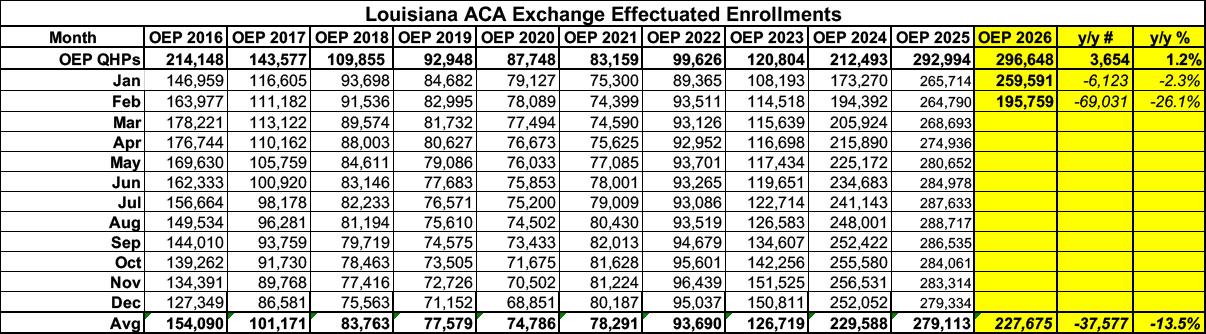

Before I begin, it's important to note that ACA exchange enrollment has plummeted in Louisiana since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year.

Initial signups during the 2026 Open Enrollment Period were actually up slightly vs. OEP 2025...but actual effectuated enrollment was 2.3% lower as of January...and then fell off a cliff in February, with enrollment dropping a stunning 26% vs. a year earlier. That's over 69,000 Louisianans who were priced out of coverage in just the first two months of the year:

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

Initial signups during Open Enrollment were only down about 2% vs. 2025..but effectuated enrollment began to drop immediately and has continued to drop every month since then.

As of June 2026, effectuated enrollment is down 8.4% vs. a year earlier, and is down 7.7% on average for the year so far. That's around 22,000 fewer Coloradans with ACA exchange coverage so far this year:

Before I begin, it's important to note that ACA exchange enrollment has dropped in Pennsylvania since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year...although thanks to the state implementing fairly robust Premium Alignment pricing, it's not nearly as dramatic a drop-off as in most other states.

Initial signups during Open Enrollment were actually slightly higher than last year...but effectuated enrollment began to drop starting in February and has continued to drop at an increasing rate every month since then. As of July 2026, effectuated enrollment is down more than 10% vs. a year earlier, and it's down nearly 4% on average for the year so far. That's 48,000 fewer Pennsylvanians with ACA exchange coverage as of July:

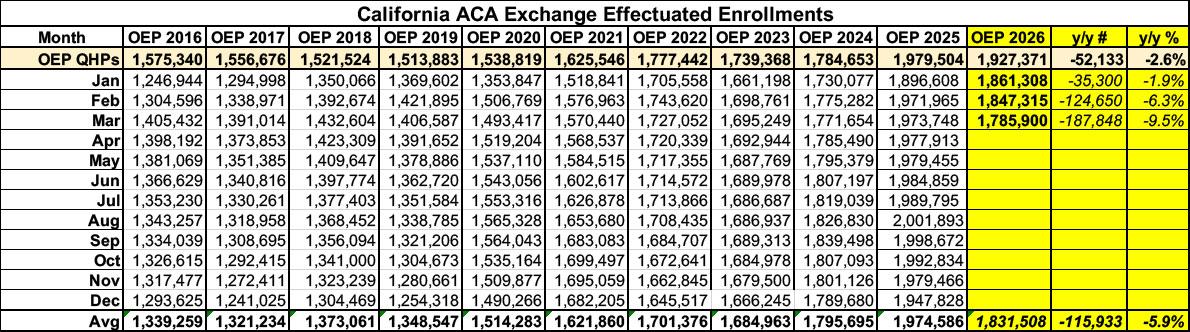

Before I begin, it's important to note that ACA exchange enrollment has dropped in California since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year...although thanks to the state providing its own supplemental financial subsidies to partially cancel out the lost federal subsidies, it's not nearly as dramatic a drop-off as in most other states.

Effectuated enrollment was down 9.5% year over year as of March, and has almost certainly continued to drop further since then based on the trend line (see below). That's at least 187,000 fewer Californians enrolled in ACA healthcare coverage this year.

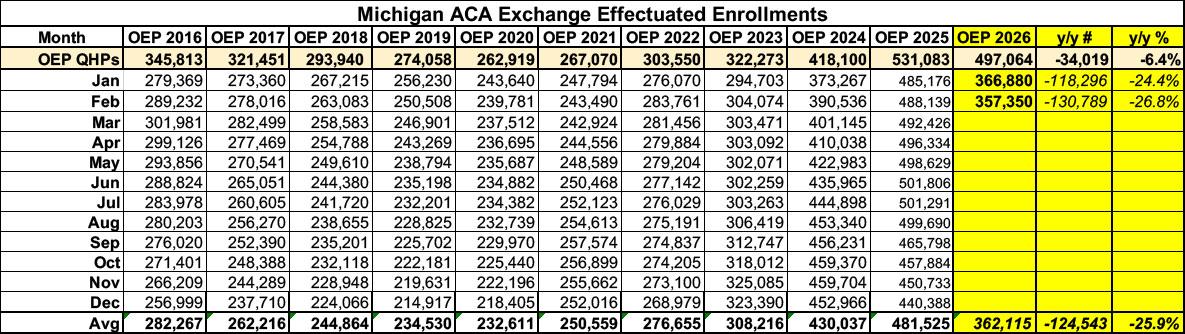

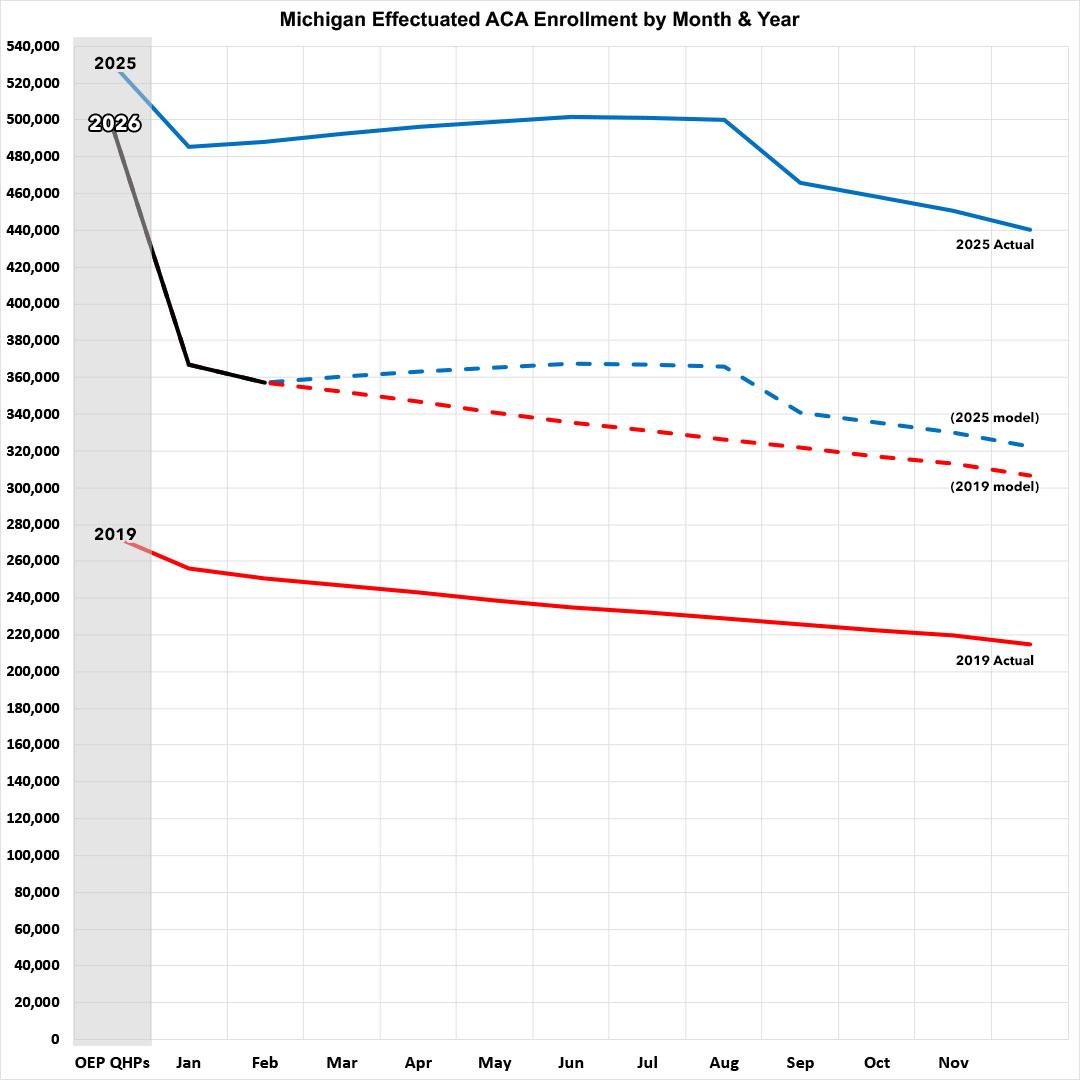

Before I begin, it's important to note that as in most states, ACA exchange enrollment has plummeted in Michigan since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year: Effectuated enrollment was down 27% year over year as of February, and has almost certainly continued to drop further since then. That's at least 131,000 fewer Michiganders enrolled in ACA healthcare coverage this year.

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

Health Carriers Propose Affordable Care Act Premium Rates for 2027

Proactive policies of the Moore Administration and General Assembly ensure that Maryland's individual premium rates remain among the lowest in the nation, in spite of federal pressures due to changing Exchange rules and continued lack of expansion of enhanced tax credits

BALTIMORE – The Maryland Insurance Administration has received the 2027 proposed premium rates for Affordable Care Act products offered by health and dental carriers in the individual, non-Medigap and small group markets, which impact approximately 482,000 Marylanders and represents 19% of the commercial health insurance market.

In the individual, non-Medigap market, carriers are requesting an overall average rate change of 13.7%, with the average request by carrier ranging from 12% to 14.6%.

2027 Requested Commercial Health Insurance Rates Have Been Submitted to OHIC for Review

The Office of Health Insurance Commissioner (OHIC) today released the individual, small group, and large group market premium rates requested by Rhode Island’s insurers. The requests were filed as part of OHIC’s rate review process (for coverage effective on or after January 1, 2027).

“Health insurers are once again seeking rate increases to cover the rising cost of health care and other expenses,” said Health Insurance Commissioner Cory King. He continued: “OHIC will thoroughly review these requests to determine whether they are justified.”

Two insurers, Blue Cross Blue Shield of Rhode Island (BCBSRI) and Neighborhood Health Plan of Rhode Island (NHPRI), filed rates for plans to be sold on the individual market to people and families who do not receive insurance through their employer.

The first thing that's important to understand about the Indiana insurance market is that there are two carriers leaving the individual (ACA) market, and one possibly (?) leaving the small group market next year.