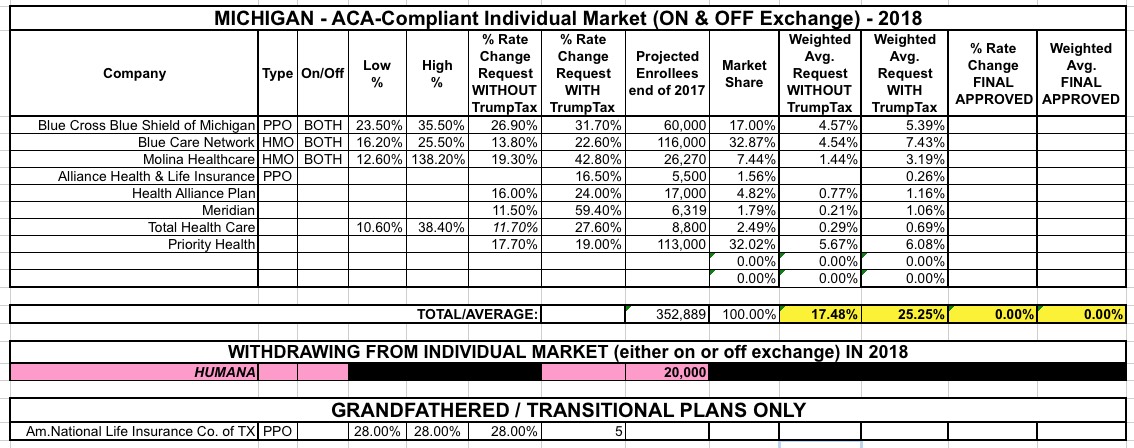

Michiganders purchasing health insurance through the federal marketplace will see an average rate increase of 27.6 percent in 2018, the Michigan Department of Insurance and Financial Services announced Friday.

One reason for the big increase: Uncertainty over whether President Trump will continue to fund Cost-Sharing Reduction payments, which subsidize plans for low- and moderate-income households.

Idaho is a bit of an odd duck when it comes to the ACA. On the one hand, they're the only state completely controlled by Republicans to set up their own ACA exchange (Kentucky's much-lauded "kynect" exchange was created by Democratic Governor Steve Beshear by executive order...and was then promptly scrapped the moment that incoming GOP Governor Matt Bevin took office). On the other hand, they're also the only state with their own exchange not to expand Medicaid. (As an aside, ID is also the only state to start out on the federal exchange the first year before breaking out onto their own exchange website).

We Can Talk About is a fun, informative, engaging weekly podcast dedicating to taking back the narrative in American politics. For too long we've let the other side set the terms of the conversation and it's about time we promote our own nurturant values.

We spent an hour or so discussing the CSR reimbursement brouhaha, the ACA in general, and especially my ongoing battle to get people to understand the distinction between phrases like "single payer", "Medicare for All", "universal care" and so on in an episode entitled "The Road to Single-Payer Healthcare". Check it out!

Anthem on Wednesday continued reducing its Obamacare business, as the big insurer said it will cut in half the number of counties in Kentucky where it sells individual health plans next year.

Virginia was the very first state whose 2018 rate filings I analyzed, way back in early May. At the time, the initial filings amounted to 9 carriers on the individual market with an average rate increase request of around 30%. At the time I hadn't started distinguishing between "with CSR payments" or "without CSR payments", so I don't really know which scenario that 30% reflected; it was probably a mix of both depending on the carrier. 61,000 Aetna enrollees would have to shop around for a new carrier since they had previously announced they were pulling out of the individual market.

Back in January, I was pleasantly surprised to be included (sort of) in an actual comic book (OK, a "graphic novel") drawn/written by a skilled artist named Michael Goodwin. He did an excellent job of explaining the basics of how the ACA was supposed to work, some of the problems it's had, what the GOP was trying to push as a replacement, why that replacement sucked so badly and so forth. I was honored to learn that he had utilized some of my own data in putting together the project.

Well, Goodwin is back with a follow-up. This one isn't as long, and it focuses mainly on the sabotage efforts being attempted by Donald Trump and the GOP to undermine the ACA as much as possible. Once again, he's included some of my info/analysis as part of the comic, which I'm greatly flattered by. Here's a sample; click through for the whole thing:

Up at the top of the site is a big yellow button leading directly to the ongoing 2018 Rate Hike project. Let's face it, though: It's an awful lot of updates to scroll through. In addition, now that we're past the (extended) rate filing deadline, I've been able to make a lot of updates over the past few days (shoutout to Louise Norris, who did much of the grunt work on these).

As of today (September 6th), I now have average requested 2018 rate changes for the individual market across all 50 states + DC, and have made updates/corrections to several of these.

More importantly, I also now have approved 2018 rate changes for 6 states. They only represent around 9% of the population, though, so I wouldn't focus very much on the "national average" for the approved states yet; that will jump around a lot as more states are added to the mix, and likely won't start to settle in until at least half the states are included.

Having said that, here's what things look like as of today:

(sigh) Colorado's state insurance division just released their approved 2018 rate increases (busy day!), and the situation appears to be similar to Maine: The average requested rates which I thought already assumed no CSR reimbursements appear to have assumed CSRs would be paid after all:

Division of Insurance approves health insurance premiums for 2018

Commissioner: Measures to stablize market for 2018 must happen by Sept. 30

DENVER (Sept. 6, 2017) – The Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA), has approved the individual and small group health insurance plans for 2018. Average premium changes within each market - individual and small group - as well as the average change for each insurance company are listed below.

The state of Maine's insurance regulatory agency has announced the approved 2018 individual market rate hikes for the three carriers operating in the state. Louise Norris beat me to the punch:

Regulators in Maine published rate proposals for the three Maine exchange insurers in June, and finalized the rates in early September. Insurers proposed two sets of rates: one that assumes cost-sharing reduction (CSR) funding will continue, and another that assumes the federal government will not fund CSRs in 2018.

The Maine Bureau of Insurance initially rejected all three insurers’ rate proposals on August 10, and asked them to submit new rates. The revised rate filings were then approved on September 1. These average approved rate increases all assume that CSR funding will continue in 2018:

Vermont was one of the first states I analyzed back in the late spring; obvoiusly a lot has changed since then, so I updated/revised my analysis of their requested rate hikes for 2018 a couple of weeks ago, with requested average increases of 11.9% if CSR payments are made or 21.6% if they aren't.

Yesterday, Louise Norris gave me a heads up that the Vermont regulators have issued their approved rate increases for the two carriers operating on the individual and small group markets in the tiny state. This makes Vermont the 4th state to announce their approved rates for next year, joining Oregon, Maryland and New York.