As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

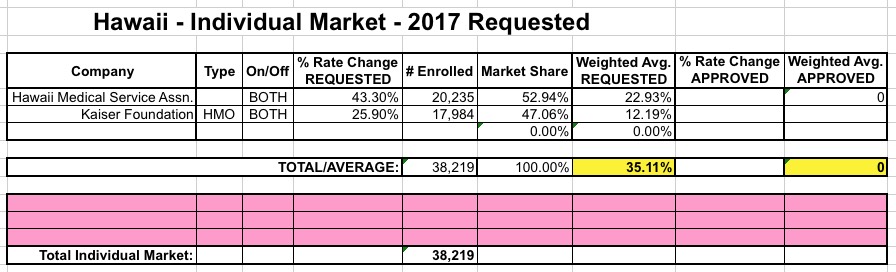

There are only two insurance carriers participating in Hawaii's individual market next year: The Hawaii Medical Service Association (HMSA) and the Kaiser Foundation Health Plan.

As I noted Monday, I believe August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

In 2014, New Jersey's total individual market was estimated at around 261,000 people, including off-exchange, grandfathered and transitional enrollees. Assuming 25% growth, this should be around 325,000 today.

As I noted Monday, I believe August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

Today is August 1st. I was hoping that most/all of the states still missing from my 2017 Requested Rate Hike project would finally make their rate filings public as of today, but apparently not (or at least, they aren't live as of 10am).

Health plans sold on Michigan's insurance exchange could see an average 17.3% increase next year, and if recent history is any guide, state regulators could approve the insurance companies' rate hike requests without many — if any — changes.

The rate increases would mean a financial hit for taxpayers in general and the 345,000 Michiganders who buy their health insurance on the Healthcare.gov exchange, created under the Affordable Care Act, also known as Obamacare.

Regular readers know that I used to regularly post an entry about the official CMS Medicaid enrollment reports every month, documenting the increase in Medicaid enrollment since ACA expansion went into effect. The numbers were increasing dramatically every month for nearly two years, but started slowing down last fall as most of the expansion states started maxing out on their eligible enrollees.

As of November 2015, there had been a net increase of 14.1 million people added to the Medicaid rolls since October 2013 (the month when ACA expansion enrollment began), plus another 950,000 people who had already been quietly transferred over to Medicaid from existing, state-funded programs prior to 2013 via other ACA provisions.

There's been numerous mentions this week at the Democratic National Convention about Hillary Clinton's role in creating the Children's Health Insurance Program (CHIP), and with good reason.

The number which keeps getting thrown around is "over 8 million" (which is true), while the official CHIP website lists it as 8.1 million (which was true for 2014).

However, out of curiousity, I took a look to see what the 2015 data is, and sure enough, it was up to 8.4 million last year.

Here's a table showing, state by state, how many children were enrolled in the CHIP program last year (as well as the number in Medicaid, which, surprisingly, is actually more than 4x higher). In fact, well over half of all Medicaid enrollees are children.

NOTE: "Ever Enrolled" is confusing; it makes it sound like this is cumulative since the 1990's. It actually means "ever enrolled during that year", since there's a lot of churn with children moving into or out of the program as their family situation changes over time:

(Note: I've had to re-work some of this entry thanks to clarifications from Adam Cancryn about the RBC rule; too many little edits to document each one).

Last week I posted about the latest ugly Co-Op meltdown, this time Land of Lincoln Health (LoL) of Illinois.

As pointed out in my follow-up entry, given the precarious financial state LoL was already in last year, it made little sense that they only asked for fairly nominal rate hikes:

Now, since LoL went belly-up mid-year regardless, obviously even those massive rate hikes weren't enough to save them, so the question is, what would have happened if LoL had gotten their nominal increases as requested?

The most recent ACA/healthcare news out of Illinois was the ugly announcement that Land of Lincoln Health is the latest ACA-created Co-Op to go belly-up, leaving 49,000 people (39,000 on individual plans and 10,000 in the small group market) having to scramble to find new coverage in the middle of the year. This was on top of recent news that UnitedHealthcare is pulling out of dozens of states including Illinois (Humana is also dropping out of a bunch of states, but I don't think Illinois is among them).

Well, nature (and the market) abhors a vacuum, so guess what?

One of the nation's largest health insurance companies plans to enter the Obamacare marketplace in the Chicago area for the first time, bringing new competition as other insurers exit or go out of business.

My posts have been pretty light of late; between being on vacation, a big work backlog when I got back, and getting wrapped up in the RNC and DNC craziness, I've been a bit off-track. I'm hoping to catch up a bit over the next week or so.

As of 6/12, MNsure had 95,637 QHP selections, so this is an additional 1,286, or 34/day over the past 38 days. This is down substantially from the June report, when it averaged a whopping 179/day.

For the entire off-season period, MNsure has added 11,533 QHP selections, or an average of 68 per day. Extrapolated out nationally, that would be about 10,300 per day nationally, although in prior years off-season SEPs have averaged between 7,000 - 9,000 per day.