Kansas is another state where the annual rate filings are redacted for many of the carriers; as a result, I can only run a semi-weighted average, and even that is dependent on my estimate of the total individual market size being accurate (my general rule of thumb as long as the enhanced subsidies of the IRA are in place is that about 90% of most states individual market enrollment is on-exchange unless I have data proving otherwise).

With that in mind, the carriers on the Kansas individual market are asking for rate hikes ranging from 2.1% - 24.4%, with an estimated semi-weighted average of 8.9%.

For the small group market, I can't even run a semi-weighted average since I have no idea what the KS small group market size is overall, but the unweighted average rate hikes being requested is 14.9%.

It's also worth noting that unless I'm missing something, US Health & Life Insurance seems to be pulling out of the Kansas individual market, while both Aetna and Cigna seem to be missing from the small group market.

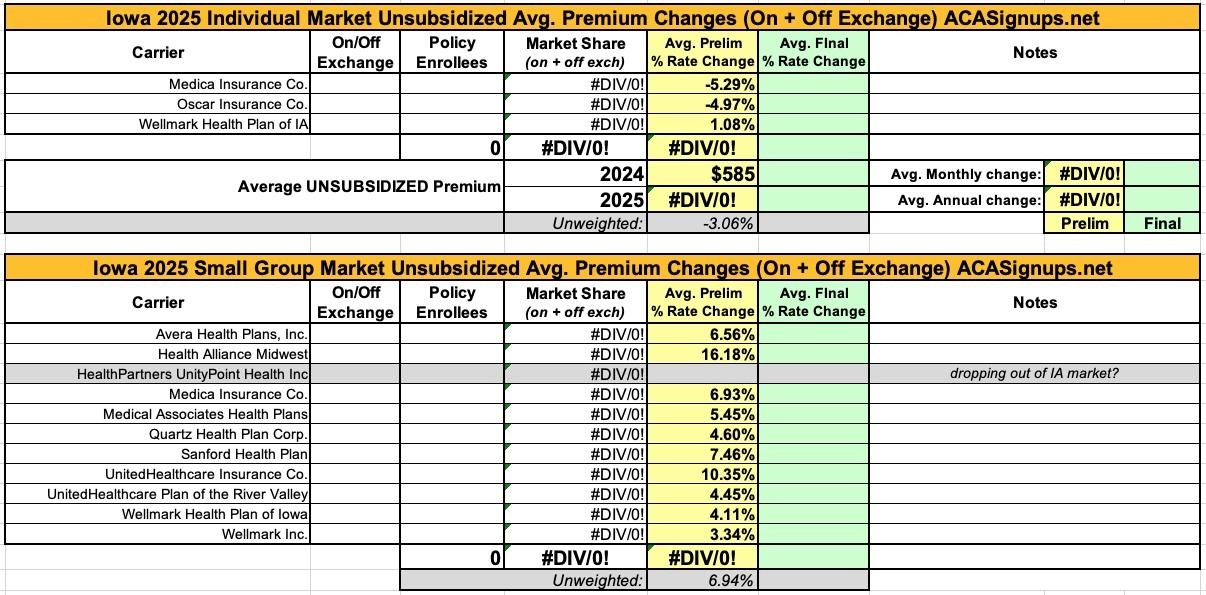

Here's the preliminary 2025 ACA individual and small group market rate filings. Unfortunately, the effectuated enrollment isn't available this year for the carriers in either market, so I can only offer unweighted averages...which include a 3.1% reduction on the indy market and a 6.9% increase for small group enrollees.

the only other noteworthy item is that it looks like HealthPartners UnityPoint is dropping out of Iowa's small group market next year...but with 9 other carriers participating there's still plenty of options for that population.

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request. Huge kudos to the GA OCI folks!

Georgia's individual market has grown dramatically over the past two years; it went from 660,000 in 2023 to 813,000 people in 2024 to a stunning 1.3 MILLION this year. The weighted average rate increase for unsubsidized enrollees will go up 9.9% if state regulators approve all of the carrier requests as is.

The Biden-Harris Administration today continued its historic investment in health care coverage and the Affordable Care Act (ACA) by awarding a new round of $100 million to organizations vital to helping underserved communities, consumers, and small businesses find and enroll in quality, affordable health coverage through HealthCare.gov, the Health Insurance Marketplace®.

The Centers for Medicare & Medicaid Services (CMS) is awarding the grants, in advance of this year’s Marketplace Open Enrollment (which begins November 1, 2024) to 44 Navigator grantees in states using HealthCare.gov. The grants are part of a commitment of up to $500 million over five years — the longest grant period and financial commitment to date, and a critical boost for recruiting trusted local organizations to better connect with those who often face barriers to obtaining health care coverage.

The Inflation Reduction Act is saving Americans millions in lower prescription drug costs and making health insurance more affordable.

Two years ago today, President Biden signed into law historic legislation to lower health care costs for millions of Americans. The Inflation Reduction Act, also known as the lower cost prescription drug law, created the first ever annual cap on out-of-pocket drug costs for people with Medicare, capped the cost of each covered insulin at $35 per month, granted Medicare the power to directly negotiate drug prices, and made Affordable Care Act (ACA) marketplace plans more affordable, leading to the lowest uninsured rate in history.

In a historic moment that will help lower prescription drug prices for millions of people across America, the Biden-Harris Administration announced that it has reached agreement for new, lower prices for all 10 drugs selected for negotiations. These negotiated drugs are some of the most expensive and most frequently dispensed drugs in the Medicare program and are used to treat conditions such as heart disease, diabetes, and cancer. The new prices will go into effect for people with Medicare Part D prescription drug coverage beginning January 1, 2026.

via Covered California: (this is actually from nearly a month ago; somehow I missed it at the time):

SACRAMENTO, Calif. — Covered California announced its health plans and rates for the 2025 coverage year with a preliminary weighted average rate increase of 7.9 percent.

The rate change can be attributed to many factors, including a continued rise in health care use, increases in pharmacy expenditures, the rising cost of care, labor shortages and other issues affecting the health care industry.

Because of the robust financial help available to Covered California enrollees, many will see a small impact, if any, to their monthly cost. Covered California, with the support of Gov. Newsom and the California Legislature, has worked to reduce the impact of increased consumer costs in 2025 by providing more support for its state-enhanced cost-sharing reduction (CSR) program, which will eliminate deductibles and lower the cost of care for over a million Californians.

The good news about New Hampshire's health insurance market is that they're the only state without its own ACA exchange which produces publicly-accessible monthly reports on individual on-exchange market enrollment. The bad news is that they don't seem to publish the actual rate filings in an easy-to-read format, which means I'm left with the federal rate review website, which sometimes posts average rate requests which don't match up with the actual filings...but it's gonna have to do here.

With these two data sources in hand, New Hampshire's individual market carriers are asking for a weighted average increase of 4.8%. It's important to note that Anthem Health Plans and Matthew Thornton Health Plan are listed as separate carriers on the federal Rate Review website (with separate average rate requests), but on the state's monthly report, they're merged into a single listing.

With no way of knowing what the actual enrollment breakout is between these two, I'm assuming a 50/50 split.

Each year, the Idaho Department of Insurance posts rate changes of individual and small group health insurance products so consumers can review and provide comments on the proposed increases. Insurance companies submit proposed rates for the upcoming calendar year to the Department, along with descriptions and justifications for why the rates are reasonable and not excessive. The Department of Insurance is seeking public input for rate changes of individual and small group health insurance products to improve insurer accountability and transparency. By following the links below, the public can access a summary of the increase amounts and the carrier justifications for the rates. Please submit any comments to the Department for consideration.

The good news is that the federal Rate Review database has now posted the preliminary avg. 2025 rate filings for the individual and small group markets for every state. This makes it very easy to plug in the average requested rate changes in 2025 for every carrier participating in both markets.

The bad news is that most of the underlying filing forms are heavily redacted, meaning I can't use the RR database to acquire the other critical data I need in order to run a proper weighted average: The number of people actually enrolled in the policies for each carrier.

This means that in cases where this data isn't available elsewhere (either the state's insurance department website, the SERFF database or otherwise), I'm limited to running an unweighted average. This can make a huge difference...if one carrier is requesting a 10% increase and the other is keeping prices flat, that's a 5.0% unweighted average rate hike...but if the first carrier has 99,000 enrollees and the second only has 1,000, that means the weighted average is actually 9.9%.