Sen. Richard Burr (R-N.C.) said Thursday that Republicans might not be able to pass an alternative to ObamaCare until 2017.

Burr, along with Sen. Orrin Hatch (R-Utah) and Rep. Fred Upton (R-Mich.) unveiled a GOP replacement plan for ObamaCare on Wednesday. But, appearing the next evening on Fox News's "Special Report with Bret Baier," Burr said no single idea is likely to generate consensus.

"I don't think so," he said. "I think that there are going to be a lot of ideas not only in Congress but around the think tanks here in Washington and around the country."

Some positive news to cushion the blow of the CoOportunity meltdown...

Y'know, there's all sorts of ways to spin formal press releases.

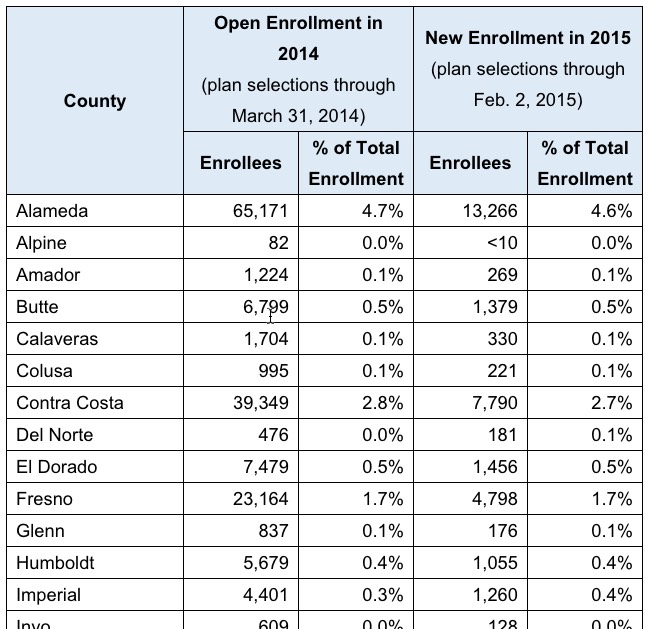

For instance: Moments ago, the HHS Dept. of the United States sent out this press release, touting the fact that about 6.5 million people who selected private policies via Healthcare.Gov for 2015 (about 87% of the 7.5 million total confirmed via the federal exchange) qualify to receive tax credits to help cover the cost of their health insurance premiums. The average tax credit for those 6.5 million people is $268/month, or $3,216 per year:

FOR IMMEDIATE RELEASE

Monday, Feb. 09, 2015

Almost 6.5 million consumers qualify for an average tax credit of $268 per month through the Health Insurance Marketplaces

The Feb. 15 deadline is just six days away; 8 in 10 consumers can get coverage for $100 or less

Outgoing Republican Pennsylvania Governor Tom Corbett tried a desperate hail mary play to save his job: Expanding Medicaid via the Affordable Care Act, but doing it in an absurdly complicated and confusing way in order to appease his Republican base. It didn't work; he lost to Democrat Tom Wolf, one of the few bright spots for the Dems in an otherwise lousy 2014 election.

I'm not a lawyer, but I've always understood that in order for a case to be brought to court, there generally has to be, you know, a plaintiff. That is, as far as I know, a lawyer can't just file a suit and have it taken up by the Supreme Court of the United States just because they don't happen to approve of a law; there has to be someone who can claim that they were actually harmed by it (or at least by a particular provision of the law as enacted or enforced). Alternately, they have to at the very least have "standing" to challenge the law under the legal definition of such, no matter how thin the argument may be.

In December, Tennessee Gov. Bill Haslam, a Republican, got the deal he wanted from the Obama administration: Tennessee would accept more than $1 billion in federal funding to expand Medicaid, as allowed for in the Affordable Care Act, but Obama aides would allow Haslam to essentially write staunchly conservative ideas into the program's rules for the state. He dubbed the reformed Medicaid program "Insure Tennessee."

But the state's chapter of Americans for Prosperity, the national conservative group whose foundation is chaired by controversial billionaire David Koch, argued Haslam was just trying to trick conservatives into implementing Obamacare in their state by giving it a new name. AFP campaigned aggressively Haslam's plans for the next six weeks, even running radio ads blasting GOP state legislators who said they might vote for it.

On Wednesday, Haslam's bill died in a committee of the Tennessee state senate. The vote was one of the clearest illustrations of the increasing power of AFP and other conservative groups funded in part by the Koch brothers.

Technically speaking, there could be one more "weekly snapshot" after this Wednesday's, since those reports run through the previous Friday...except that would be kind of silly, since Sunday the 15th is the final day of the open enrollment period anyway. I find it difficult to believe that HHS would issue a report next Wednesday which leaves off the final 2 days of the period (which are also likely to be the busiest yet).

Anyway, on Wednesday the 11th, HHS should issue a report including all HC.gov QHP selections as of Friday the 6th. I'm expecting the total to be roughly 7.75 million, or about 276K for the week.

National QHP selections, including all 14 state-based exchanges, should have been roughly 10.32 million as of Friday, and should have started to ramp up significantly over this weekend. In fact, I'm anticipating hitting around 10.48 million by midnight Sunday...which should mean roughly 9.2 million paid enrollees.

In other words, we've finally broken through the HHS Dept's official exchange-based private policy enrollment projection for 2015.

Kentucky's previous update had them at 92,886 QHPs and 38,547 additional Medicaid enrollees via kynect, as of 1/22.

Today's update brings these numbers up to 95,927 QHPs and 46,422 added to Medicaid, increases of 3,041 and 7,875 respectively (through yesterday).

That's 217/day on the private side, during a the slow patch. In order to reach the HHS target of 107K QHP selections, they'll have to average 1,100 per day. With the expected deadline surge, this will be tough but doable. Reaching my KY target of 130K, on the other hand, would need 3,400/day, which doesn't seem to be in the cards.

2014/2015 Open Enrollment stats as of Thursday 2/5/2015:

The last MNsure update was 1/25, when they had 44,331 QHP selections. Since then, they've added just 1,642 more...or about 150/day. In order to reach their lowered target of 67K by 2/15, they'll need to add 2,100/day for 10 days straight. I just don't see them pulling that off.

Still, if they can reach, say, half of that, they'll add another 11K, which would bring their total up to perhaps 57,000, which isn't unreasonable.

Meanwhile, Minnesota's Medicaid/MinnesotaCare tally is up to 78,863 combined.

February 6, 2015

MNsure will release 2015 enrollment metrics weekly, and will present a more robust metrics summary to the MNsure Board of Directors at each regularly-scheduled board meeting. During weeks that MNsure is closed on Friday, the enrollment metrics update will be released earlier in the week.

Health Coverage Type Cumulative Enrollments

Medical Assistance 57,593

MinnesotaCare 21,270 Qualified Health Plan (QHP) 45,973

TOTAL 124,836

As of January 26th, California's 2015 QHP selection total was at least 1.217 million people. I say "at least" because the actual renewal number is a bit fuzzy (it's either 944K or 947K depending on whether you go by the CoveredCA or HHS/ASPE report). Anyway, today they issued a press release which at least updates the new enrollee number...if you do the math:

(etc etc...too long to post the whole list)

Add them all up and you get 288,568 new enrollees for 2015. Add those to the 944K (minimum) renewals from 2014 and you get 1,232,568 or more through Feb. 2nd.

Since the prior number was 1,217,111 as of 1/26, that's an average of around 2,200/day over the course of the slowest patch of the enrollment period.

Yesterday I lamented the fact that the Washington State ACA exchange seemed to be seriously lagging behind just about every other state in terms of achieving their 2015 QHP selection target, with only 132K QHPs to date vs. the 215K that they were hoping to reach this year (not to mention my personal target of 250K, which turns out to have been way out of line).

I figured that they're on track to only end up with perhaps 180-190K by 2/15, coming up 25K - 35K short of their goal.

However, IBD's Jed Graham (who has been on fire lately; this is the 2nd important point he's brought to my attention this week) reminded me that last year, unlike every other state except Massachusetts, Washington only reported paid enrollments, not total plan selections. If that's true this year as well, he noted, then I've been missing roughly 12% of WA's total all along (put another way, I should be plugging that 132K number into the paid column, not the total column).