On Get Covered Colorado Day, Connect for Health Colorado and state leaders urge customers to compare options and maintain health coverage in 2026.

Denver, Colo.– Today is Get Covered Colorado Day, a day of action designed to encourage as many Coloradans as possible to enroll in 2026 health insurance during Connect for Health Colorado's annual open enrollment period.

“Our message today is simple: we’re here to help every Coloradan get covered,” said Kevin Patterson, chief executive officer of Connect for Health Colorado, the state’s official health insurance marketplace. “Even with premium increases and the possible expiration of federal enhanced Premium Tax Credits, Coloradans are finding plans that fit their needs and their budgets – and they’re not doing it alone. Our experts are ready to guide customers every step of the way. We want Coloradans to know there’s no better time than now to shop, compare options and take advantage of the support we have available.”

There are 43 U.S. House districts where the Republican nominee won by 15 points or less. Of those, one (WA-04) doesn't really count since there were 2 Republicans running in the general election (Washington State has "jungle primaries"). Four others were won by Donald Trump by between 16 - 20 points (AZ-08, CO-04, TX-15 & WI-08).

That leaves 38 GOP-held House seats where the Republican won by 15 pts or less and where either Kamala Harris won, or Donald Trump also won by 15 points or less. The table below breaks these out with both margins, while also listing my estimate of how many residents of each district are enrolled in ACA coverage.

To: Plymouth Union Public Advocacy From: Tony Fabrizio & Bob Ward

Date: July 14, 2025

Re: Expiration of Premium Tax Credits Survey – Targeted Congressional Districts

Our survey of voters in the most competitive Congressional Districts shows Republicans have an opportunity to overcome a current generic ballot deficit and take the lead by extending the healthcare premium tax credits for those who purchase health insurance for themselves. Without Congressional action, the tax credit expires this year.

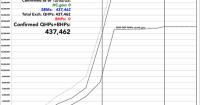

For 12 years now, one of the traditions of ACA Signups has been The Graph: A line graph tracking enrollment in ACA policies over the course of each Open Enrollment Period.

The original Graph from 2013-2014 looked quite different from more recent years, partly because I was attempting to track Medicaid/CHIP enrollment and other coverage categories at the same time, and partly because, frankly, I didn't really know what I was doing at the time.

Over the next few years I modified & improved both my methodology as well as the format, culminating in last year's 2025 Open Enrollment Period Graph, which featured the highest enrollment figures in the ACA's history: ~24.3 million Qualified Health Plan (QHP) enrollees, plus another ~1.8 million Basic Health Plan (BHP) enrollees in Minnesota, New York & Oregon specifically, for a grand total of just a hair over 26 million people.

For the 2026 Open Enrollment Period, however, actual hard enrollment data has been, shall we say, difficult to come by so far.

I don't know if this is new or not, but it turns out that Covered California--the largest state-based ACA exchange in the country--has an Open Enrollment Dashboard after all!

This means that in addition to two small states regularly reporting Open Enrollment data (Maine and New Mexico), the largest one is as well!

Here's what Covered CA is reporting as of November 29th:

New enrollments: 45,023

Active renewals: 365,879

Passive/Autorenewals: 1,412,526

Total: 1,823,428

As I've noted in both my Maine and New Mexico updates, while I include the passive/auto-renewal number for completeness sake, that number won't really be relevant until after the deadline for January 1st coverage passes (which is December 15th in most states, although not until 12/23 in MA & 12/31 in MD, NV, NJ, NM & RI).4,

via MNsure, Minnesota's ACA exchange (email only for now):

Minnesota residents affected by the end of Strategic Limited Partners coverage can enroll in new health insurance through MNsure

ST. PAUL, Minn.—MNsure is opening a limited special enrollment period (SEP) for Minnesota residents who purchased insurance through Strategic Limited Partners offsite of the MNsure website. The SEP follows enforcement action by the Minnesota Department of Commerce.

Commerce found that Strategic Limited Partners, an unlicensed company, sold unauthorized and deceptive health coverage to Minnesotans through misleading ads. Under a consent order, Strategic Limited Partners must cease operations by December 31, 2025, notify customers of its exit, repay outstanding claims, and pay a civil penalty.

To protect affected consumers, MNsure is offering this limited SEP:

While it appears that Congress will allow enhanced federal Premium Tax Credits to expire, New Mexico’s Health Care Affordability Fund (HCAF) will cover the loss of the enhanced premium tax credits for households with income under 400% of the Federal Poverty Level (or $128,600 for a family of four), providing up to $68 million in premium relief for working families who enroll in coverage through BeWell in 2026. Federal and state premium assistance will continue to reduce the impact of the rate increases.

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2026. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin coverage. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2026 is December 15, 2025. Consumers who select a plan between December 16, 2025 and January 15, 2026 will have coverage beginning February 1, 2026.

New Mexico Open Enrollment 2026 - Enrollment Summary

Last Refreshed On: December 2, 2025

Officially, they're reporting 75,926 Qualified Health Plan (QHP) enrollments already, which is actually 8% higher than the 70,373 which they ended with during the 2025 Open Enrollment Period (OEP) last January.

HOWEVER...and this is a major caveat...that 75,926 includes all current enrollees being auto-renewed for 2026, which doesn't really count for my purposes. Most state exchanges used to hold off on lumping in the auto-renewals until after the initial December deadline, only reporting current enrollees who actively re-enroll along with new enrollees.

Earlier this afternoon I joined cancer survivor and healthcare reform advocate Laura Packard on her CareTalk podcast to discuss the upcoming expiration of the enhanced ACA tax credits and the Trump Regime's confusing, will-they-or-won't-they non-proposal to maybe, possibly extend them...with a bunch of major caveats attached. Tune in!