Beneficiaries with Healthy Michigan Plan Coverage: 588,641

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of March 16, 2015

*Updated every Monday at 3 p.m.

So, for a year and a half now, I've been plugging raw data into spreadsheets and meticulously tallying the health insurance comings & goings of pretty much every person outside of Medicare, traditional Medicaid, ESI and the Indian Health Service.

I've learned more about the different types of health insurance polices than I ever wanted to. Small group. Large group. Off-exchange. "Grandfathered" plans. "Transitional" plans. The Child Health Plus (CHP) program in New York (not to be confused with the Children's Health Insurance Program (CHIP). The Basic Health Plan in Minnesota (MinnesotaCare). HMOs. PPOs. EMOs. "Sub26ers". Different Metal Levels.

Pharmspective is a company that specializes in healthcare industry data visualization/management apps. Most recently, they've announced a new app called "ACO Tracker" which basically does just that: Unscrambles information about Accountable Care Organizations, which are a Big Deal® these days.

Full disclosure: While they're not paying me to promote this particular app for them, they did pay me to help out with some data issues last fall, so take that for what you will (as an aside, in the process of helping them answer some questions which aren't directly related to this site last year, I also stumbled upon some info which is directly related, so that worked out nicely).

Anyway, I don't know much about ACOs myself, but as a data nerd it seems like a pretty cool app for those interested in this area, so what the heck: Check it out.

Wyoming Gov. Matt Mead (R) is no fan of the Affordable Care Act. He supported the first Supreme Court case seeking to repeal the law, and he claimed that the law is “unconstitutional.” And yet, at a news conference last week, Mead echoed many of the Justice Department’s warnings regarding what will happen if the justices side with a new case seeking to gut the law. Indeed, according to the Wyoming Tribune Eagle, Mead “hopes the court will reject the case and uphold the law.”

...In his press conference, Mead worried about the chaos that would result from a decision that allowed all of this to happen. “If on June 30, if that’s when the case comes down, and they say no more subsidies for federal exchanges … it is going to cause a lot of turmoil,” he warned, adding that his home state of Wyoming “will be scrambling” if the King plaintiffs win their case.

OK, I lied; I do have one comment which Gov. Mead might want to pass along to his Republican colleagues in Congress:

OK, this one came out of nowhere, but it's helpful: The Assistant Secretary for Planning and Evaluation (ASPE, the source of the official monthly ACA exchange enrollment reports) and the Director of the Office of Health Reform at the Health & Human Services Dept. just released a new report which states that:

Since several of the Affordable Care Act’s March coverage provisions took effect, about 16.4 million uninsured people have gained health insurance coverage. That includes:

Remember all the fuss and bother back in 2013 over OMG!!! ELEVENTYGAZILLION POLICIES CANCELLED DUE TO OBAMACARE!!!?

Remember how the number of people having their policies cancelled due to not being compliant with minimum Affordable Care Act standards supposedly totalled anywhere from a somewhat reasonable 4-5 million to an absurd 17 million, depending on whether the rightwing source screaming about it was of the rational or batsh*t insane variety?

Well, in the end, it appears that it was only 2.6 million people at most, according to a study by the Urban Institute at the time. However, even that number may be too high, because it also turns out that a lot of people whose policies were originally cancelled were later reinstated after the backlash caused President Obama and the HHS Dept. to allow states to extend those non-compliant policies by 1, 2 or even 3 years.

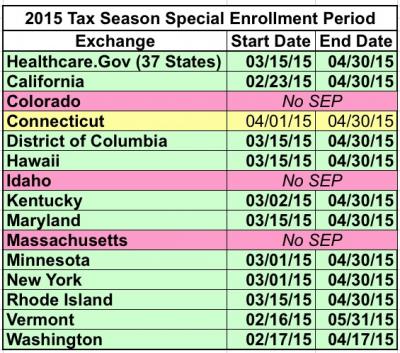

OK...technically speaking, 6 states had already kicked off their Tax Filing Season Special Enrollment Period starting as early as February 17th (Washington State), but for 40 states (plus DC) states, the "encore" edition of 2015 ACA Enrollment officially began today. Connecticut doesn't start theirs for another 2 weeks, and 3 states (CO, ID & MA) are not offering a "tax filing season" SEP. However, those three, like every state, still have the "normal" off-season SEP for people who have significant life changes such as getting married, divorced, giving birth, adopting a child, losing their other coverage or moving to a new state.

Just as a few states starting this SEP early, 2 (Vermont and Washington State) are also ending their Tax Season SEP later than the rest. However, for 46 states, the cut-off is April 30th.

U.S. Senators Barbara Boxer and Dianne Feinstein are calling on California’s health insurance marketplace, Covered California, to allow women to sign up for coverage when they become pregnant.

Under the current rules of the Affordable Care Act, uninsured women who discover they’re pregnant outside of open enrollment periods can only sign up for coverage once the baby is born. The senators sent a letter to Covered California on Wednesday urging the agency to change the policy to make pregnancy a “qualifying life event” that allows women to enroll in coverage at that time.

OK...technically speaking, 6 states had already kicked off their Tax Filing Season Special Enrollment Period starting as early as February 17th (Washington State), but for 40 states (plus DC) states, the "encore" edition of 2015 ACA Enrollment officially began today. Connecticut doesn't start theirs for another 2 weeks, and 3 states (CO, ID & MA) are not offering a "tax filing season" SEP. However, those three, like every state, still have the "normal" off-season SEP for people who have significant life changes such as getting married, divorced, giving birth, adopting a child, losing their other coverage or moving to a new state.

OK...technically speaking, 6 states had already kicked off their Tax Filing Season Special Enrollment Period starting as early as February 17th (Washington State), but for 40 states (plus DC) states, the "encore" edition of 2015 ACA Enrollment officially began today. Connecticut doesn't start theirs for another 2 weeks, and 3 states (CO, ID & MA) are not offering a "tax filing season" SEP. However, those three, like every state, still have the "normal" off-season SEP for people who have significant life changes such as getting married, divorced, giving birth, adopting a child, losing their other coverage or moving to a new state.