Oregon is the 5th state to post their initial 2018 rate filings. Last year their weighted average increase was roughly 26.5% across 10 individual market carriers. This year I only see 8 carriers offering policies on the indy market, but the two missing are "Trillium" and "ZOOM", neither of which had more than a handful of enrollees to begin with.

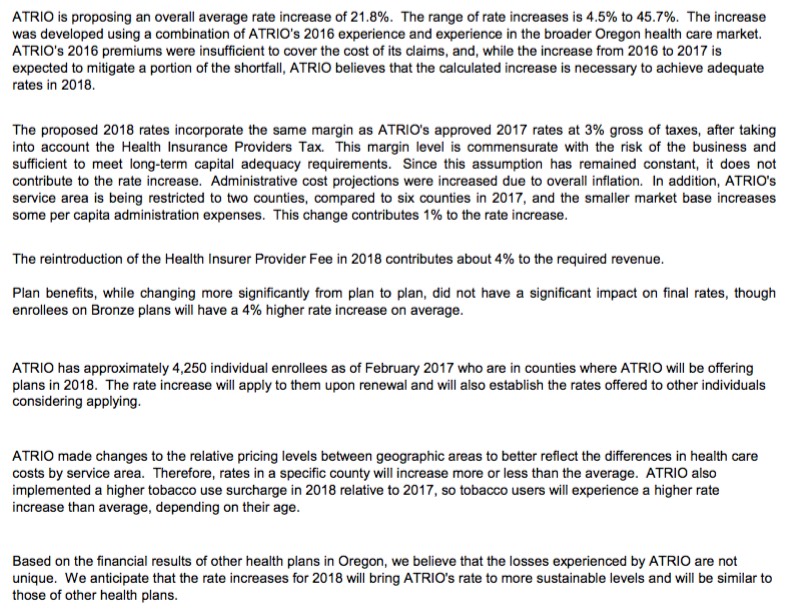

As you can see, ATRIO Health Plans was refreshingly clear in their rate justification letter, not only listing the key numbers (covered lives, average increase) but the reasons for it: 4% due to the reinstatement of the ACA's carrier tax; 1% due to them choosing to shrink their own coverage area from 6 counties to just 2; an increase for smokers., etc. They list 4,250 people being impacted by the increase; I don't know the population of the other 4 counties they're pulling out of, but assuming they're roughly equal, around 8,000 current enrollees will have to shop around this fall.

Regular readers may be a bit confused here, as Oregon's insurance dept. had already approved 2017 rates back in early August, for a statewide average of around 23.8%.

But when four carriers (Atrio, BridgeSpan, Providence, and — off-exchange — Regence) agreed in August to cover a broader service area than they had originally intended for 2017, state regulators also allowed them to further increase their premiums due to the increased risk they would be shouldering. Final approved average rate increases for Oregon’s exchange carriers are as follows:

Atrio Health Plans: 29 percent (up from the originally-approved 20.8 percent).

BridgeSpan: 23 percent (up from the originally-approved 18.9 percent).

Kaiser Permanente: 14.5 percent (range is from 10.9 to 22 percent).

Oy vey iz mir. Last fall, half of the two dozen Co-Ops created by the ACA were wiped out, falling like dominos over about a two month period, for a variety of reasons including the Risk Corridor Massacre. The other half managed to survive The Purge, many of them just barely doing so.

This year, it looks very much like the Risk Adjustment debacle has decided to try and finish off the job.

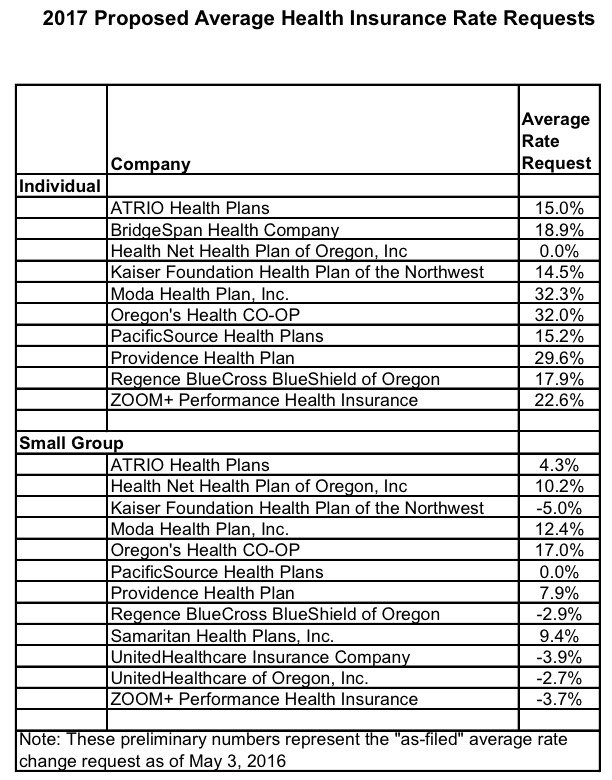

Oregon was the second state to publicly announce the rate changes their carriers are requesting for the 2017 individual and small group markets. The overall weighted average request on the individual market side came in at a requested 27.5% increase, while the small group market requests had an average increase of just 1% overall (I didn't weight the small group enrollment numbers at the time, but have done so below).

A few weeks ago, I got a heads up that Virginia was the first state out of the gate with their 2017 Rate Request filings. There were some confusing numbers which took awhile to sort out, but once the dust settled, the overall weighted average rate hike requests for Virginia's entire ACA-compliant individual market came in at around 17.9%.

Some states make it next to impossible to track down this info. Others hand it to you on a silver plate. And then there are states like Oregon, who provide the average rate hike requests in a simple, easy format, but don't necessarily include the market share of those companies, making it difficult to compile a weighted average:

Back in January I noted that Moda Health Plans, which had plenty of self-inflicted wounds in addition to being kneecapped by the Risk Corridor Massacre, was dropping out of the Oregon exchange and likely the Alaska exchange as well, so today's news isn't a big surprise.

Even so, this is definitely a major problem for the Alaska individual market, which was already extremely expensive prior to the ACA and which now only has a single insurance carrier participating (h/t to Louise Norris):

The individual market in Alaska has just two carriers in 2016: Moda and Premera. Both have struggled with significant losses under the ACA, and Moda nearly exited the Alaska market altogether in late January (more details below).

Oregon is considering proposals by four companies to provide a new software platform for the state’s health insurance marketplace.

The state uses the federal insurance exchange, http://www.Healthcare.gov, and state officials began to explore other options after the federal government decided to begin charging insurance companies a fee to use the exchange in Oregon.

Oregon has used the federal platform since its own insurance portal, Cover Oregon, failed to launch in 2013. The state and technology company Oracle, which built the Cover Oregon system, are still engaged in a legal battle over who is to blame for the problems.

Remember how the Risk Corridor program was put in place specifically to help guide insurance carriers through the rocky, turbulent, confusing waters of the early years of the ACA exchanges by mitigating massive premium rate miscalculations the first few by having carriers which did better than expected chip into a kitty to be passed out to those which missed the target for the first 3 years?

Remember how the carriers which lost money the first year were really, really counting on those Risk Corridor funds to be there to help cushion the blow?

Remember how as a result, when it came time to start doling out the RC funds to the carriers which had a crappy first year, there were only 12 cents on the dollar sitting in the cupboard?

As anyone who's been following the ACA exchange saga over the past few years knows, the original idea was that all 50 states (+DC) would establish their own, individual healthcare exchange, including their own website/technology platform for enrolling residents in private policies (QHPs), Medicaid (supplementing or replacing whatever existing Medicaid system they already had) and small business policies (the ACA's SHOP program). In addition, each state exchange would also have their own board of directors, marketing department, support call center, fee structure for covering the cost of operations and so on.

If things had worked out that way, there would have been 51 different websites where people would enroll in ACA policies, each one independently branded.

That's 2 in one day, the 8th to fold to date and the 4th one which can be specifically connected the Risk Corridor Disaster:

Health Republic Insurance Not Offering Plans in 2016

Lake Oswego, Ore. (Oct. 16, 2015) –Health Republic Insurance, a non-profit health insurance carrier, announced today that it will not offer small group or individual plans on or off exchange in 2016. All current Health Republic individual and small group policies remain in full effect through the end of 2015. Members can continue to see plan providers and claims will be paid under plan terms.

The federal government recently announced it would pay insurance companies only 12.6% of their risk corridor receivable for the 2014 plan year and has created industry-wide concern about when, or if the 2015 risk corridor would be paid.