In computer science, GIGO means that a faulty input will result in a faulty output. Perhaps GIGO in the specific area of Obamacare enrollment projects should be Gaba In, Gaba Out since many leftwing sites are currently singing the praises of one Charles Gaba, a blogger who is projecting incredibly high Obamacare numbers. And now the Washington Post's Wonkblog writer, Jason Millman, is the latest person to be enthralled by the very convenient Obamacare numbers served up by Gaba. Here is Millman singing his Gaba paean:

The Obama administration on Monday announced that 5 million people had signed up for Obamacare exchange plans. Hours earlier, a self-employed Web developer from Michigan had already predicted the milestone would be hit on Monday.

UPDATE: 1/13/15: I've modified my final #OE3 projection; I'm now projecting a range of anywhere between 13.8 - 14.2 million (but I'll still be judging myself based on how close I came to the 14.7M figure, however.)

That's 2 in one day, the 8th to fold to date and the 4th one which can be specifically connected the Risk Corridor Disaster:

Health Republic Insurance Not Offering Plans in 2016

Lake Oswego, Ore. (Oct. 16, 2015) –Health Republic Insurance, a non-profit health insurance carrier, announced today that it will not offer small group or individual plans on or off exchange in 2016. All current Health Republic individual and small group policies remain in full effect through the end of 2015. Members can continue to see plan providers and claims will be paid under plan terms.

The federal government recently announced it would pay insurance companies only 12.6% of their risk corridor receivable for the 2014 plan year and has created industry-wide concern about when, or if the 2015 risk corridor would be paid.

The program has been under siege from the start, including from the insurance industry. Before the law’s passage, government grants to help them get going were switched to loans. None of that money could go for advertising — a wounding rule for new insurers that needed to attract customers. Moreover, the amount available was cut from $10 billion to $6 billion and then later, as part of the administration’s budget deals with congressional Republicans, to $2.4 billion. Federal health officials abandoned plans for a co-op in every state.

So, let's see here: You're trying to create start-ups to enter an existing, mature market which is already dominated by major, behemoth-sized competitors which have almost unlimited funds. Naturally it makes total sense to a) make the seed money a loan with a tight payback time table; b) prevent them from advertising in a saturated market; and c) slash their budget by 75%.

Hold on tight, this is gonna be a big one; it covers stories dating back several weeks, so some of these might be completely irrelevant at this point, but...

I've promised not to reveal the actual number anywhere else until tomorrow, so you'll have to read the full piece to get my call...but I do have some important caveats, disclaimers and additional points which I can make here as well:

*IMPORTANT: This assumes that everyone currently enrolled sticks with their current policy next year. If enough people shop around and consider their options, the average premiums for various plans, various companies, in vartious states and nationally could end up being considerably lower (possibly coming in under 10% overall).

Again: Do not blindly autorenew! Contact your ACA exchange website/call center (or your insurance carrier, if you're enrolled directly through them) and check out your options before committing to your existing plan! In many cases, there will be a different plan which is a better value for you!

At last!! It's been extremely frustrating trying to lock down the 2016 average premium hikes for Pennsylvania, especially because their Insurance Dept. website has actually been very good about posting every requested rate change in an easy-to-read, comprehensive fashion.

The problem with PA's rate filings hasn't been on the percentage change side, it's on the covered lives side. I was able to compile enrollment numbers for some carriers but not others...including First Priority, which was requesting a 29.5% rate hike. Without knowing whether they had a huge chunk of the market or not, posting the "average" rate hikes without including theirs was kind of meaningless, since it could potentially jack that average up or down dramatically.

So, I finally kind of gave up on it, figuring that even when the approved rates were posted, they probably still wouldn't include the number of covered lives for each insurance company.

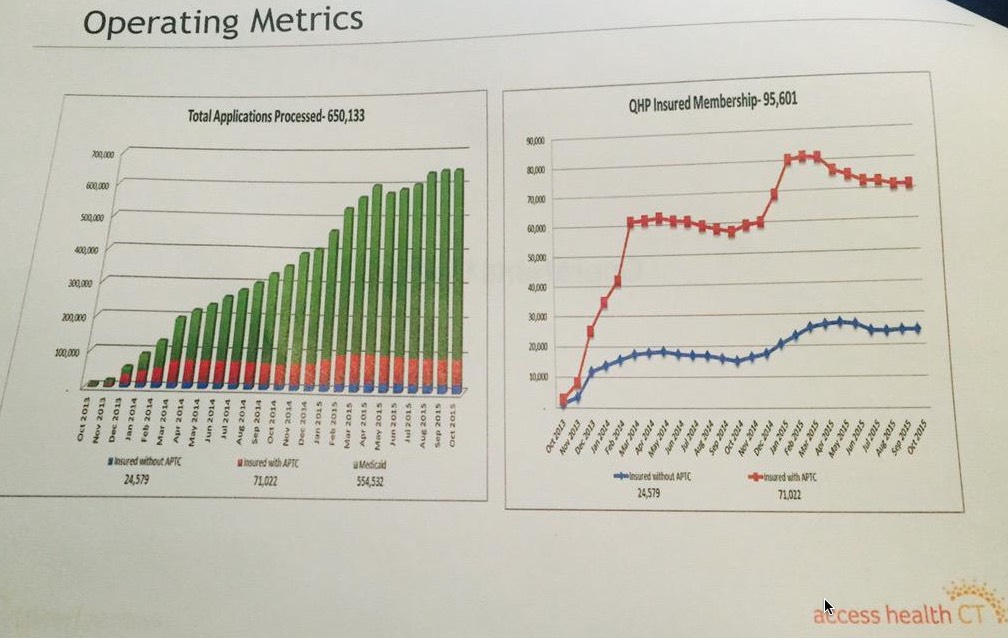

A quick update from Connecticut: Last month it looked like effectuated QHP enrollment at AccessHealthCT had increased a bit between June and September, from around 92.2K to 96.6K.

However, just moments ago at the AccessHealthCT board meeting, this graph was displayed, showing that effectuated enrollment has actually been dropping off gradually since March, which is actually exactly what you'd normally expect via normal attrition anyway.

In any event, according to this slide, CT currently has 95,601 effectuated QHP enrollees: 71,022 receiving tax credits (74%), 24,579 without (26%), which is down slightly from September. This is right in line with my (revised) national attrition estimates, which should taper off at around 9.7 million effectuated enrollees by the end of the year.