Oklahoma has around ~293,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

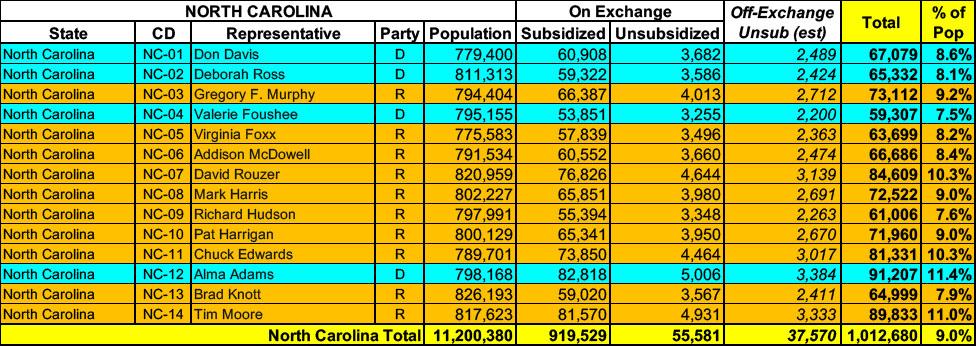

North Carolina has around ~975,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~37,000 unsubsidized off-exchange enrollees.

Montana has around ~77,000 residents enrolled in ACA exchange plans, 89% of whom are currently subsidized. I estimate they also have another ~8,400 unsubsidized off-exchange enrollees.

Louisiana has around ~293,000 residents enrolled in ACA exchange plans, 96% of whom are currently subsidized. I estimate they also have another ~13,000 unsubsidized off-exchange enrollees.

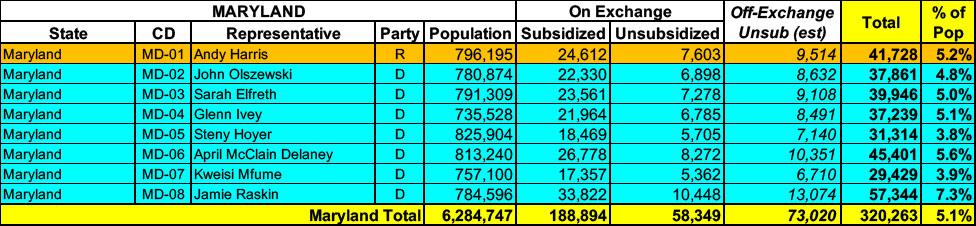

Maryland has around 247,000 residents enrolled in ACA exchange plans, 76% of whom are currently subsidized. I estimate they also have another ~73,000 unsubsidized off-exchange enrollees.

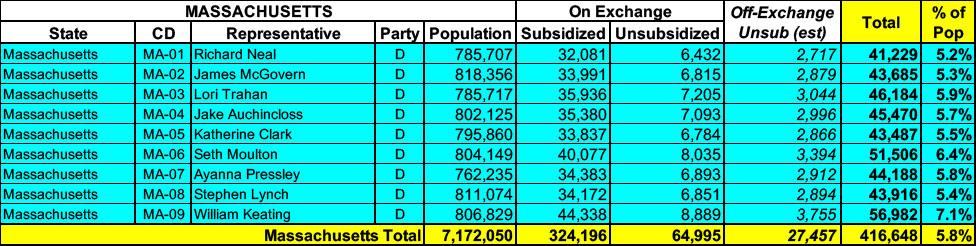

Massachusetts has around 390,000 residents enrolled in ACA exchange plans, 83% of whom are currently subsidized. I estimate they also have another ~27,000 unsubsidized off-exchange enrollees.

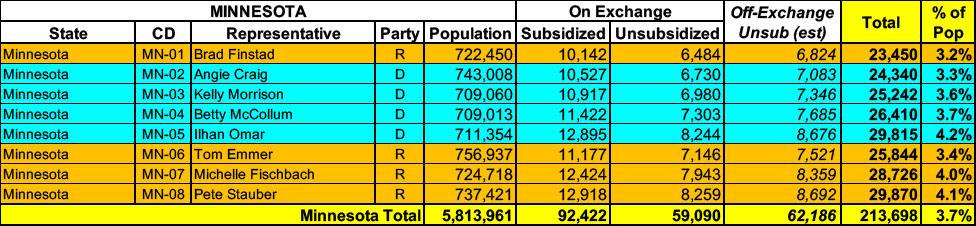

Minnesota has around 151,000 residents enrolled in ACA exchange plans, 61% of whom are currently subsidized. I estimate they also have another ~62,000 unsubsidized off-exchange enrollees.

Kentucky has around 97,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. I estimate they also have another ~6,800 unsubsidized off-exchange enrollees.

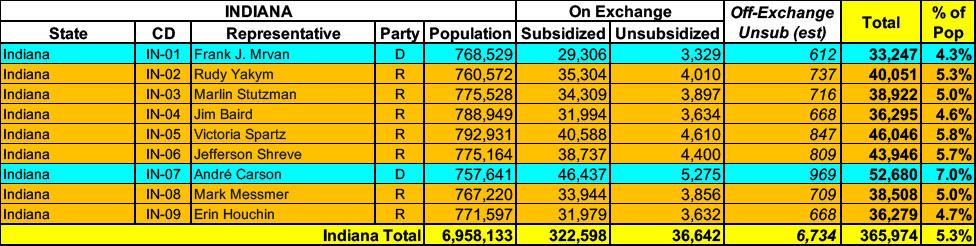

Indiana has around 359,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~6,700 unsubsidized off-exchange enrollees

According to the new report, total enrollment from September through December actually increased by just a hair (5,377) and still remained at over 20.7 million nationally, so it doesn't look like the Trump Admin has started cooking these particular books, at least not yet.

I've been able to cobble together more recent ACA expansion enrollment for about half of the 40 states (+DC) which participate in the program: