I've written not one, not two, but three different blog entries in the past 24 hours about Bernie Sanders' just-announced "Medicare for All" proposal...but the reality is, I shouldn't have. Frankly, while it's a discussion/debate that we do need to have, making a big thing about it right this moment is, the more I think about it, terrible timing, because the Affordable Care Act is still in being attacked and at risk in several ways:

FIRST: The CSR issue still hasn't been resolved, although at this point it's extremely unlikely that Patty Murray and Lamar Alexander are going to pull a CSR/reinsurance rabbit out of their hats after all. Last week things looked somewhat promising, but this week it appears to have gone off the rails again...and with just 17 days left in the fiscal year (and, I believe, only 14 days before the contracts have to be signed by carriers for 2018 exchange participation), there's almost no time left to get even a minor stabilization bill pushed through.

SECOND: On a related note, Bill "so much for the Jimmy Kimmel test!" Cassidy and Lindsey Graham are still trying to cram through their pile-of-garbage Hal Mary Trumpcare bill, which is at least as bad as the GOP's failed AHCA/BCRAP bills were earlier this year and even worse in some ways. Again, there's only 17 days left to pull it off, but remember what happened with AHCA last spring...anything's possible. Here's a summary of the impact of the Cassidy-Graham bill via Andy Slavitt and the Centers for Budget & Policy:

OK, here it is. I've linked to a PDF with the full legislative text at the bottom of this blog entry; here's the summary version, with some notes:

TITLE I—ESTABLISHMENT OF THE UNIVERSAL MEDICARE PROGRAM

Establishes a Universal Medicare Program for every resident of the United States, including the District of Columbia and the territories. Guarantees patients the freedom to choose their health care provider. Provides for the issuance of Universal Medicare cards that all residents may use to get the health care they need upon enrollment. Prohibits discrimination against anyone seeking benefits under this act.

OK, so it apparently would cover undocumented immigrants, and every doctor/hospital/clinic/etc. would be required to participate, with anyone in the country being covered by any healthcare provider nationally.

The official announcement is scheduled for Wednesday, presumably with much hoopla accompanying it (and a dozen or so Democratic Senators co-sponsoring it, many of whom are considered likely 2020 POTUS candidate prospects). Over at the Washington Post, Dave Weigel has a sneak peak. I'll wait until I've had a chance to read through the actual text of the bill itself to write up a full response/analysis, so I'll just post a few key excerpts from Weigel's piece for now:

Sanders’s bill, the Medicare for All Act of 2017, has no chance of passage in a Republican-run Congress. But after months of behind-the-scenes meetings and a public pressure campaign, the bill is already backed by most of the senators seen as likely 2020 Democratic candidates — if not by most senators facing tough reelection battles in 2018.

For the past year and a half, of all the proxy battles between "Team Hillary" and "Team Bernie" on the left side of the aisle, no issue has been more repsentative of both how passionate people are or how much each "side" misunderstands the other than the future of the American healthcare system.

"Team Bernie", in essence, consisted of progressives (and Democrats) who believe that while the ACA may have improved things to some degree in some ways, it not only isn't enough long-term, it isn't nearly enough short-term either; the next step (and for many, the only acceptable next step) must be moving the entire U.S. population over to a universal Medicare-style Single Payer system, with everyone in the country being covered through a single, comprehensive healthcare program funded entirely (or nearly entirely) by taxes.

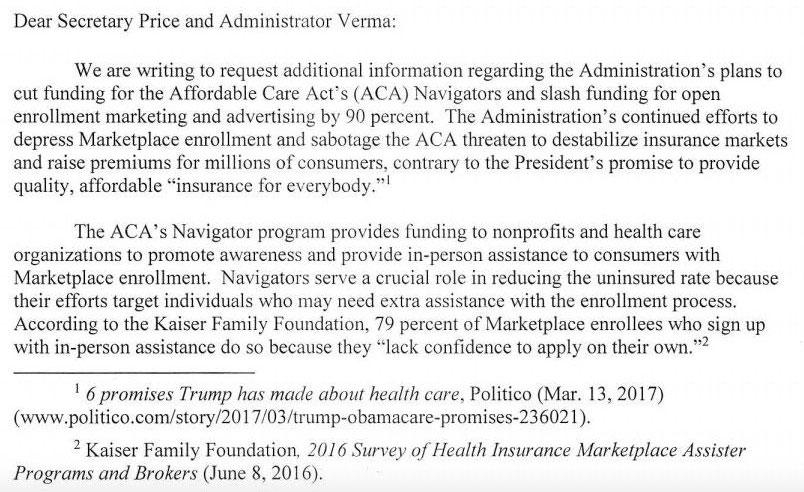

It appears that a formal letter was sent to HHS Secretary Tom Price and CMS Administrator Seema Verma from the Energy & Commerce Committee of the House of Representatives...it's 6 pages long, and unfortunately the text isn't selectable, so I had to embed the pages as images. I'm happy to report that I contributed to their inquiry.

If you look at the top of the website today, you'll notice a couple of new graphics, both relating to the Indivisible ACA Signup Project.

The short version is this:

Donald Trump is cutting ACA outreach, so we've started an Indivisible-based, state-by-state sign-up project group to counter the sabotage.

All you need to do (should you agree) is use social media to update people (on your advocacy and/or personal pages) in your state on key issues and dates/deadlines for sign-ups.

That's pretty much the whole thing in a nutshell, at least so far. It's a closed Facebook Group which you need to request permission to join, but they obviously want the materials to be disseminated as widely as possible (that's kind of the whole point!), so I've agreed to set up a permanent, public link for folks to access them.

...and believe me, it wasn't on purpose; I've simply been swamped the past couple of weeks with other stuff, and somehow I just never got around to writing anything up about it.

I should have, though. Everyone thinks the existential threat to the ACA was over back on July 28th, and now it's simply a matter of "stabilizing the market" and "stopping Trump from sabotaging Open Enrollment". For the most part this is true, but for whatever reason, Louisiana GOP Senator Bill Cassidy and South Carolina GOP Senator Lindsey Graham simply won't let it go already, and are insisting on trying one final, desperate Hail Mary play to squeeze through an ACA repeal/Trumpcare bill as the final seconds run out on the 2017 Fiscal Year (which ends September 30th).

Since I'm so late to the party on this and there's so little time to stop it, instead of my own explainer I'm going to simply crib a bit from former CMS head Andy Slavitt's USA Today column in which he gives the lowdown:

A week ago, Vox's Sarah Kliff reported that the Trump Administration was slashing the 2018 Open Enrollment Period advertising budget by 90% and the navigator/outreach grant budget by nearly 40%. As I noted at the time, the potential negative impact of these moves on enrollment numbers this fall--coming on top of the period being slashed in half, the CSR reimbursement and mandate enforcement sabotage efforts of the Trump/Price HHS Dept. and the general confusion and uncertainty being felt by the GOP spending the past 7 months desperately attempting to repeal the ACA altogether could be significant. In states utilizing the federal exchange (HealthCare.Gov), 2017 enrollment was running neck & neck with 2016 right up until the critical final week...which played out under the Trump Administration, which killed off the final ad/marketing blitz.

Result? A 5.3% total enrollment drop (or 4.7% if you don't include Louisiana, which expanded Medicaid halfway through the year) via HC.gov, while the 12 state-based exchanges--which run their own marketing/advertising budgets--saw a 1.8% increase in total enrollment year over year.

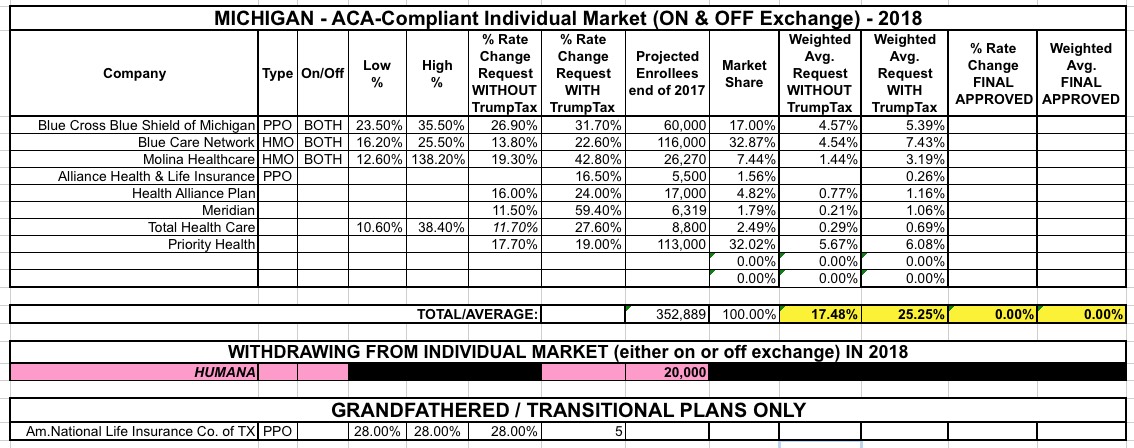

Michiganders purchasing health insurance through the federal marketplace will see an average rate increase of 27.6 percent in 2018, the Michigan Department of Insurance and Financial Services announced Friday.

One reason for the big increase: Uncertainty over whether President Trump will continue to fund Cost-Sharing Reduction payments, which subsidize plans for low- and moderate-income households.

Idaho is a bit of an odd duck when it comes to the ACA. On the one hand, they're the only state completely controlled by Republicans to set up their own ACA exchange (Kentucky's much-lauded "kynect" exchange was created by Democratic Governor Steve Beshear by executive order...and was then promptly scrapped the moment that incoming GOP Governor Matt Bevin took office). On the other hand, they're also the only state with their own exchange not to expand Medicaid. (As an aside, ID is also the only state to start out on the federal exchange the first year before breaking out onto their own exchange website).