I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

As I noted a couple of weeks ago, I've relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

The American Rescue Plan does plenty to make private ACA-compliant health insurance dramatically more affordable for everyone earning more than 100% of the Federal Poverty Level. For those below 100% FPL, however, it takes an indirect approach. As I wrote a few weeks ago:

One possible "solution" would have been to simply remove the lower-bound income cut-off point for ACA exchange subsidy eligibility (that is, to lower the threshold from 100% FPL to 0%)...However, this would create two new problems: First, Medicaid is far more comprehensive than nearly all ACA plans...Secondly, if the lower-end subsidy cut-off were removed, it's almost certain that quite a few states which have already expanded the program would reverse themselves and allow Medicaid expansion to expire, in order to save the 10% portion of the cost that they have to pay.

The Alabama Department of Insurance (ALDOI) has approved the final 2021 premium rates for the Affordable Care Act Individual Market in Alabama. The rates will be effective on January 1, 2021. The two carriers in the Alabama individual market are Blue Cross Blue Shield of Alabama (BCBS) and Bright Health Insurance Company of Alabama (BHIC). In general, rates for BCBS increased five percent and rates for BHIC increased 22 percent. The actual rates and the supporting material may be found by clicking on the links below.

Unfortunately, the linked documents are still redacted and thus don't include the enrollment numbers for Bright (and this press release says nothing about the small group market), but as far as I can tell this doesn't change the averages of either market much from the preliminary filings. Assuming Bright still only has a tiny part of the market, even its 22% average increase doesn't move the needle much.

The good news is that both of last years' individual market carriers (Blue Cross Blue Shield and Bright Healthcare) do have listings for 2021 in the SERFF database.

The bad news is that those listings don't include actual rate filings, just some other forms.

The good news is that rate filings for every state appear to be available at RateReview.HealthCare.Gov this week.

The bad news is that the filings at RR.HC.gov appear to be incomplete so far; BCBS is listed but Bright isn't (and since I do have other forms for Bright being listed in 2021, I'm pretty sure it's not because they're pulling out of the Alabama market).

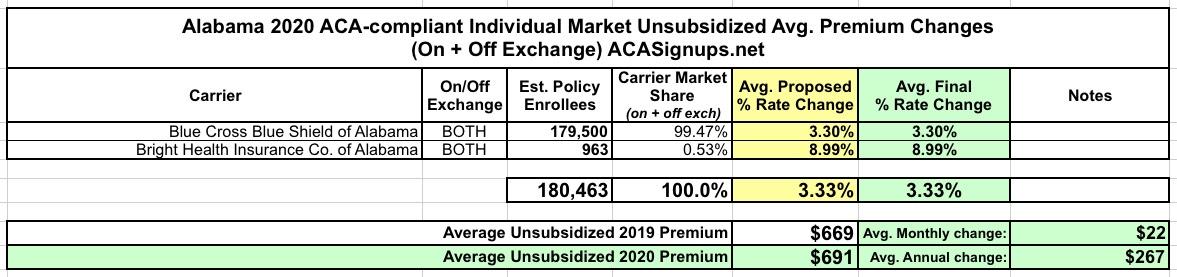

When I first ran the preliminary 2020 ACA premium rate filing requests for Alabama in August, I came up with a weighted average increase of 3.9%.

CMS has just posted the final, approved rates for Alabama's 2 carriers (Blue Cross Blue Shield and Bright Health). Both carriers had their requested rate hikes approved without any changes, but the final weighted average for unsubsidized enrollees still dropped a bit to 3.3%...because I had the wrong market share ratios. It looks like Bright has an even smaller share of the market than I thought (less than 1%), bringing the weighted average down a bit.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

Alabama only has two carriers offering Individual Market policies. Unfortunately, the rate filing forms are redacted in some states, so I'm having to patch together bits & pieces of data to try and estimate the weighted average rate changes. In the case of Alabama, the filing for Blue Cross Blue Shield lists 179,500 total individual market enrollees in 2018, but there's no data for 2019...while the filing for Bright Health Insurance (a relative newcomer to the market) doesn't list any enrollment data at all.

I'm assuming that BCBSAL holds a solid 90% of the market and that their total enrollment is around the same year over year. If so, that would give Bright around 20.5K enrollees and make the total Alabama Individual Market around an even 200,000 people. Again, assuming all of this is accurate, that means a weighted average increase of 3.9%, which in turn means unsubsidized enrollees are looking at average premium increases of around $26/month or $312 for the year.

NOTE: This has been corrected from an earlier version.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

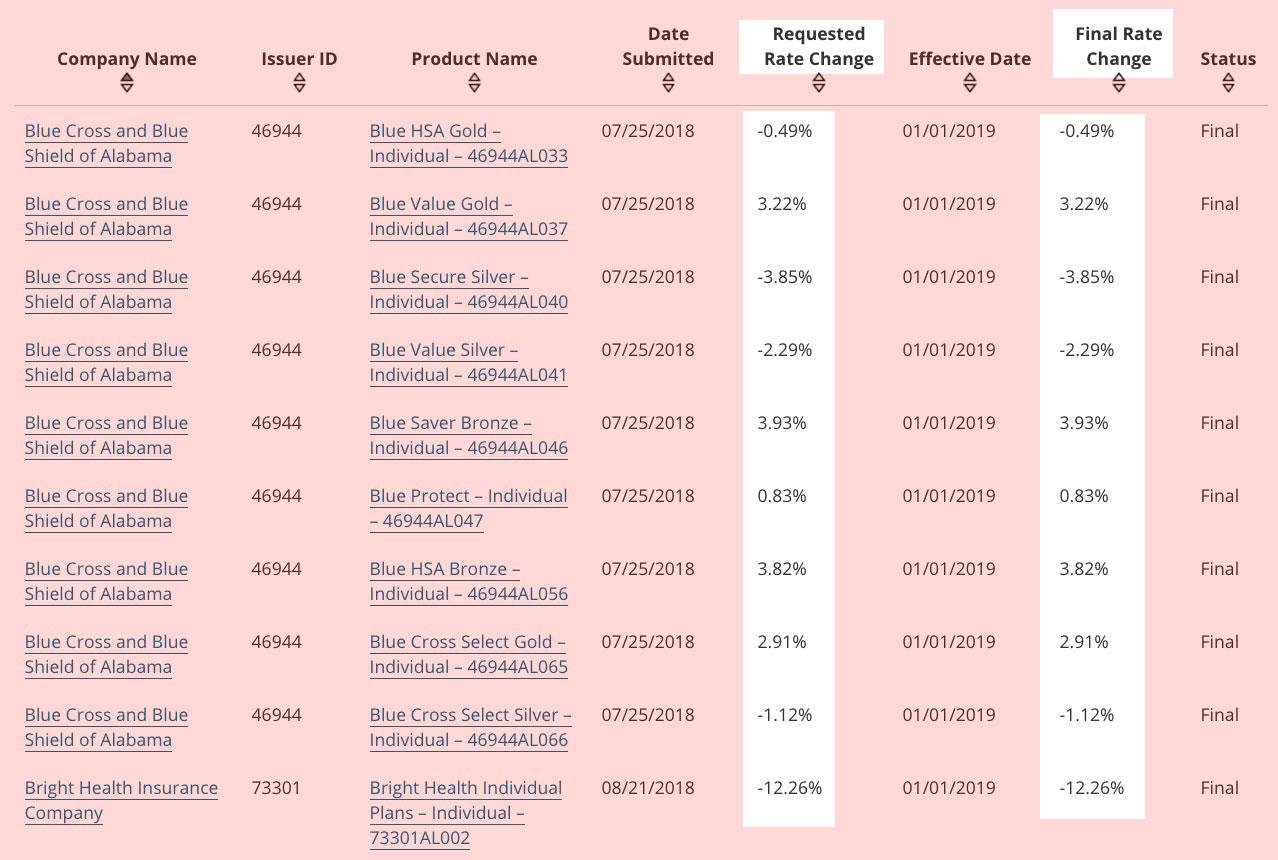

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these. Making things even easier (although not necessarily better from an enrollee perspective), in three states the approved rates are exactly what the requested rates were for every carrier: Alabama, Mississippi and Utah: