California’s Open Enrollment for Individuals Ends Jan. 15; Consumers Have One Week to Sign Up for Health Care Coverage

Consumers have through Jan. 15 to sign up and select a plan through Covered California or directly with health plans for coverage that will begin on Feb. 1.

The final week of open enrollment comes on the heels of Gov. Newsom’s announcing sweeping proposals, including a new requirement for having coverage and expanded subsidies.

While open enrollment ended for much of the nation in December, California’s final deadline is about two weeks earlier than it was in previous years, when open enrollment ran through the end of the month.

More than 238,000 consumers had selected a plan through Dec. 31.

Gov. Gavin Newson announced sweeping proposals to tackle the state’s healthcare needs shortly after taking office on Monday, outlining a dramatic Medi-Cal expansion that would cover young undocumented adults, a requirement that all consumers in the state carry health insurance and increased subsidies for middle-class families to help those who need it.

...Newsom campaigned on a universal healthcare platform and has said the issue would be among his top priorities. His announcement on Monday stopped short of the single-payer system demanded by activists that would cover all residents’ healthcare costs, but was characterized as the first step down that path.

According to the article, Newsom, who just took office a few hours ago, already plans on rolling out his proposed state budget on Thursday, which is expected to include, among other things:

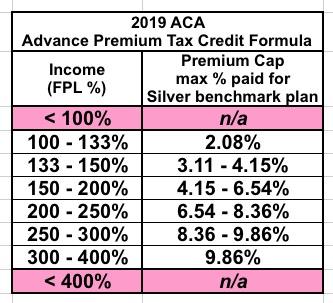

For years now, I (and many other healthcare wonks) have been arguing that one of the most important fixes/improvements that the ACA needs regardless of the Next Big Thing® is to #KillTheCliff...that is, to eliminate the infamous "subsidy cliff" which hits those who earn just over the 400% Federal Poverty Level income cap for Advance Premium Tax Credit (APTC) assistance.

Once again: Under the ACA, if you earn between 100-400% FPL (between $12,140 and $48,560 for a single person), you're eligible for APTC assistance on a sliding scale. The formula is based on the premium for the Silver "benchmark" plan available in your area, which averages around $611/month in 2019.

Here's how the formula works under the current ACA wording:

Now that the Democrats have officially retaken control of the U.S. House of Representatives, everyone's expecting them to try and save and improve the ACA. I stress "try", of course, because without the Senate, it's unlikely that any bill to protect or improve the law will get passed...and even if it did somehow, the odds are high that it would then be vetoed by Donald Trump (or Mike Pence, in the unlikely-but-still-conceivable event that Trump is removed from office before January 20, 2021).

HOWEVER...they can certainly at least try. With a likely 235:200 advantage in the House and a caucus which is far more progressive on healthcare issues than it was a decade ago, the Dems shouldn't have too much trouble passing a fairly robust healthcare reform package even knowing that it's unlikely to go anywhere in the Senate. The question is how robust?

UPDATE 3:50pm: OK, it sounds like you can completely disregard all the Medicaid-related stuff below; apparently there was a communication error. I've confirmed with the Whitmer campaign that the proposed reinsurance plan would not be tied in with Michigan's ACA Medicaid expansion program at all, nor would it have any impact on the Medicaid eligigibility threshold, which means this would indeed be a standard ACA individual market reinsurance program after all...which is what I assumed in the first place, and which would be perfectly fine!

BREAKING: Governor @JerryBrownGov today signed several #Care4AllCA bills that protects patients and places greater accountability on health insurers now on Gov's desk:#SB910 & #SB1375 to ban/limit "junk" insurance;#AB2499 on MLR; and#AB2472 on a public option study.

Back in April, I started an ambitious project which set out to track every legislative or regulatory measure taken by every state to counter, cancel out or mitigate sabotage of the Affordable Care Act by the Trump Administration and Congressional Republicans. It resulted in this color-coded spreadsheet, which lists dozens of bills, proposals, amendments and so on at various stages of completion.

The bad news is that project has proven to be too large for me to keep up with--there's simply too many bills, too many stages and too much other stuff going on for me to keep track of it all.

Note: Most of this isn't limited to Michigan...nearly all of the items listed here could/should be applied in other states as well.

Dear Democratic nominees for Michigan State House and State Senate:

Hi there, and congratulations on your primary victory!

If you're familiar with me and this site, you probably know three things about me:

1. I strongly support achieving Universal Healthcare coverage, and I'd ideally prefer to utilize some sort of Single Payer system as the payment mechanism to do so.

2. However, even with the recent strengthening in support, I remain skeptical that a SP/Medicare-for-All type of law is feasible yet, for a number of reasons I've talked about before but won't go into right now.

3. Having said that, during the interim between today and whatever the Next Big Thing is in healthcare (whether it's Medicare for All, Medicare X, Medicare Extra (my personal favorite), Medicaid Buy-In, Medicare Part E, CHIPA, USEAHIA, Healthy America or some other federal program), I strongly believe that it is vitally important to protect, repair and strengthen the Affordable Care Act even if it ends up being replaced by something else in the near future.

Gov. David Ige signed a new law on Thursday that ensures certain benefits under the Affordable Care Act will be preserved under Hawaii law.

Senate Bill 2340 retains several of the measures introduced in the Obama-era legislation, also known as Obamacare, including a clause that allows Hawaii adults up to 26 years-old to continue receiving health insurance under their parents.

The law also prohibits health insurance organizations from excluding coverage to those with preexisting conditions, or using an individual's gender to determine premiums or contributions to health insurance plans.

State’s Market Stability Workgroup Recommends Immediate Action to Protect Rhode Islanders from Federal Threats to Health Insurance Access and Affordability

Posted on June 27, 2018 | By HealthSource RI

EAST PROVIDENCE, R.I. (June 27, 2018) – Rhode Island must act “without delay” to protect consumers from rising health coverage costs brought on by federal policy changes according to a report issued to Governor Raimondo by the state’s Market Stability Workgroup.

“People representing a wide variety of viewpoints engaged in lively discussions over the course of 8 weeks,” said Workgroup co-chair Bill Wray, Chief Risk Officer at the Washington Trust. “The fruits of those discussions are in this report. All of us – consumer advocates, business groups, health insurers and providers – were able to broadly agree on how best to protect Rhode Island’s insurance markets.”