is roughly 24%. On the other hand, this is 4 points lower than the 28% requested average from the carriers. As I noted in June, Idaho is among the only states which also posts exactly how much each carrier earned in premiums and paid out in claims for both last year and this year to date, giving some insight into which carriers are making a profit or taking a loss on the indy market:

Over at Investor's Business Daily, Jed Graham has crunched some IRS numbers to determine just how many people ended up paying the ACA's dreaded "Shared Responsibility" mandate penalty this year. It's a pretty negative piece, as you'd expect, but I'm mostly interested in the actual numbers, of course:

Yet the IRS Taxpayer Advocate Service included some preliminary statistics on 2016 ObamaCare mandate payments, officially called the Individual Shared Responsibility Payment, when it issued its below-the-radar annual tax season review on July 7. As of April 30, 5.6 million tax returns included mandate payments averaging $442 per return, compared with 6.6 million tax forms including average payments of $190 at the same point in 2015.

More recent data from the IRS wrapping the past tax year show that the final tally for 2015 ObamaCare Mandate fines included payments on 8.1 million tax returns averaging $210 for a total of $1.7 billion.

In addition to the ACA providing "APTC" tax credits to those who qualify, the ACA also provides "CSR" (Cost Sharing Reduction) assistance to those who a) are under 250% FPL and b) enroll in Silver exchange plans.

The CSR payments don't actually go directly to the enrollee; instead the insurance carriers cover the appropriate chunk of deductibles/co-pays, with the CSR funds going to reimburse the carriers.

Former House Speaker, Republican John Boehner, sued the HHS Dept. and the Obama administration over CSR appropriations, claiming that since Congress never specifically appropriated funding for CSR payments, it's illegal for the HHS Dept. to reimburse the carriers.

So far, the federal judge in the case has sided with the House Republicans, although the case is still winding it's way up the ladder, presumably to eventually end up at, yes...the Supreme Court of the United States (which has to be sick to death of being dragged into the middle of Obamacare yet again)

For the moment, the CSR assistance/reimbursements continue to flow...but if they were to be cut off, the insurance carriers would still be legally required to keep paying out CSR assistance, even though they wouldn't be reimbursed by the HHS Dept.

This would result in the carriers either a) filing potentially millions of lawsuits to get legally-mandated reimbursements for each individual CSR claim, which would clog up the courts, or, more likely, b) it would result in the carriers basically saying "screw this, I'm just gonna jack up rates by $1,000 a pop to cover my CSR losses".

However, due to a quirk in how the metal levels and CSR rules work, only Silver plans (the ones with CSR) would have their rates increase...meaning that Gold plans could end up costing less than Silver, which would just confuse the hell out of everyone.

Every once in awhile I remember what I actually do for a living (I'm a website developer, for those who don't know). That's actually a major reason I started this project in the first place...the techical meltdown of HealthCare.Gov and many of the state-based exchange sites in October 2013 fascinated me, leading me to start trying to assess just how many people were actually enrolling in the plans using the messy websites, and it spread from there.

Since then, of course, most of the exchange sites have been vastly improved. HealthCare.Gov is literally 100,000x better than it was in 2013 (while also now being considered among the most secure major consumer websites in the world), and has completely overhauled and streamlined their user interface and workflow process (cutting the number of screens for creating an account from around 80 down to 16). They've also added some nifty features like their Expected Total Cost, Network and Formulary tools.

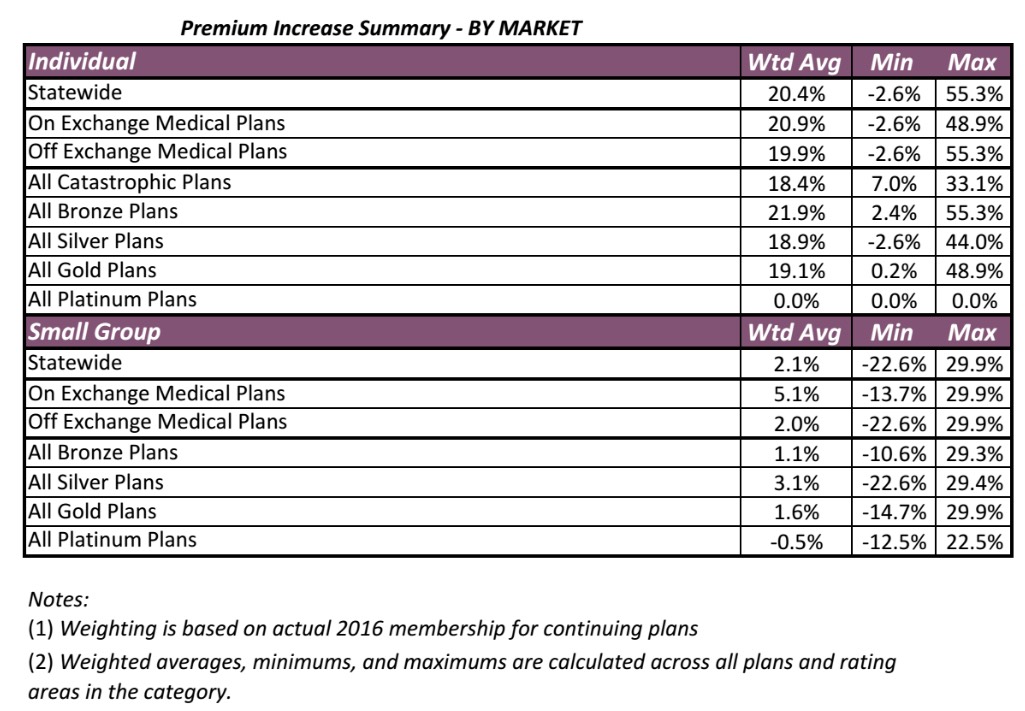

Well, today the Colorado Dept. of Insurance released their approved rate hikes for both the individual and small group markets. Unfortunately, I don't see an actual carrier-by-carrier breakout, but they do provide weighted averages by other criteria such as metal level, on exchange vs. off exchange and so on:

While it would be nice to have the averages weighted by carrier, the on/off breakout is kind of interesting because it also lets me know what the relative numbers are between the two. For the individual market, note that the on exchange weighted average is 20.9% vs. the off-exchange's 19.9%.