JULY 31st, 2025 - Nevadans Get a Preview of 2026 Proposed Health Insurance Rate Changes for Upcoming Open Enrollment

[CARSON CITY, NV] - Starting August 1st, Nevada consumers who shop for their health insurance on the individual health insurance market can view and provide comments on proposed rate changes for Plan Year 2026.

The Nevada Division of Insurance (Division) has received and made public on its website the 2026 proposed rate changes from health insurers intending to sell plans on and off the Silver State Health Insurance Exchange (the "Exchange"). The Exchange is the state agency that assists eligible Nevada residents to purchase affordable health and dental plans.

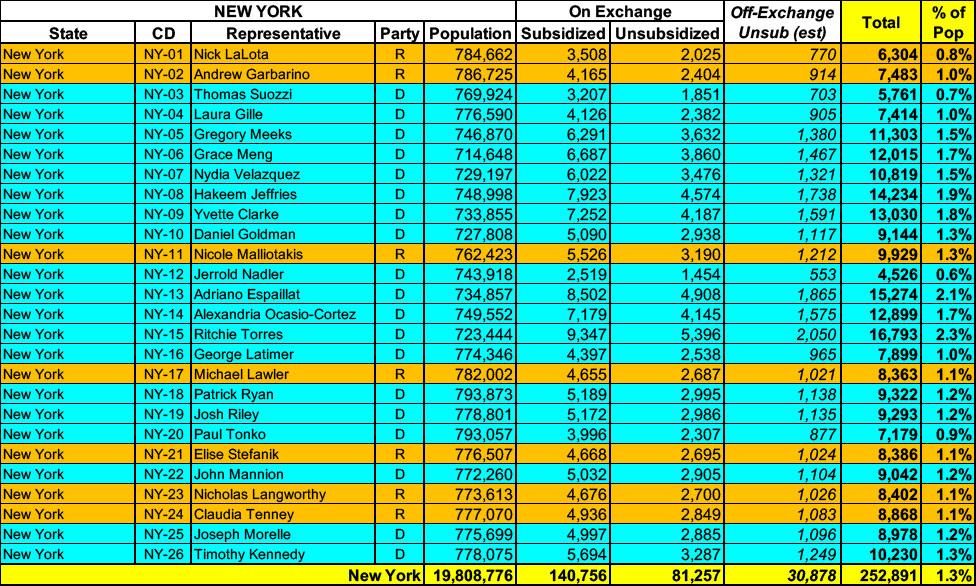

New York has around ~222,000 residents enrolled in ACA exchange plans, 63% of whom are currently subsidized. I estimate they also have another ~31,000 unsubsidized off-exchange enrollees.

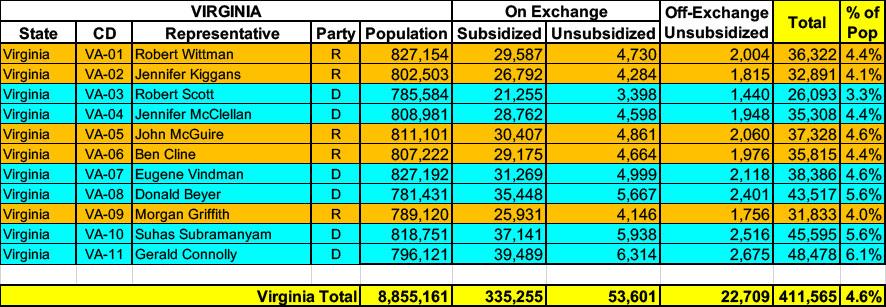

Virginia has ~388,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. They also have over 22,000 off-exchange enrollees. Combined, that's 411,000 people with ACA market coverage, or 4.6% of the total population.

South Dakota has around ~54,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~3,000 unsubsidized off-exchange enrollees.

Green Mountain Care Board Receives 2026 QHP Rate Requests Amid Rising Health Care Costs

Montpelier, VT – On May 12, 2025, the Green Mountain Care Board (GMCB) received the 2026 individual and small group health insurance premium rate filings from BlueCross and BlueShield of Vermont and MVP Health Plan. The filings will be posted on GMCB’s rate review website. The average rate increases being requested are shown below:

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

However, there's an important caveat:

While it appears that Congress will allow enhanced federal Premium Tax Credits to expire, New Mexico’s Health Care Affordability Fund (HCAF) will cover the loss of the enhanced premium tax credits for households with income under 400% of the Federal Poverty Level (or $128,600 for a family of four), providing up to $68 million in premium relief for working families who enroll in coverage through BeWell in 2026. Federal and state premium assistance will continue to reduce the impact of the rate increases.

(Unfortunately, Avera hasn't provided a justification summary and has almost completely redacted their actuarial memo, making it impossible for me to know what their current enrollment is; see below)

Blue Cross and Blue Shield of Montana (BCBSMT) filed rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate changes for these plans is an increase of 0.9% to an increase of 42.5%.

Product Blue Preferred Blue Focus Changes in allowable rating factors, such as age, geographical area, or tobacco use, may also impact the premium amount for the coverage.

There are currently 44,116 members on Individual Affordable Care Act (ACA) plans that may be affected by these proposed rates.

Consistent with the filed URRT, earned premiums for Individual plans during calendar year 2024 were $252,957,302 and total claims incurred were $235,192,937. The proposed rates effective January 1, 2026, are expected to achieve the loss ratio assumed in the rate development.

Blue Cross and Blue Shield of New Mexico (BCBSNM) is filing new rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate changes for these plans is an increase of 18.4% to an increase of 49.6%.

The cost relativities among plans are different from the experience period to the prospective rating period due to anticipated non-uniform changes in network reimbursement levels. Additionally, the rates vary by plan due to the leveraging and utilization differences driven by variations in member cost sharing. Therefore, the proposed rates and rate changes may vary by plan.

Changes in allowable rating factors, such as age and geographical area, may also impact the premium amount for the coverage.

NJ Department of Banking and Insurance Releases Initial Health Insurance Rates for the Individual Market for Plan Year 2026

Federal Inaction on Enhanced Premium Tax Credits Among Issues Impacting Consumer Costs

TRENTON — The New Jersey Department of Banking and Insurance today announced that plan year 2026 health insurance initial rates have been submitted by insurance carriers operating in the individual market, which includes Get Covered New Jersey, the State’s Official Health Insurance Marketplace.