For 2016, HMSA has proposed a 45.5 percent rate increase for their individual HMO plan, and nearly a 50 percent rate hike for their individual PPO plan (49.1 percent overall). The carrier justified their rate hikes based on claims costs, explaining that while virtually everyone in Hawaii was already insured, the uninsured pool – many of whom purchased new ACA-compliant plans – had significant medical needs.

Ouch. Yup, that's a pretty ugly requested increase, no way around it.

The following day, Kaiser proposed an 8.7 percent rate increase for their individual market policies.

If approved as is, this would have resulted in a 33.7% average rate increase, when weighted by market share between the two companies.

About a month ago, I crunched Nevada's individual and small group rate hike numbers and concluded that the overall weighted average hike in the Silver State next year (assuming everyone stays put and doesn't shop around) will be roughly 9.6% on the individual market and just 5.3% for small businesses.

Now, it's not the lower rate which caught my eye; the 8.7% figure only includes exchange-based carriers, of which there's only three this year, versus the dozen or so who operate throughout the state (there are 9 more insurance carriers who are only operating off of the exchange).

What I'm puzzled by is this part...which also includes some good news:

I realize this is mostly off-topic (although certainly gun violence overlaps with healthcare, both in terms of emergency room expenses as well as mental health services), but I couldn't resist posting about it.

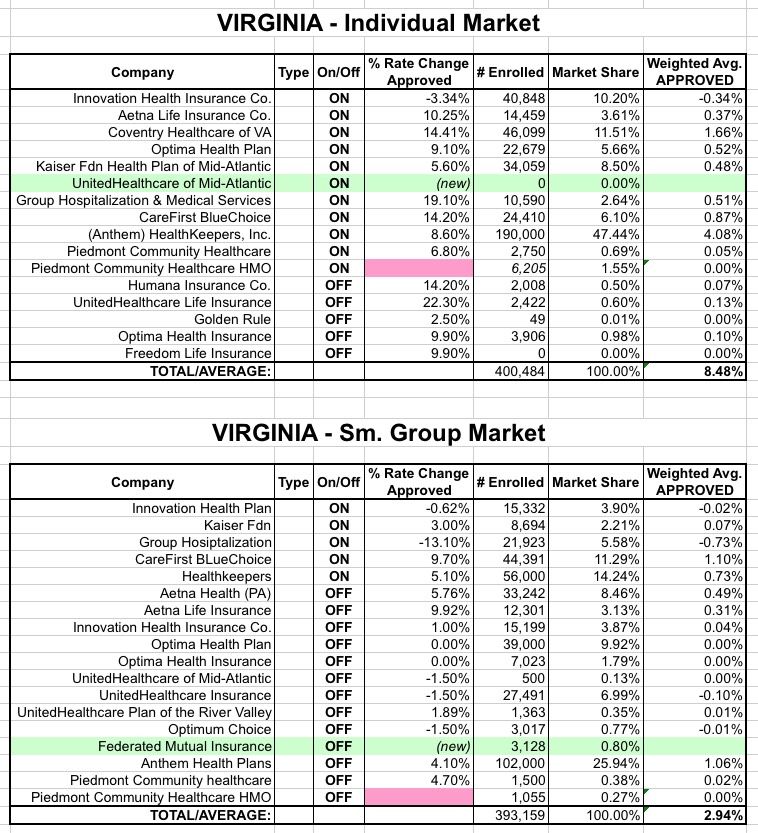

Some relatively welcome news going into the home stretch: After a series of ugly (over 20%) rate hike averages from Alabama, Delaware, South Dakota and especially Minnesota, I've just completed the Virginia analysis:

Unlike many other states, there's no guesswork or educated guesses here; the Virginia Dept. of Insurance SERFF filings are quite complete and straightforward, so I have every company providing individual and/or sm. group coverage listed, both on and off the exchange, with the exact average rate changes and affected enrollee numbers for pratically every one of them.

The only exceptions are Piedmont Community Healthcare HMO, whose SERFF filings, oddly, included the enrollee count but not the rate change (usually it's the other way around). In addition, there's a couple of new additions to each (UHC of Mid-Atlantic on the indy market, Federated Mutual on the sm. group market). However, none of these have large enough enrollment numbers to amount to more than a rounding error in either category.

