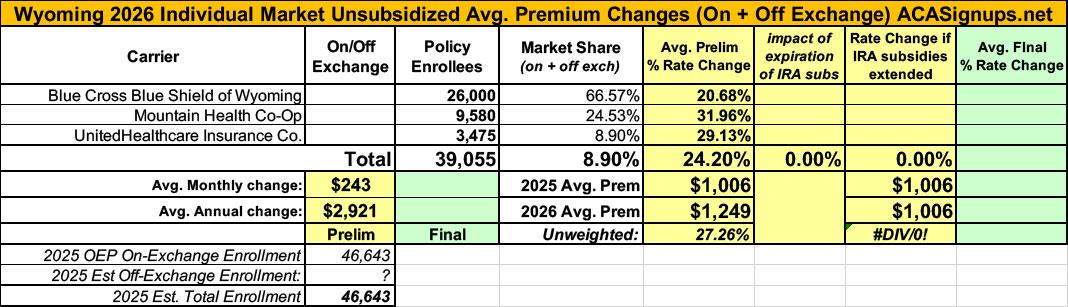

It was just a couple of weeks ago that the official (if preliminary) 2026 ACA individual market rate filings for Wyoming insurance carriers went live on the federal rate review website.

I published a writeup about these just 3 days ago; unlike some states, Wyoming was pretty easy to break out as they only have three carriers on the indy market, all of which also made their current enrollment data easy to find.

The landscape isn't pretty: BCBS is seeking average rate increases of 20.7%; UHC wants 29.1%, and Mountain Health Co-Op, which has around 9,600 enrollees, was asking for a whopping 32% average premium hike.

Keep in mind that Wyoming already has among the most expensive individual market policies in the country, with premiums averaging over $1,000/month.

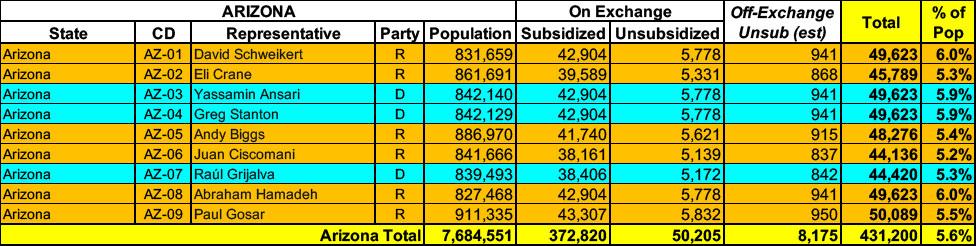

Arizona has around 423,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have perhaps another ~8,000 unsubsidized off-exchange enrollees.

Open Enrollment Period through Get Covered New Jersey Begins November 1, 2025

TRENTON — New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman today announced a total of $5 million in available grant funds for community organizations to apply to serve as state-certified Navigators for the Get Covered New Jersey Open Enrollment Period and throughout 2026. Navigators offer free, unbiased, community-based education and assistance to consumers seeking to enroll in health insurance through Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

Delaware has ~53,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. They also have an unknown number enrolled in off-exchange plans. Overall, with net attrition, I estimate current total enrollment is down a bit to perhaps 52,000 today.

Connecticut has around ~151,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of April 2025:

Public comment at Washington Health Benefit Exchange Board includes 10 testimonials, plus additional stories

OLYMPIA, Wash. – Washingtonians shared stories of how access to more affordable health insurance has affected lives and communities all across the state, with Washington Health Benefit Exchange (Exchange) Board last week. The testimonials were particularly impactful in light of a myriad of recent federal changes to state-based marketplaces such as the Exchange, and the impending potential expiration of enhanced premium tax credits (ePTC) before Congress.

SACRAMENTO, Calif. — Due to recent rule changes made by the federal government, Covered California enrollees who are part of the Deferred Action for Childhood Arrivals (DACA) program will have their Affordable Care Act health insurance terminated on Aug. 31, 2025. The federal rule will affect more than 2,300 DACA recipients in California.

More congressional Republicans are saying they could support a limited extension of enhanced Affordable Care Act subsidies — but only as part of a wider deal and with possible new limits to the assistance.

Why it matters: Democrats are pushing for a clean extension, but the more realistic path, if there's one at all, is a short-term extension that includes conservative health policies.

What they're saying: "How many clean extensions have you seen of late?" said Sen. Thom Tillis, who began pushing for a subsidy extension in the spring. He added that he didn't know what the contours of a deal could look like.

...Changes that could make an extension more palatable for Republicans include limiting the subsidies for higher-income enrollees or requiring that all enrollees pay at least some cost-sharing or premiums.

Now that I've finally completed overhauling & updating my House District Healthcare Enrollment Pie Chart project with the latest data, I wanted to address a rather frustrating elephant in the room.

For most of the healthcare programs involved, the enrollment data is now reasonably up to date: