UPDATE 3/26/19:I'm watching the actual press conference right now. I just wanted to note that there will likely be a few changes/tweaks in the bill/bills introduced today vs. last year's H.R.5155, but it sounds like it'll be about 95% the same. More details this evening.

Back in early January, in an MSNBC interview with Joy Reid, House Speaker Nancy Pelosi noted that she did indeed intend on moving on legislation to, at the very least, raise or remove the ACA subsidy income threshold to allow financial assistance to be available to more people:

The new Speaker of the U.S. House of Representatives said this weekend she wants changes in the income threshold to allow more Americans to gain subsidies so they can buy individual coverage known as Obamacare. Helping more people get subsides are among the "couple of things" she would like to do to improve the ACA and expand health coverage to more Americans, Pelosi, a California Democrat, told MSNBC Friday night.

Connecticut lawmakers are joining other states that have unveiled proposals to expand government-run health coverage, with plans to extend state health benefits to small businesses and nonprofits, and to explore a public option for individuals.

Under two measures announced Thursday, officials would open the state health plan to nonprofits and small companies – those with 50 or fewer employees – and form an advisory council to guide the development of a public option. The legislation would allow the state to create a program, dubbed “ConnectHealth,” that offers low-cost coverage to people who don’t have employer-sponsored insurance.

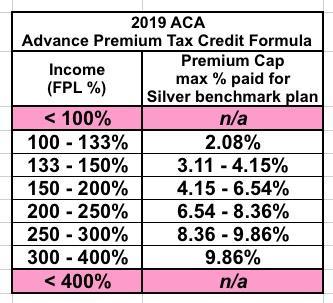

Regular readers know that I've been calling for Congress to #KillTheCliff for years:

Once again: Under the ACA, if you earn between 100-400% FPL (between $12,140 and $48,560 for a single person), you're eligible for APTC assistance on a sliding scale. The formula is based on the premium for the Silver "benchmark" plan available in your area, which averages around $611/month in 2019.

Here's how the formula works under the current ACA wording:

...Here's the problem: If they earn exactly 400% FPL ($48,560), they'll also only have to pay 9.86% ($4,802), receiving $2,530 in subsidies for the year....

I don't know what the status is of H.R. 5155 (the House Democrats catch-all "ACA 2.0" bill which I've been pushing for awhile now), but it looks like individual elements of it are also in the works as standalone bills:

Date: Wednesday, March 6, 2019 - 10:00am

Location: 2123 Rayburn House Office Building

Subcommittees: Health (116th Congress)

The Health Subcommittee with hold a legislative hearing on Wednesday, March 6, at 10 am in the John D. Dingell Room, 2123 Rayburn House Office Building. The hearing is entitled, “Strengthening Our Health Care System: Legislation to Lower Consumer Costs and Expand Access.” The bills to be the subject of the legislative hearing are as follows.

Over at Balloon Juice, David Anderson notes that the Blue Cross & Blue Shield Association has released their own "ACA 2.0" proposal...and many elements line up pretty closely to my own vision of what ACA 2.0 should look like as well as both the House (H.R. 5155) and Senate (S.2582) Dem versions. Here's Anderson's summary of the BCBSA proposal:

Younger adults pay a lower percentage of their income (at a given level) for the benchmark plan

Older adults are held harmless

All individuals, regardless of income, are eligible for subsidy assistance

CSRs appropriated

CSRs expanded

Full advertising and outreach funded

Health insurance premium tax suspended

...It looks like the insurers are trying to lay markers for where they want to see things in 2021 or 2022. They are looking at a fix and expansion of the current paradigm instead of a complete replacement of the system.

I visited DC last month for the Families USA healthcare conference. While I was there, I managed to arrange to meet with staffers for four U.S. Senators and two House members (in fact, the House members themselves stopped by to talk for awhile as well. None of the Senators did, but they were a bit busy dealing with Donald Trump's idiotic temper tantrum government shutdown at the time).

In my meetings, we discussed a variety of healthcare policy-related issues, but the two most important ones I focused on were:

Last year I briefly attempted to keep track off the dozens of various state-based "ACA 2.0" protection/improvement bills flying around various state legislatures. I eventually abandoned this project since it became too difficult to keep up with, but I'm still reporting case studies as they come to my attention...and Louise Norris has just alerted me to some pretty big changes going into effect in Colorado this April.

First up: Short-term plans are being heavily neutered. In addition to being limited to 6 months per year (which is still longer than the Obama Administration's 3-month cut-off)...

Short-term plans will have to charge older adults no more than three times as much as they charge younger adults. Short-term plans are generally not available after a person is 64, but a quick check of plans currently available in Colorado show that some insurers are charging a 64-year-old up to seven times as much as a 21-year-old. That will have to stop as of April.

A couple of weeks ago, I noted that Speaker of the House Nancy Pelosi, in an interview airing on MSNBC, stated that two of the major pieces of healthcare legislation she intends on pushing through this session are raising the ACA's tax credit eligibility threshold and "replacing" the now-repealed ACA individual mandate (i was never sure whether "replacing" meant reinstating it or actually replacing it with some other enrollment incentive).

I realize that the odds of any useful healthcare legislation managing to pass the Senate and become law under the Trump Administration is pretty slim, but hey, it's still good news, right!

State government plays a critical role in today’s health care system. Every policy decision we make has an impact on the individuals, children and families who need care. The Governor’s FY20 budget proposal builds on this momentum, preserving vital ACA protections that promote market stability and help to keep uninsured rates low. There are no eligibility cuts or broad-based benefit impacts proposed.

Back in April 2017, I compiled a 20-itme "ACA 2.0 wish list" which I titled "If I Ran the Zoo", which gained some amount of attention from the healthcare policy wonk community. To be clear, I wasn't the first one to come up with most of these ideas; it was mainly just pulling together a bunch of proposals to protect, repair and strengthen the ACA from various sources into a single, comprehensive collection.

Since then, several bills have been introduced by Democrats in either the House or the Senate which addressed one or more of these recommendations, and last spring there were two bills (one in the House, one in the Senate) which tackled over a half-dozen of them in a package deal. None of these bills have gone anywhere since then, of course; with the Dems having retaken the House, it's a lot more viable that one or more will do so this year, although getting any of them through the Senate is obviously a much tougher climb.

However, some of the items on the list haven't even made it that far, including #5 on my list: