As I noted last month with my "Silver Switcharoo" explainer, for carriers which remain in the ACA exchanges next year, there's three potential scenarios which could happen (well, four, actually, if you include "Congress manages to sneak a full CSR appropriation bill into law just under the wire", although that seems pretty unlikely at this point given the time crunch and the fact that it'd need a 2/3 majority in both the House and Senate to avoid being vetoed by Trump anyway):

Quick recap: As of 2013, the pre-ACA individual market consisted of around 10.7 million people. The vast majority of the policies these folks were enrolled in were not ACA-compliant for one reason or another, including not covering one or more of the 10 Essential Health Benefits (EHBs) required by the ACA, having annual/lifetime caps on benefits or any number of other reasons.

Under ACA regulations, non-compliant policies which people were enrolled in prior to March 2010 (when President Obama signed the ACA into law) were grandfathered in...that is, insurance carriers could continue to offer them to existing enrollees for as long as they wanted to, and existing enrollees could stay on them for as long as they wished, but they couldn't be offered to anyone else, and once a current enrollee dropped out of a grandfathered plan they aren't allowed to rejoin it later on. The number of "grandfathered" enrollees has gradually declined since 2013, of course, as people either move to other coverage, die off (hey, it happens) or the carriers decide to discontinue the policies altogether.

Back in early June, the New York Dept. of Financial Services posted the requested 2018 rate hikes for the individual and small group markets. In most states, the CSR reimbursement issue is a much bigger factor than whether or not the Trump Administration enforces the individual mandate, but in New York it's the exact opposite: According to the NY DFS, loss of CSR payments would only tack on 1.3 points to the total, while "a full repeal of the federal individual mandate would increase rates by an additional 32.6%".

The reason for the fairly nominal CSR factor is that the vast majority of NY's CSR-eligible population (those earning 138-200% FPL) is instead enrolled in the state's Basic Health Program. As a result, only 26% of New York's exchange enrollees receive CSR assistance, and the 200-250% FPL recipients only receive a fairly skimpy amount of CSR help anyway. At the opposite end of the spectrum, the 32-point mandate factor is far higher than most carriers are indicating (more like 4-5 points), but there's a big difference between the administration "not enforcing" the penalty and outright repealing it, which NY DFS is talking about.

In any event, this means that NY's requested average increases boiled down to: 15.0% if CSRs are paid/mandate enforced, 16.6% if CSRs aren't paid/mandate is enforced, or a whopping 50.5% if CSRs aren't paid and the mandate was repealed.

OK, perhaps this is just me being paranoid, but then again, given the #TrumpRussia/Hacking brouhaha, perhaps not.

Like most website owners, now and then I like to check my website analytics to see how the site is doing traffic-wise. Every now and then I'll poke through the various demographics of site visitors. Once in a blue moon I'll even check which country people are visiting from. Given the nature of this site, obviously the vast majority of the traffic comes from the United States; after that, most visitors typically come from Canada, the United Kingdom or France, none of which is particularly surprising.

However, I noticed something interesting today, and decided to go back to prior years to check on something...and sure enough, guess what?

As I noted earlier today, there’s a gazillion ways the Trump Administration could sabotage (and in some cases, is already sabotaging) the 2018 Open Enrollment period this fall, doing everything in their power to dampen, obstruct and otherwise minimize the number of people who actually enroll in a healthcare policy via the federal ACA exchanges.

However, as I've noted before (and as the CBO confirmed last week), due to the confusing, inside out way in which the APTC and CSR subsidy formulas happen to work, there's also the potential for one of the most pressing sabotage schemes by Trump and the GOP to backfire completely, leading to the potential for a significant increase in ACA exchange enrollment.

I've noted before that even if the Trump Administration does ensure CSR reimbursement payments and does enforce the individual mandate in 2018, there are literally dozens of other ways that Trump and HHS Secretary Tom Price could sabotage the 2018 Open Enrollment Period. Here's just a few, several of which they've already been caught doing:

Minimal or non-existent advertising/outreach/promotional efforts

Understaffing of call centers/support staff, leading to absurdly long hold times

Deliberately underthrottled server bandwidth, slowing HC.gov down or even taking it offline, especially during peak hours

"Accidentally" misentered enrollment instructions or policy specifications

Confusing or missing confirmation/status notification messages either on the site, via email or both

