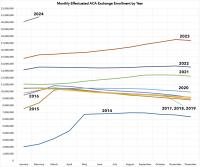

While it's unfortunate that neither 2014 nor 2015 were included, I have partial data for the first two years of the ACA exchanges from a similar post I put together back in 2019.

It's important to understand the difference between someone selecting a Qualified Health Plan (QHP) from one of the ACA exchanges during the Open Enrollment Period and someone actually being enrolled in an effectuated policy...that is, just because you sign your family up for a policy on HealthCare.Gov or a state-based exchange, you aren't considered effectuated until you actually pay your first monthly premium.

While nearly 21.5 million Americans selected Qualified Health Plans (QHPs) via the federal and state ACA exchanges/marketplaces during the official 2024 Open Enrollment Period (along with an additional 1.3 million signing up for a Basic Health Plan (BHP) program in New York & Minnesota, which CMS continues to inexplicably treat as an afterthought in such reports), not all of them actually pay their first monthly premium (for January) for various reasons:

Normally, states will review (or "redetermine") whether people enrolled in Medicaid or the CHIP program are still eligible to be covered by it on a monthly (or in some cases, quarterly, I believe) basis.

However, the federal Families First Coronavirus Response Act (FFCRA), passed by Congress at the start of the COVID-19 pandemic in March 2020, included a provision requiring state Medicaid programs to keep people enrolled through the end of the Public Health Emergency (PHE). In return, states received higher federal funding to the tune of billions of dollars.

As a result, there are tens of millions of Medicaid/CHIP enrollees who didn't have their eligibility status redetermined for as long as three years.

It's been a long, long time since I've written about the "Sub26ers"...that is, the population of Americans age 18 - 25 who are enrolled in the same healthcare policy as their parents thanks to the ACA's provision mandating that insurance carriers allow them to do so. While I may be missing a more recent article, the last time I recall writing anything in depth about this was nearly a decade ago:

Long-time readers will remember that throughout the 2014 Open Enrollment period, there was much fuss and bother made by both the Obama administration, the HHS Dept., myself and some ACA detractors over the "sub26er" population: Young adults aged from 19-25 years old who are covered by their parents policies thanks to provisions in the Affordable Care Act requiring all new policies issued since 2010 to allow this.

At the time I was a bit obsessed with trying to suss out just how many Americans fell into this particular category. It was a tricky number to pin down for a number of reasons, but in the end it seemed to hover somewhere in the 2 - 3 million range, depending on your source.

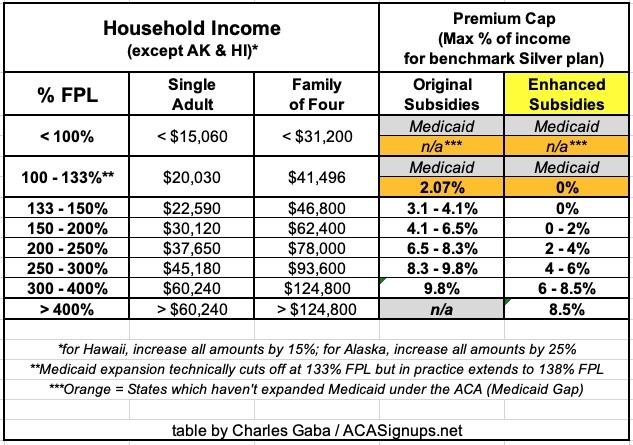

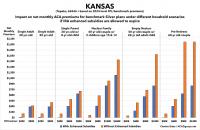

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula: