Over at The Huffington Post, Jonathan Cohn lays out the potential carnage if the King v. Burwell plaintiffs receive a favorable ruling from the Supreme Court...and why it would be far, far worse than the 2 million or so people whose noncompliant policies were cancelled at the end of 2013 & 2014.

This is the first time I've updated The Graph in awhile, for an obvious reason: Since the end of Open Enrollment (including the "Waiting in Line" extension period) there's only been a tiny smattering of data updates, from Colorado, DC, Maryland, Massachusetts, Minnesota and Rhode Island...and only 2 of those include any of March. Slim pickings indeed. Of course, the #ACATaxTime Special Enrollment Period kicked off on the 15th in most states, so things should have picked up, but unless the HHS Dept. surprises me, you're not likely to hear anything official about it until after April 30th (and possibly not even then). (Update: Yay! They'll issue some sort of enrollment update next week after all!)

Still, based on the snippets of data I do have since 2/22, along with last year's off-season pattern and some educated guesswork for the tax season SEP, here's where I think things should stand as of Monday, March 23rd, 2015...otherwise known as the 5 year anniversary of the Affordable Care Act being signed into law by President Obama (make sure to click the image for a higher-resolution version):

The domain name for D.C. Health Link's website was allowed to expire for 49 minutes earlier this week.

A D.C. website development company discovered the problem Tuesday morning as it tried to use D.C. Health Link's web page for its own employees' coverage. D.C. Health Link, the District's Affordable Care Act exchange, is operated by the D.C. Health Benefit Exchange Authority and has come under fire recently for technical and usability issues.

I can't even...

(sigh) For those who aren't familiar with how domain name registrations work, renewing one takes literally seconds to do, only has to be done once per year, costs a whopping $10 or so per year, and can easily be set up to either autorenew every year or you can register the domain for up to 10 years at a time.

Fox News cited an unnamed "independent expert" to cast doubt on the veracity of recent Affordable Care Act enrollment numbers, which have exceeded 16 million Americans and are reported to have driven the largest reduction in uninsured persons in 40 years.

...On the March 16 edition of Special Report with Bret Baier, host Bret Baier briefly reported on the enrollment numbers, offering the unevidenced claim that "an independent expert says the reality is fewer than 10 million people have signed up."

I suppose I could write a lengthy screed explaining 8 ways from Sunday how utterly full of garbage that is (i.e., if you don't include Medicaid, don't include sub26ers on their parent's plan, don't include off-exchange enrollments and don't bother including the 14 states running their own exchanges), but really...why bother? FOX has literally pulled a number out of their ass here. I can do the same thing:

"FOX News claims that none of their on-air personalities have molested goats. But an independent expert says that at least 40% of them have."

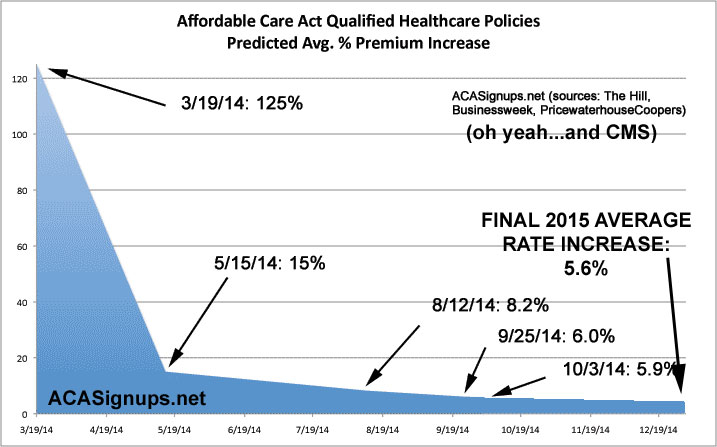

As open enrollment for the second year of the Affordable Care Act’s health coverage expansion begins, a clearer picture of 2015 health insurance rates has emerged. As of November 4, 2014, seven states—Colorado, Maryland, New York, Ohio, Oregon, Rhode Island, and Vermont—as well as the District of Columbia announced approved rates for both on-exchange and off-exchange health plans on the individual market. In total, HRI has collected premium data from 43 states and the District of Columbia.

Among the seven states and DC with final rate announcements, the average premium (across metal tiers and ages) is about $344, andthe average premium increase from 2014 is 3.5%. By contrast, the average premium increase across all reporting states is 5.6%, and the average premium is $381.

The Kaiser Family Foundation has posted a very handy table listing how many people in each state are receiving federal tax credits for ACA exchange-purchased healthcare policies this year, how much those policies would cost (on average) at full price, and what the average tax credit in each state is.

I'm using their data to take this info one step further: If the Supreme Court does tear away the tax credits in states operating on the federal marketplace, just how many people would be screwed by the ruling as a result, both on and off the exchanges? Remember, studies by both the Urban Institute and the RAND Corporation agree that average individual market premiums would rise by at least 35% in those states (and potentially as high as 45% in all states) as a result of such a ruling. The American Academy of Actuaries is taking these projections very, very seriously.

PEMBROKE, Maine — Jeremy Brown has made a living hunting scallops in unforgiving waters off the state’s far eastern tip, where doctor visits are often construed as signs of weakness.

But sometimes his back hurts. His son got sick. Like many in Maine’s coastal fishing communities, he begrudgingly accepted insurance offered to his family through the Affordable Care Act and has come to rely on a federal discount to keep it.

Now, that support may disappear for tens of thousands of families in Maine and New Hampshire.

...The Affordable Care Act, President Obama’s signature legislative achievement, was enacted in 2010 and GOP lawmakers have worked to kill it since. They object to the cost and consider it governmental overreach. But if the law gets uprooted without a viable replacement, Republicans could face a backlash.

Yeah, I know, not exactly an earth-shattering development, but it's a fairly slow news day ACA-wise, and everyone's spazzing out about Hillary Clinton's a) email brouhaha and/or b) her (supposedly) imminent official announcement about whether or not she's gonna run for President next year, so I figured this was worth a post:

Repeal of the ACA would let insurers write their own rules again, and wipe out coverage for 16 million Americans.

But luckily the Constitution supplies a contingency plan, even if the administration doesn’t know it yet: If the administration loses in King, it can announce that it is complying with the Supreme Court’s judgment — but only with respect to the four plaintiffs who brought the suit.

This announcement would not defy a Supreme Court order, since the court has the formal power to order a remedy only for the four people actually before it. The administration would simply be refusing to extend the Supreme Court’s reasoning to the millions of people who, like the plaintiffs, may be eligible for tax credits but, unlike the plaintiffs, did not sue.