Consumer Interest Surges as First Key Deadline Approaches for Covered California and the Individual Market

More than 150,000 new consumers selected a plan through Dec. 12.

Consumer interest is surging, with more than 28,000 consumers selecting a plan during the past three days.

Consumers must sign up by Dec. 15 in order to have their coverage start on Jan. 1, 2019. Open enrollment in California continues through Jan. 15.

SACRAMENTO, Calif. — Covered California announced today that 150,191 new consumers signed up for coverage through Dec. 12. Consumer interest is once again surging ahead of a key deadline, with more than 10,000 people signing up on Wednesday, and more than 28,000 selecting a plan within the past three days.

Last week I acquired the DC Health Link enrollment data for the first two weeks of 2019 Open Enrollment. It showed that DC, unlike most of the other state-based exchanges, was lagging behind last year for the first two weeks (although not as much as most of the HC.gov states).

Well, I just received updated data out of DC and the enrollment situation over the following four weeks didn't improve (if anything they dropped off slightly more):

Nov. 1 - Dec. 11, 2017: 19,252 QHP selections

Nov. 1 - Dec. 11, 2018: 17,825 QHP selections

That's a drop of around 7.4% year over year so far.

As with most other state-based exchanges, the numbers for both years include auto-renewals, which means the vast bulk of 2019 enrollments are likely already baked in. Last year's final tally was 19,289; DC has already reached 92% of that as of 12/11. Keep in mind that DC's Open Enrollment Period does not end on Saturday the 15th; it continues for another 47 days after that, through January 31st.

So, how likely is HC.gov to reach last year's total in the final week? Well...not very likely, but let's do the math anyway. Again, this is for the 39 states hosted by HC.gov only; it does NOT include the 12 state-based exchanges, which are mostly AHEAD of last year so far.

Last year, 8,743,642 people selected QHPs via HC.gov total:

4,580,782 actively re-enrolled

1,702,429 were auto-reenrolled

2,460,431 were new enrollees

Of those 8.74 million total, there are likely around 6.16 million currently enrolled as of December

Last year, 97% of those still enrolled as of December re-enrolled (actively or passively). If that holds true this year, that'll be around 5.97 million total renewals

That means HC.gov would need 2.77 million new enrollees total

In week six of the 2019 Open Enrollment, 934,269 people selected plans using the HealthCare.gov platform. As in past years, enrollment weeks are measured Sunday through Saturday. Consequently, the cumulative totals reported in this snapshot reflect one fewer day than last year.

Every week during Open Enrollment, the Centers for Medicare & Medicaid Services (CMS) will release enrollment snapshots for the HealthCare.gov platform, which is used by the Federally-facilitated Exchanges and some State-based Exchanges. These snapshots provide point-in-time estimates of weekly plan selections, call center activity, and visits to HealthCare.gov or CuidadoDeSalud.gov.

The final number of plan selections associated with enrollment activity during a reporting period may change due to plan modifications or cancellations. In addition, the weekly snapshot only reports new plan selections and active plan renewals and does not report the number of consumers who have paid premiums to effectuate their enrollment.

Definitions and details on the data are included in the glossary.

Unfortunately, Vermont is one of the three states (along with Idaho and Maryland) which hasn't released any 2019 Open Enrollment data yet, so I don't have any numbers to report on that front. However, they did just post this "Open Letter" which I found interesting. The two things to keep in mind about Vermont are: 1) they include their own subsidies on top of ACA subsidies; and 2) they were among two states (North Dakota is the other one) which upgraded their premium pricing in 2019 from "no load" to full #SilverSwitcharoo status.

You can read about the wonky mechanics of this here, but the bottom line is that Vermont residents who qualify for subsidies have substantially better deals available this year, while unsubsidized enrollees have an important workaround to avoid being stung with extra CSR costs:

So, my wife and I finally got around to renewing our own ACA exchange plan the other day (yes, I'm realize how ironic it is that I've spent the past 41 days screaming at everyone else to #GetCovered while waiting until the last week to do so myself. We're a bit busy this month. Don't @ me.)

Anyway, we went through a lot of research and discussion (including assistance from fantastic folks who know more about this stuff than me like Louise Norris and David Anderson) about whether to stick with our existing Gold HMO (we have some pricey issues to deal with) or to switch to a Bronze HMO...but with a Health Savings Account.

I know very little about HSAs, but Dave and Louise suggested I look into one so we did. In our particular case, we decided to stick with the Gold plan in the end for reasons I'd rather not get into...but along the way, while researching our actual 2018 medical claims and expenses, I noticed something rather important. See if you can figure out what it is:

The midterms are over, and the Democrats won back the U.S. House, so the ACA is (mostly) safe at last, right?

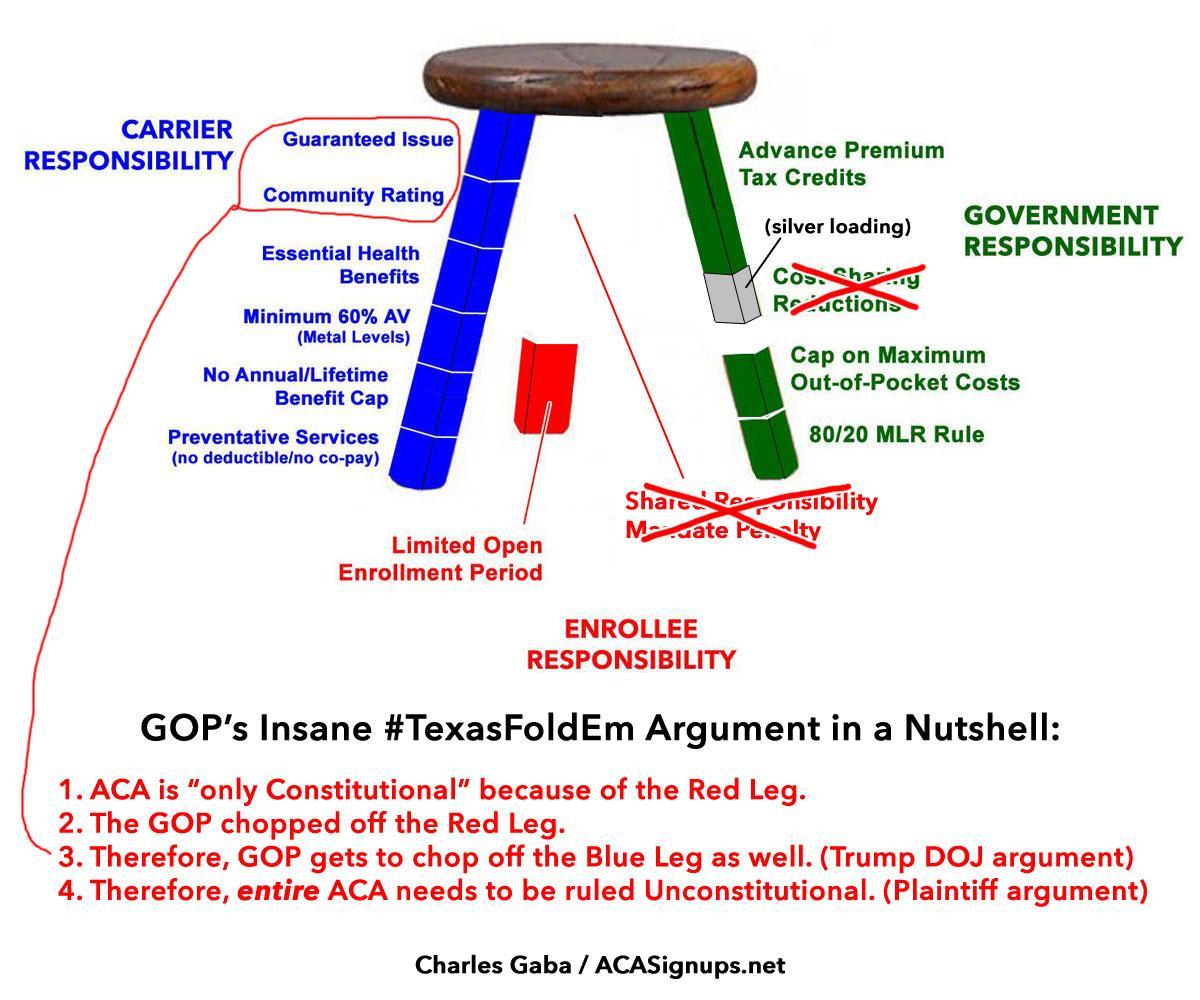

Well...maybe. In addition to the ongoing regulatory sabotage by the Trump Administration to undermine, weaken and generally piss all over the law as much as possible, there's also still a little thing called Texas vs. Azar, aka the #TexasFoldEm federal lawsuit. Oral arguments were held way back in early September, and right-wing Judge O'Connor claimed that he'd rule on a preliminary injunction "quickly" afterwards.

As a reminder, here's the #TexasFoldEm case in a single image:

Deadline to Apply for Health Insurance for the 2019 Plan Year is Dec. 15

Nine in 10 Idahoans Qualify for a Tax Credit to Help Lower Monthly Premiums

BOISE, Idaho – Idahoans wanting health insurance coverage starting on January 1, only have a few days left to enroll in a plan for 2019 with Your Health Idaho, the state’s health insurance exchange. Idahoans must complete their application by midnight, December 15 in order to have coverage at the start of the new year. In response to high demand, Your Health Idaho is extending its support center hours to help customers enroll or answer any questions.

Again, I realize that doesn't mean much of anything on its own; I haven't a clue what counts as "high demand" in Idaho or how it differs from prior years. Still, it does suggest that things are running smoothly at the Idaho exchange.

They just updated that tally for me: 104,162 signups as of EOD 12/6.

Last year, MNsure broke 100,000 enrollments as of 11/23 and 101,626 as of 12/15, which should have put them at right around 100,900 QHP selections as of 12/06/17. That means the current total is around 3.2% ahead of the same point last year.

It's important to note that unlike most states, Minnesota's 2019 Open Enrollment Period doesn't end on the 15th (although you do have to sign up by then in order to have coverage start on January 1st); Minnesotans still have until January 13th to enroll (anyone who enrolls after 12/15 will have their coverage kick in on February 1st instead).