Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

BREAKING -- Poverty rights group files suit in federal court against work requirements MI has enacted for those on expanded Medicaid program Healthy Michigan.

A lawsuit has been filed challenging Michigan's new Medicaid work requirements that take effect Jan. 1. Plaintiffs are 4 people enrolled in the Medicaid expansion program known as Healthy Michigan #MiLeg

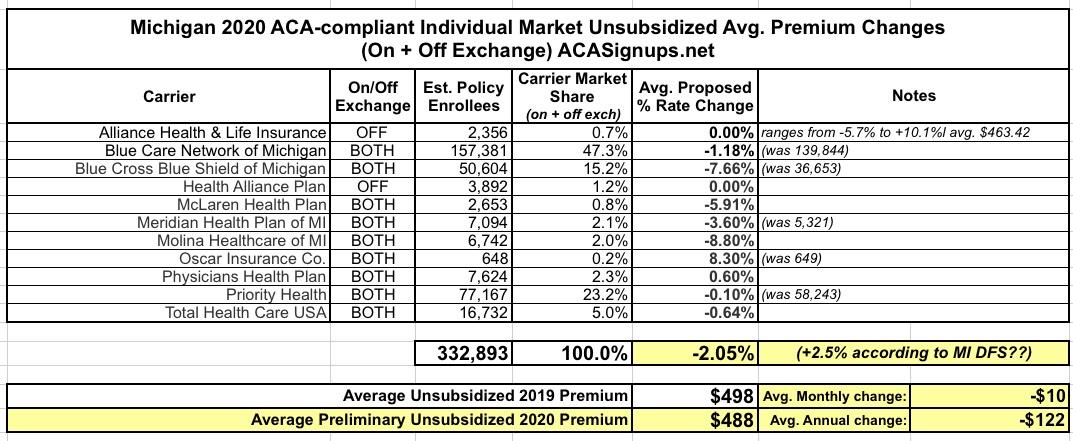

At the time, I concluded that the weighted average change marketwide was a 2.1% reduction in premiums compared to 2019, for around 333,000 Michiganders on the Indy market. This would mean roughly a $10 average premium reduction per unsubsidized enrollee per month, or $122 per year:

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Back in June, I noted that the Michigan legislature was trying to slap a band-aid on the terrible GOP-passed & signed Medicaid work requirement bill (aka "God's Safety Net" bill) which passed about a year ago.

As you may recall, the original bill added fairly draconian work requirements to Michigan's implementation of the ACA's Medicaid expansion program, known here as "Healthy Michigan". Around 670,000 Michiganders are covered by the program (the number fluctuates between around 650K - 700K from week to week) today.

At the time, several reports had come out putting the number of people likely to lose healthcare coverage under the new requirements (which go into effect on January 1st, 2020) as high as 183,000 statewide, or as much as 28% of the total covered population...thousands of whom would lose coverage even if they do comply with the rules but aren't able to comply with the reporting requirements.

A few weeks ago, I posted a lengthy, in-the-weeds explainer about how the ACA's Medical Loss Ratio (MLR) provision works. The short version is that ever since the ACA went into effect in 2011 (3 years before newly-sold policies had to be ACA compliant), to help reduce price gouging, insurance carriers have been required to spend a minimum of 80% of their premium revenue (85% for the large group market) on actual medical claims.

Put another way, their gross margins are limited to no more than 20% (or 15% in the large group market). Remember, that's their gross margin, not net; all operational expenses must come out of that 20% (15%). The idea is that they should be spending as much of your premium dollars as possible on actual healthcare, as opposed to junkets to Tahiti or marble staircases in the corporate offices, etc. Anything over that 20% (15%) gross margin has to be rebated to the policyholder.

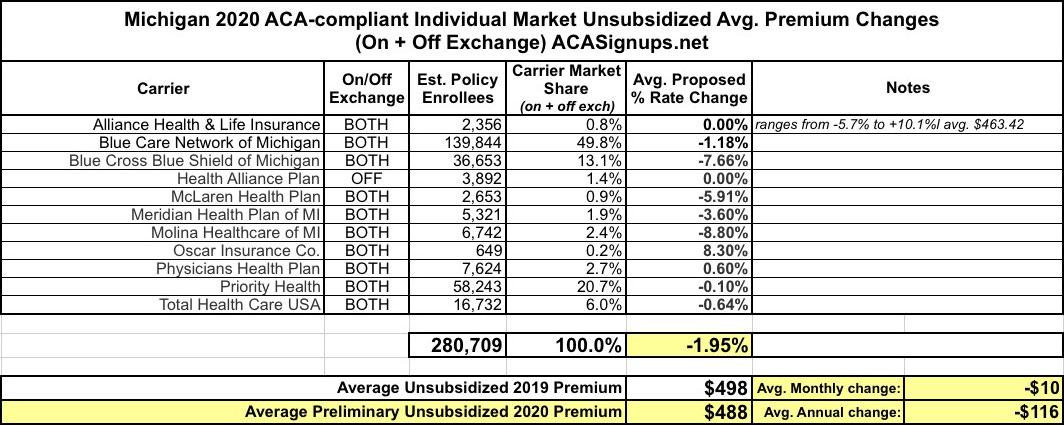

At the time, I concluded that the weighted average change marketwide was a 1.95% reduction in premiums compared to 2019, for around 281,000 Michiganders on the Indy market. This would mean roughly a $10 average premium reduction per unsubsidized enrollee per month, or $116 per year:

Several studies, including this one from just the other day, have driven home this point clearly: Adding work requirements to Medicaid expansion enrollees serves no useful purpose other than to kick tens of thousands of people off of their healthcare coverage (which, of course, is the whole point from the POV of those who add the requirements).

As for the one positive-sounding goal (increasing employment) which supporters always use to try and justify them, that's a complete joke:

The first major study on the nation’s first Medicaid work requirements finds that people fell off of the Medicaid rolls but didn’t seem to find more work.