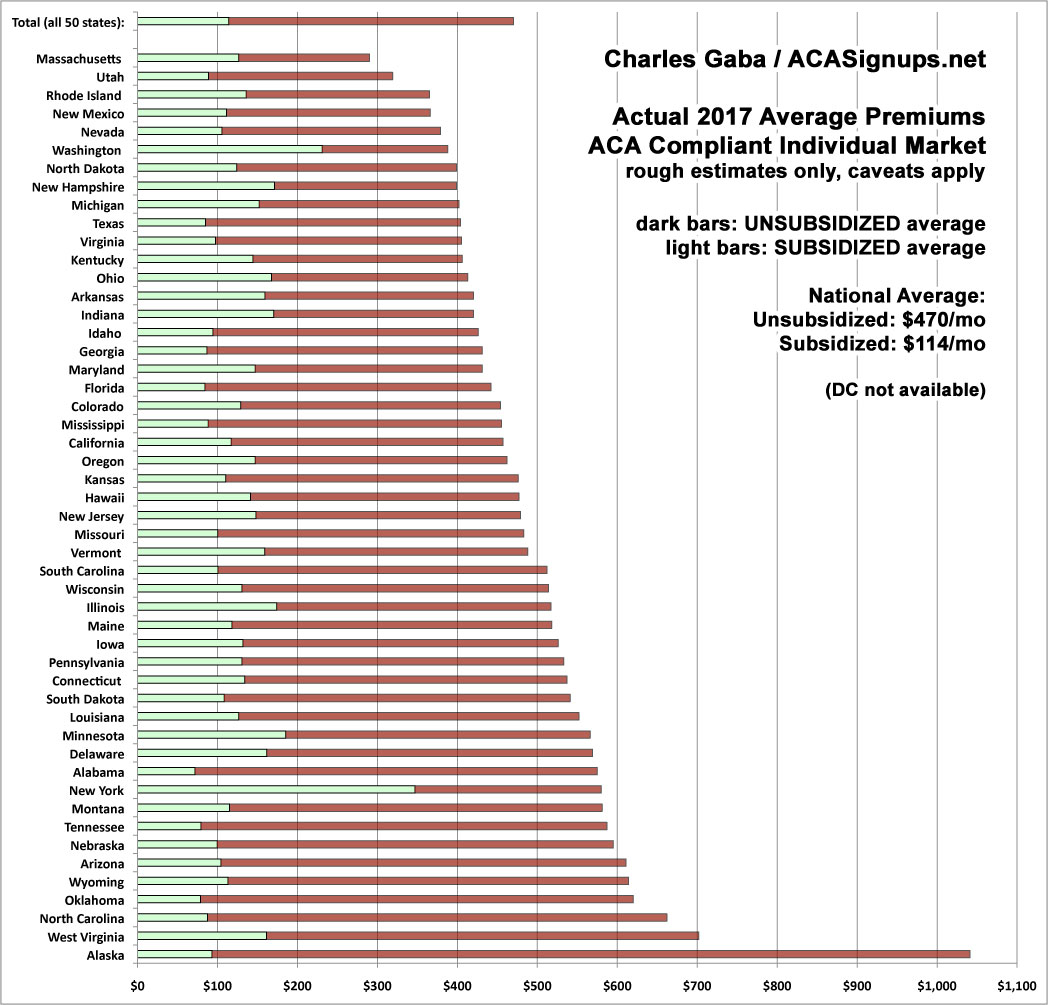

For all the fuss and bother about how much premiums are expected to go up on a percentage basis next year, using percentages can be misleading, since the lower the premium is to begin with, the more dramatic a percentage increase is going to seem relative to where it started.

With that in mind, I've decided to mush together two recent projects of mine: First, my debunking/correction of the May ASPE report which disingenuously claimed that individual market premiums had "increased by 105% since 2013 due to the ACA"; second, my 2018 Rate Hike Project.

As I noted when I debunked/corrected the ASPE report, not only did it turn out to be somewhat lower when all 50 states were included (84%, not 105%), but the ASPE report completely ignores both the financial assistance provided to roughly half the market and, just as importantly, blows off the apples to oranges mismatch between the numbers, because only a handful of states had guaranteed issue laws in 2013, and only one (NY) had a community rating law. Having said that, as long as you keep those caveats in mind, the (corrected) ASPE report does provide a good baseline for figuring out what the 2018 premiums are likely to be.

By merging the spreadsheets for these projects together, I've come up with a rough idea of what I expect to see in terms of unsubsidized, full-price premiums for individual ACA policies this November. I'm using a median instead of a weighted average this time around because I expect high variables in terms of the number of people who enroll in each state compared to 2017 (unfortunately, I still don't have 2018 data for several states, and I don't have the 2017 dollar average for DC to compare against).

I've ordered the states from lowest to highest based on the assumption that CSR reimbursements aren't made next year ("full sabotage effect"). The blue sections are my best estimates for each state assuming CSRs are paid; the yellow sections represent how much of the average premiums are due to "CSR padding" by the carriers.

Tuesday morning I left on a quickie family vacation to Mackinac Island; we got back into town last night, so I was gone for just 4 days. In that time, here's some of the bigger developments on the ACA/healthcare policy front:

The Congressional Budget Office issued their formal projection of the 10-year (9-year, really) impact of terminating CSR reimbursement payments permanently starting in January 2018. Their major takeaways are pretty much the same as what I and most other healthcare wonks have been projecting, with a few twists:

The fraction of people living in areas with no insurers offering nongroup plans would be greater during the next two years and about the same starting in 2020

Gross premiums for silver plans offered through the marketplaces would be 20 percent higher in 2018 and 25 percent higher by 2020—boosting the amount of premium tax credits according to the statutory formula

Most people would pay net premiums (after accounting for premium tax credits) for nongroup insurance throughout the next decade that were similar to or less than what they would pay otherwise—although the share of people facing slight increases would be higher during the next two years

Federal deficits would increase by $6 billion in 2018, $21 billion in 2020, and $26 billion in 2026

The number of people uninsured would be slightly higher in 2018 but slightly lower starting in 2020.

In general, their projections on the impact on premiums (unsubsidized and subsidized) is similar to what I, the Kaiser Family Foundation, Oliver Wyman and others have been saying all along: Around 20 percentage point increases across all Silver plans (which would be the equivalent of around 14-15% if spread out across all plans on & off the exchanges.

Hey Michigan Residents! Do you live in Michigan's 1st Congressional District? Are you sick of Jack Bergman (MI-01) refusing to even talk to you about their "replacement" healthcare bill, which would tear away healthcare coverage for millions of Americans and hurt the coverage of countless millions more?

If so, come on out to Traverse City TOMORROW, Sunday, August 20th, and join State Representatives Christine Greig (appearing in person) and myself (appearing via Skype) as we explain what the latest craziness is regarding the ACA, the GOP attempts to repeal and/or sabotage it and healthcare policy in general from 10:30am - 11:30am at the Workshop Brewery, 221 Garland St. in Traverse City:

{kind=link}