This means they added 1,613 more people in the past week, but the pool of current enrollees dropped by 1,675, which means that at least a small number have actively cancelled their policies altogether. Looked at another way, the number of new enrollees has increased by 3,211 (from 11,749 to 14,960), which means that, again, a couple thousand current enrollees who either actively (or were passively) auto-renewed have since gone back into the system and changed their mind and cancelled their 2018 plans. This is normal, especially for the states which "front-load" auto-renewals before the December deadline passes.

Last winter and spring, you may recall that I crunched a ton of data to come up with my best estimates about just how many people were projected to lose their healthcare coverage at the Congressional District level in the event various versions of Affordable Care Act repeal/replacement bills were to be signed into law (the AHCA, BCRAP, ORRA and so forth). After the first couple of attempts, the folks over at the Center for American Progress took over much of the heavy lifting on my part.

CAP started breaking the numbers out, leaving me to separate them out into easily-sharable state-level infographics (I also added partisan info for each member of Congress, since every Democrat has been steadfastly opposed to each one of these bills, while just about every Republican has supported most of them so far).

Eureka! I've finally acquired fairly up-to-date Open Enrollment data for the last blank state on my list: Vermont. The exchange representative kept it simple for me:

Vermont’s net plan selections as of December 2, 2017:

25,559 renewing individuals

1,335 new individuals (including those previously, but not currently, enrolled)

Enrollment in Qualified Health Plans and Essential Plan Reaches Nearly 900,000

December 15th is the Deadline to Enroll for January Coverage

New Yorkers Urged to Enroll Now

ALBANY, N.Y. (December 7, 2017) - NY State of Health, the state’s official health plan Marketplace, today announced enrollment in Qualified Health Plans (QHP) and the Essential Plan have reached nearly 900,000—continuing to outpace enrollment at the same point last year by 13 percent.

I've just been sent a link to the first official update on ACA exchange enrollment in DC. It includes a whole mess of demographic data (click below for full-size version), but the main takeaway is near the top: 18,740 QHP selections as of December 5th (compared against December 8th of last year). With auto-renewals included, this year's tally is about 2% shy vs. last year, but again, those extra 3 days make a bigger difference than you might think, especially as we approach the mid-December deadline.

It's important to remember that DC, along with California and New York, is sticking with the full 3-month Open Enrollment Period this year, so residents will still have another 6 weeks after 12/15 to sign up for coverage starting in either February or March.

Excellent news out of Massachusetts! I haven't posted any updates from the Bay State since 11/15, when they reported enrollments were up 40% year over year, but today they've given me very comprehensive and up-to-date numbers:

As of Dec. 6, we had a total of 259,815 plan selections and enrollments. This includes auto renewal of existing members. Of that, 26,074 are people who are new for 2018.

For comparison sake, for Dec. 6, 2016, we were at 244,845, and 25,746 for the new. These numbers also includes auto renewal, of course.

Obviously when you throw auto-renewals into the mix, the percentage increase drops substantially, but they're still up 6% over last year (nearly 15,000 people), and new enrolles are up about 1%.

OK, today saw two major 2018 Open Enrollment Period data updates out of HealthCare.Gov and Covered California, plus a minor one out of Maryland.

As I reported this morning, the HC.gov Week 5 Snapshot report came in much lower than I expected this week, at just 823K vs. the 1.2 million I was anticipating; as a result, the HC.gov section of The Graph (in green below) has finally reverted back to my original projection line with a total of 3.6 million as of December 2nd. If it follows my trendline this week, HC.gov should tack on another 1.2 million for a total of 4.8 million by Saturday night, December 9th, ahead of what should be the Big Final Week Surge.

Covered California’s Open Enrollment Continues at a Brisk Pace with New Data Showing Most Consumers Who Renewed and Enrolled in November will Pay Less in 2018

More than 102,000 new consumers selected a plan during the first month of open enrollment, a 28 percent increase over the same time period last year.

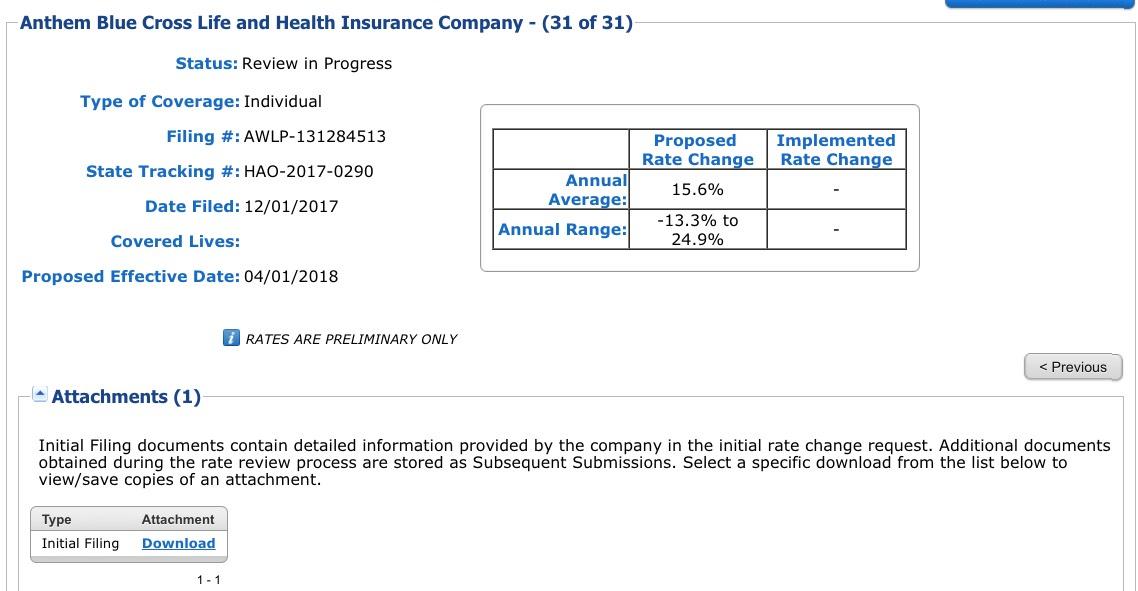

This just in from the California Insurance Dept...

Thank you for signing up to receive email alerts when new health insurance rate filings are submitted to the California Department of Insurance.

This message is to inform you that we have posted new rate filing submissions to our health rate filing website. Please select the link below to review and/or comment on newly added rate filing submissions. The Department of Insurance does not respond to questions about rate review filings submitted through the rate website, but we do consider comments during our review process.

After being way off in my initial HC.gov projections the first and second weeks of the 2018 Open Enrollment Period, I recalibrated and was dead on target for Weeks 3and 4: As of November 25th, just shy of 2.8 million people had selected Qualified Health Plans (QHPs) through the federal exchange.

As I had predicted, there were a bunch of eye-roll-inducing headlines about how enrollments had dropped off a cliff, etc etc, which completely ignored the fact that it was Thanksgiving week, and that a 35%+ drop-off is typical for the holiday weekend. Whatever.