Utah has also finally released their requested 2018 individual market rate increases. There are six carriers offering individual policies next year, but only 2 of them are participating on the ACA exchange (and the 4 off-exchange carriers hold less than 4% of the total market combined). In fact, two of the off-exchange-only carriers are barely participating at all: BridgeSpan has only 8 enrollees, while "National Foundation" (a "phantom carrier" which also goes by "Freedom Life" in other states) once again supposedly only has a single "enrollee". Molina has a few hundred off-exchange enrollees, but the bulk of their 70,000-person membership are in exchange-based policies, and they're dropping off the exchange next year, so those 70K will have to choose from one of the two remaining exchange carriers: SelectHealth and the University of Utah.

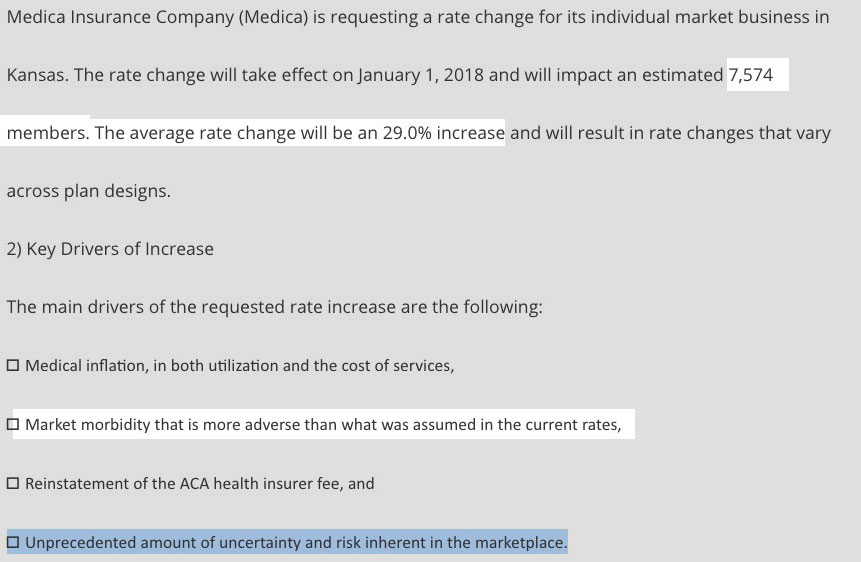

As I noted back in June, there are 3 carrers on the KS individual market this year: Medica, Blue Cross Blue Shield of Kansas Solutions and Blue Cross Blue Shield of Kansas City. Any confusion between the BCBS names was made moot, however, as BCBS of KC announced they were dropping out of the indy market anyway.

That leaves Medica and BCBSKS, both of whom filed plans to stay on the market...but only Medica appears to have actually submitted rate requests, for a mere 7,600 enrollees:

ACA Signups isn't normally known for "big scoop" stories. Yes, I'm often the first one to openly post analysis and/or debunking of information/data/claims which have already been made public, but I'm not usually the first one to actually make the underlying data itself public in the first place.

I've confirmed the veracity of these documents, and the claims related to them seem to be on the level.

According to my source, these are signed orders instructing the grant awarding officer to distribute $60,000,000 in grants with an effective date and time of August 31st, first thing in the morning.

My 2018 Rate Hike project petered out a few weeks back with the requested rate increases posted for 46 out of 50 states (along with DC). Unfortunately, the last 4 states (Kansas, Missouri, Nevada and Utah) decided to keep their cards close to their chest, delaying any public viewing of even the requested rate increases for awhile longer.

Lori Lodes used to be Communications Director for the Centers for Medicare & Medicaid until last year under President Obama. As such, a big part of her job was administering ACA outreach efforts.

Trump is slashing Obamacare’s advertising budget by 90 percent

The White House will also cut the in-person outreach program by $23 million.

The Trump administration plans to deeply cut Obamacare outreach and advertising, officials announced Thursday.

Trump will reduce Obamacare advertising spending 90 percent, from the $100 million that Obama administration spent last year to $10 million this year. It will also cut the budget for the in-person enrollment program by 39 percent.

Administration officials cited “diminishing returns” from outreach activities. In a phone call with reporters, they said that most Americans already know about the Affordable Care Act.

The effort was spearheaded by Republican John "Yeah, he's definitely primarying Trump in 2020" Kasich of Ohio and Democrat John Hickenlooper of Colorado, but also includes Brian Sandoval (GOP, NV); Tom Wolf (Dem, PA); Bill Walker (Indy, AK); Terry McAuliffe (Dem, VA); John Bel Edwards (Dem, LA); and Steve Bullock (Dem, MT).

Here's a partial version of the letter with the meat of the asks:

A Trump administration official said Wednesday that the administration wanted to stabilize health insurance markets, but refused to say if the government would promote enrollment this fall under the Affordable Care Act or pay for the activities of counselors who help people sign up for coverage.

The official also declined to say whether the administration would continue paying subsidies to insurance companies to compensate them for reducing deductibles and other out-of-pocket costs for low-income people. Without the subsidies, insurers say, they would sharply increase premiums.

The administration, the official suggested, will do the minimum necessary to comply with the law, which Mr. Trump has called “an absolute disaster” and threatened to let collapse.

State officials increasingly worry that this year’s turbulent health-care politics could threaten funding for the Children’s Health Insurance Program, a popular initiative that usually wins broad bipartisan support.

Federal funding for CHIP is set to end Sept. 30. The federal-state program provides health coverage to more than eight million low-income, uninsured children whose family incomes are too high to qualify for Medicaid.

When I last checked in on Maryland's individual market rate hikes for next year, the picture was pretty grim: Overall requested increases of around 46%...and that assumed that CSR reimbursements are made in 2018. If you assume CSRs aren't paid, it looked even worse: A whopping 57% average increase statewide for unsubsidized enrollees. Ouch.