CodeBaby, a provider of Intelligent virtual assistant technology, today announced Connect for Health Colorado® and Access Health CT have expanded the use of CodeBaby as a way to increase consumer education and improve the online experience for customers purchasing health insurance during the 2016 open enrollment period.

Connect for Health’s virtual assistant, Kyla, can be found at key points in the website, presenting important information in a clear manner, assisting users in making informed decisions, and providing decision support for critical choices. In time for this year’s open enrollment, Connect for Health has expanded Kyla to the Subsidy Eligibility System so that the avatar can answer questions, help people determine if they are eligible for subsidies, and walk them through the enrollment process.

Gov. Shumlin Updates on Vermont Health Connect Progress

MONTPELIER – Gov. Peter Shumlin, representatives from Vermont’s insurance carriers, and officials and staff from Vermont Health Connect (VHC) gathered today to update on the health insurance marketplace’s progress. The Governor announced that the technology upgrade necessary for a smooth open enrollment has been delivered and tested and will be deployed starting this evening; the backlog of change of circumstance cases has been cleared; VHC is now operating at a vastly improved customer service level for change requests; and customers will be able to report many changes online starting Monday. Meeting those milestones is consistent with the schedule laid out by the Governor in March 2015 and in legislation passed later in the spring.

NOTE: I originally posted this at 3:00pm October 1st. Shortly after that, I heard the news about the Oregon massacre. I seriously debated changing the headline, but decided that it was completely appropriate under the circumstances. If you disagree...well, we just have to disagree.

In 1991, conservative writer/humorist P.J. O'Rourke wrote a book called, fittingly enough, "Parliment of Whores". It was, as the title explains, "A Lone Humorist Attempts to Explain the Entire U.S. Government". The 9th chapter is entitled "Would you kill your mother to pave I-95?" The main point of this chapter, as you can probably imagine, is that there's a limited amount of money in any budget which can be set aside for various programs and departments, which in turn means that Tough Choices have to be made all the time:

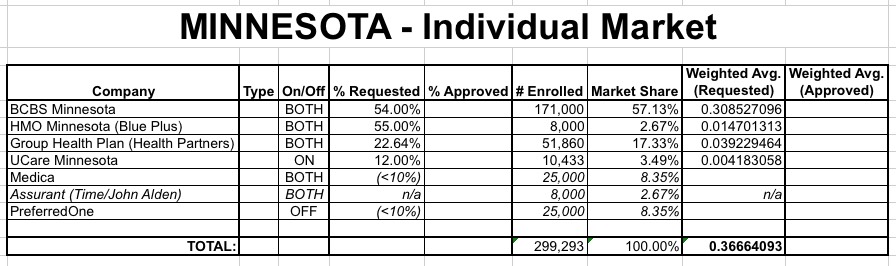

When I crunched the numbers for Minnesota's requested rate hikes, the results were pretty scary-looking; based on partial data, I estimated that the weighted average was something like a 37% overall requested increase:

Note that there were several crucial missing numbers: I didn't know the actual market share for several companies (I made a rough guess based on an estimate of the total missing enrollments), nor did I know what the requested increases were for Medica or PreferredOne, other than thinking that both were under 10%.

With the 2016 Open Enrollment Period quickly approaching (it launches on November 1st), the Maryland Health Connection has already officially launched 2016 Window Shopping!

They even whipped up a simple video stepping you through the process (oddly, the background music seems to have been lifted from "There's Something About Mary", which is either a good or bad omen depending on your POV):

Over the weekend I finally started plugging every state which have 2016 premium hike data for into a chart to see if any patterns were showing up, but I was still missing 6 states. I concluded that Medicaid expansion does not appear to be a major factor (or, at least, not an obvious one), but that there are two other clear trends:

First, states which are allowing "transitional" plans through next year are definitely seeing higher percentage rate hikes than those which stuck to their guns and discontinued non-ACA compliant policies.

Second, states which have only published requested rate changes are currently noticeably higher on average than those which have been put through the regulatory approval process.

Today I'm posting updated versions of all three charts, with some slight updates: