Key Insurers Expect To Lose Nearly 3M Combined ACA Enrollee By End Of 2026

Key publicly traded insurers reported in recent earnings calls that they expect to lose nearly 3 million enrollees combined by the end of 2026, buoying stakeholders’ fear that the loss of the enhanced tax credits will drive more people from the marketplace than the 1 million fewer signups reported by CMS

While CMS’ mid-January snapshot showed that about 1 million fewer people enrolled in an Affordable Care Act plan during open enrollment compared to last year, insurers in recent earnings calls are echoing state exchange officials’ belief that true results will take time, and four large companies reveal they expect at least 2.8 million fewer ACA exchange consumers.

Also, in line with comments from state exchange officials, carriers are seeing more consumers enrolled in less-expensive bronze plans, which have higher co-pays and deductibles.

Molina exchange business grew by 302,000 consumers to reach a total 620,000 enrollees in the first quarter, outpacing the company’s earlier 500,000 estimate, growth that CEO Joseph Zubretsky says was driven by strong product design and pricing, higher effectuation rates, lower attrition and the special open enrollment period.

Molina’s marketplace business had a Medical Loss Ratio of 77.3%, which was due to the higher-than-expected direct COVID-related costs as cases surged in many areas.

There's a lot packed into that first paragraph.

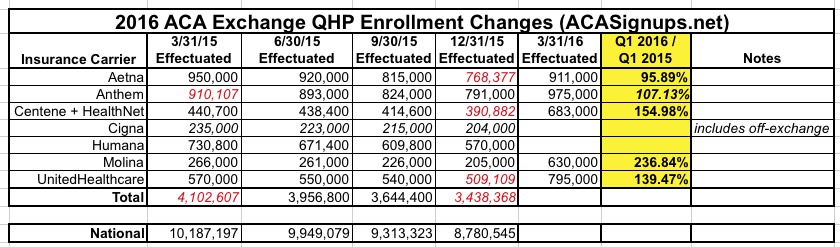

First, their ACA enrollment (which presumably includes off-exchange) for Q1 was 24% higher than expected, which is quite an eye-opener.

For the past two weeks, along with other noteworthy Open Enrollment data numbers, I've been scratching my head over what the deal is in Mississippi:

Once again, Maine remains the worst-performer year over year, mostly due to their expansion of Medicaid. Idaho isn't listed because they're a state-based exchange and haven't reported any data yet. Mississippi, on the other hand, continues to be the top out-performer vs. last year, which is interesting because there doesn't seem to be any particular reason for it.

Unlike some states, Mississippi hasn't implemented any additional subsidies, a mandate penalty or a reinsurance program of any sort. They haven't had any new carriers join the ACA market, nor have any of them left. I don't think either of the carriers on the exchange have significantly expanded their territory or changed their offerings that much either...in fact, average premiums are essentially flat year over year.

In other words, by all rights, Mississippi should be performing almost exactly as they did last year...but enrollments are up 15.5% to date. Huh.

*(Disclaimer: No, that's not a direct quote from Dr. Molina, but it's a pretty damned spot-on paraphrase).

A couple of weeks ago I noted that a buttload of heavy players in the healthcare field sent a joint letter to Trump, Tom Price and everyone else under the sun making it pretty clear how vital resolving the CSR issue is, and what the consequences would be if Congress and Trump don't make good on them.

Today, Molina Healthcare, which has around 1 million ACA exchange enrollees at the moment (roughly 9% of all effectuated enrollees) lowered the boom even harder (via Bob Herman of Axios):

Molina will exit exchanges if ACA payments aren't made

Politically, the big unknown is whether or not Paul Ryan and Mitch McConnell will get away with trying to pin the blame for this on the Democrats/the law itself. That's why they've been pushing the "Obamacare is already in a death spiral!" claim hard for the past few weeks, even though it quite simply isn't.

...So, if this does end up in a worst-case scenario, Trump's "stop enforcing the mandate altogether!" order here could end up causing that death spiral even if the GOP doesn't technically end up repealing anything legislatively. The carriers would start announcing that they're bailing next year as soon as this spring (remember, the first paperwork for 2018 exchange participation has to be filed in April or May), and McConnell/Ryan would simply say, "See?? We told you it was collapsing all by itself! We didn't touch nuthin'!!"

Thanks to Adam Cancryn for calling my attention to Molina's quarterly earnings report, which has this rather eye-opening section:

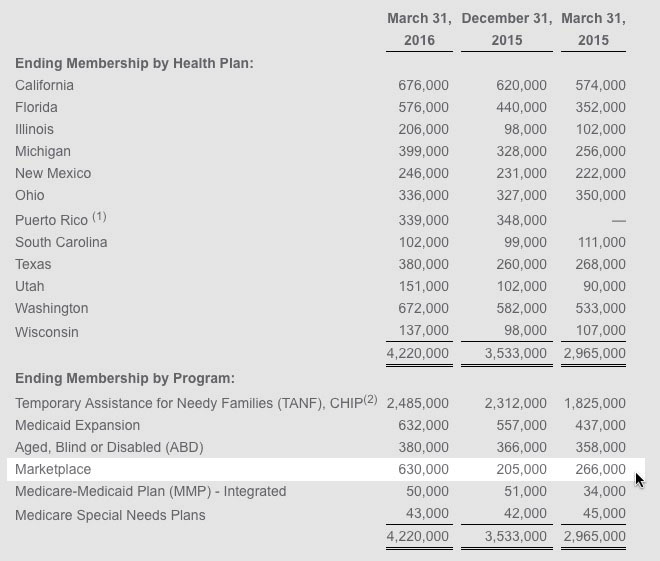

I've used Molina's Q1 2016 report, along with the Q4 2015 reports of Cigna and Humana, to further fill in the "Major Insurer" table I've been working on all this week; here's what it looks like now:

U.S. health insurers Aetna Inc and Anthem Inc on Friday sought to reassure investors that their Obamacare businesses had not worsened after UnitedHealth Group Inc warned of mounting losses in that sector.

Aetna and Anthem said their individual insurance businesses, which include the plans created by President Barack Obama's national healthcare reform law, had performed in line with projections through October. Both backed their earnings forecasts for 2015.