A few days ago, the Centers for Medicare & Medicaid released three important new reports on the 2018 Open Enrollment Period and trends in the individual market. There's a lot of data to go over, so I'm breaking my analysis into several smaller posts for easier readability.

Next, let's take a look at the average unsubsidized monthly premiums and APTC subsidies in each year. I've already crunched all of these data before, but that was based on the QHP selctions from the 2017 and 2018 Open Enrollment Periods. The table below is more accurate since it reflects the actual average premiums and subsidy amounts for all of 2017 and for 2018 after subtracting out nearly all of those who never actually paid for their first month of coverage. The numbers for each state and nationally should be close but slightly different:

A few days ago, the Centers for Medicare & Medicaid released three important new reports on the 2018 Open Enrollment Period and trends in the individual market. There's a lot of data to go over, so I'm breaking my analysis into several smaller posts for easier readability.

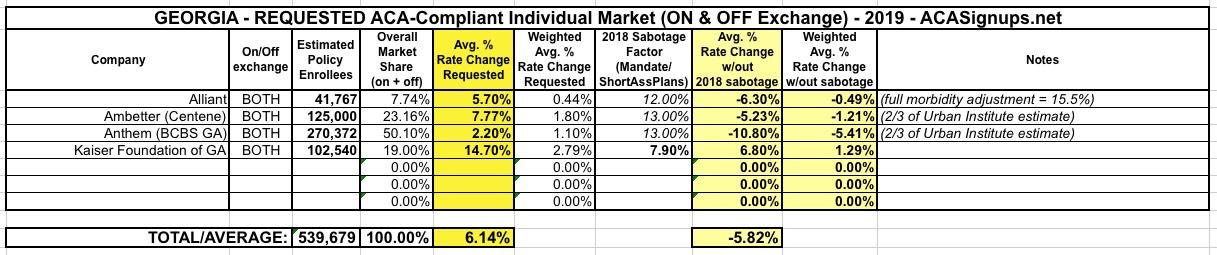

Whew! Georgia only has 4 carriers participating in the individual market, but tracking down some of the data was a royal pain in the butt, especially Ambetter/Centene, which not only buried the numbers I needed inside a whopping 1,900-page PDF file, but the actual average requested rate increase wasn't even included; for that I had to check a different file. Yeesh.

The good news is that carriers in Georgia are only requesting around a 6.1% average rate increase for ACA-compliant individual market policies next year.

The bad news is that if it weren't for the ACA's individual mandate being repealed and the Trump Administration's expansion of #ShortAssPlans, 2019 premiums would likely be dropping by around 5.8% instead.

NOTE: My broadband connection has been experiencing a lot of problems lately; I have a service guy on his way out today for the fourth time in the past two weeks, but this means I'll likely be offline for a few hours, so this post will be incomplete for awhile.

Centers for Medicare and Medicaid Services Releases Reports on the Performance of the Exchanges and Individual Health Insurance Market

Reports show individual market erosion and increasing taxpayer liability

Um...yeah, deliberately sabotaging the ACA a dozen different ways and cutting off CSR reimbursement payments, thus forcing the carriers to load CSR costs directly onto premiums, which in turn jacks up APTC subsidies accordingly, will have the effect of "increasing taxpayer liability"). Go on...

On November 8, 2010--right after the "Red Wave" midterm election in which Republicans picked up a jaw-dropping 63 seats in the U.S. House of Representatives, 6 Senate seats and 680 state legislative seats--Paul Waldman wrote, in The American Prospect:

In charting the last two years, from the euphoria of election night 2008 to the despair of election night 2010, I keep returning to Mario Cuomo's famous dictum that you campaign in poetry but govern in prose. The poetry of campaigning is lofty, gauzy, full of possibility, a world where problems are solved just because we want them to be and opposition melts away before us. The prose of governing is messy and maddening, full of compromises and half-victories that leave a sour taste in one's mouth.

...All else being equal, this means Republicans have an easier time getting elected and a harder time legislating the things they really want to do (other than tax cuts, which are never a hard sell), while Democrats have a harder time getting elected but ought to have an easier time legislating.

For nearly a year, healthcare wonks like myself, David Anderson, Andrew Sprung and Louise Norris have been heavily getting the word out to promote not just the "Silver Loading" CSR-load workaround, but an even more clever variant which I've coined "the Silver Switcharoo" which takes the concept of Silver Loading and goes one step further.

*(OK, these are technically only "semi-approved" rates...there could still be some additional tweaks later on after public comment, etc.)

Oregon was the fourth state which I ran a preliminary 2019 rate increase analysis on back in May. At the time, I concluded that insurance carriers were requesting a weighted average increase of 10.5% for ACA-compliant individual market policies next year. I knew that Oregon's state-based Reinsurance program was helping keep that average down to some degree, but I didn't know exactly how much of a factor it was.

I also knew that efforts to sabotage the ACA by Donald Trump and Congressional Republicans would play a major role in increasing 2019 rates: Repeal of the individual mandate is a big factor, along with the unnecessary 1-point increase in the state exchange fee being imposed on Oregon and the other four states which run their own exchange but "piggyback" on HealthCare.Gov's technology platform.