ALBANY, N.Y. (December 3, 2019) – NY State of Health, the state’s official health plan Marketplace, today announced its continued partnership with NYS Department of Agriculture and Markets in an effort to educate shoppers at farmers markets throughout New York State about low-cost, high-quality health coverage during the Open Enrollment Period.

Consumers must enroll by December 15, 2019 for coverage beginning January 1, 2020. Certified Enrollment Assistors will be available leading up to the December 15 deadline at select markets to answer any questions about enrolling in a health plan through the Marketplace and to set up enrollment appointments. In addition, NY State of Health educational materials will be available at select farmers’ markets across the state. This is the fourth year of the NY State of Health-NYS Department of Agriculture and Markets partnership.

Increased Visits to Food Pantries During Holiday Season Provide Opportunity to Reach Uninsured New Yorkers

ALBANY, N.Y. (November 25, 2019) – NY State of Health, the state's official health plan Marketplace, today announced its partnership with food pantries for the third holiday season to educate consumers about enrolling in high quality, affordable health insurance. Food pantries across New York will have certified enrollment assistors on-site throughout November and December to answer questions about health coverage options and how to enroll in a health plan. This year, the Marketplace is also offering eligible New Yorkers the option to receive information on the Supplemental Nutrition Assistance Program (SNAP) during the enrollment process.

Press Release: NY State of Health Announces Annual Renewal Begins Saturday

500,000 New York State Households Expected to Renew Their Health Plan for the 2020 Plan Year

Consumers Must Enroll or Renew by December 15 for Coverage Effective January 1

ALBANY, N.Y. (November 14, 2019) - NY State of Health, the state’s official health plan Marketplace, today announced that beginning November 16, the Marketplace will be open for individuals looking to renew or change their health plan for 2020. Open Enrollment for new customers seeking to enroll in a Qualified Health Plan began November 1 and runs through January 31, 2020. New Yorkers must enroll by December 15 for coverage beginning January 1, 2020.

Press Release: Governor Cuomo Announces the Start of NY State Of Health's 2020 Open Enrollment Period

New York's Uninsured Rate Continues to Decline, Among Lowest in the Nation

More than 4.8 Million New Yorkers Have Enrolled Through NY State of Health

Governor Andrew M. Cuomo today announced that on November 1, NY State of Health - New York State's Health Plan Marketplace and a national leader in enrolling people into quality, affordable health coverage - will begin its seventh annual open enrollment period for New Yorkers who want quality, low-cost health insurance coverage in 2020.

I'm not sure how this slipped by me, but in addition to Covered California already having launched their 2020 Open Enrollment Period yesterday, five other state-based ACA exchanges are already partly open as well. That is, you can shop around, compare prices on next year's health insurance policies and check and see what sort of financial assistance you may be eligible for:

I'm not sure when the other 7 state-based exchanges will launch their 2020 window shopping tools, nor do I know when HealthCare.Gov's window shopping will be open for the other 38 states, although I believe they usually do so about a week ahead of the official November 1st Open Enrollment Period launch date.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

DFS ANNOUNCES 2020 PREMIUM RATES: LOWERS OVERALL REQUESTED RATES FOR INDIVIDUALS AND SMALL BUSINESSES TO PROTECT CONSUMERS AND FUEL A COMPETITIVE HEALTH INSURANCE MARKETPLACE

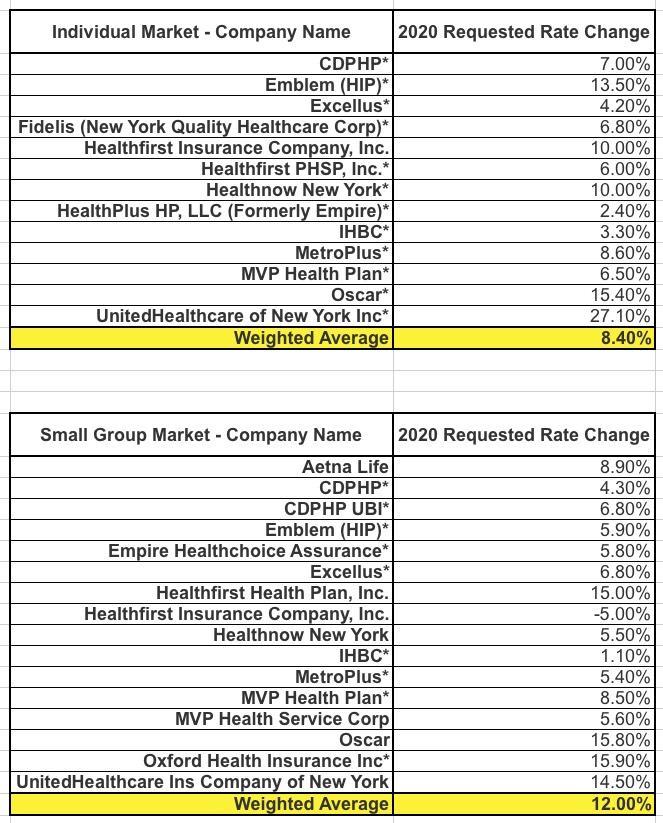

Back on May 31st, I reported that New York's Dept. of Financial Services had released the preliminary, requested premium rate hikes for the 2020 ACA individual and small group markets. At the time, the weighted average increase requested state-wide was around 8.4% (although I got 8.3% when I plugged the hard enrollment numbers into a spreadsheet).

For the small grouip market, NY DFS reported an average requested increase of 12.0%, although again, I only got 11.3% when I plugged in the numbers.

Yesterday, however, NY DFS became the third state (after Oregon and Virginia) to publicly release their approved 2020 premium changes...and like OR & VA, they've shaved a few points off the average rates:

DFS ANNOUNCES 2020 PREMIUM RATES: LOWERS OVERALL REQUESTED RATES FOR INDIVIDUALS AND SMALL BUSINESSES TO PROTECT CONSUMERS AND FUEL A COMPETITIVE HEALTH INSURANCE MARKETPLACE

2020 INDIVIDUAL AND SMALL GROUP REQUESTED RATE ACTIONS

5/31/2019 - Health insurers in New York have submitted their requested rates for 2020, as set forth in the charts below. These are the rates proposed by health insurers, and have not been approved by DFS.

* Indicates the Company offers products on the NY State of Health Marketplace.

The NY DFS website also includes handy links to the actual enrollment numbers for every carrier on both the Individual and Small Group market, allowing me to break out the numbers further:

NY State of Health Releases 2019 Open Enrollment Report

Essential Plan and Qualified Health Plan Enrollment Reach Record Levels

ALBANY, N.Y. (May 9, 2019)—NY State of Health, the state’s official health plan Marketplace, today released detailed demographic data on the more than 4.7 million New Yorkers enrolled in comprehensive health coverage through the close of the sixth open enrollment period on January 31, 2019. Marketplace enrollment is now at its highest point ever, and Essential Plan and Qualified Health Plan enrollment reached record levels of more than 1 million people.

“It’s evident in the numbers released today that there is high demand for quality, affordable health coverage,” said NY State of Health Executive Director, Donna Frescatore. “The 2019 record enrollment levels are proof that New York’s Marketplace remains strong.”

NY State of Health 2019 Open Enrollment Report Highlights