I've now analyzed the preliminary average (weighted or, in a few unfortunate cases, unweighted) premium change requests for over 3 dozen states. Of the dozen or so left, the largest states unanalyzed are Georgia, Texas...and Florida.

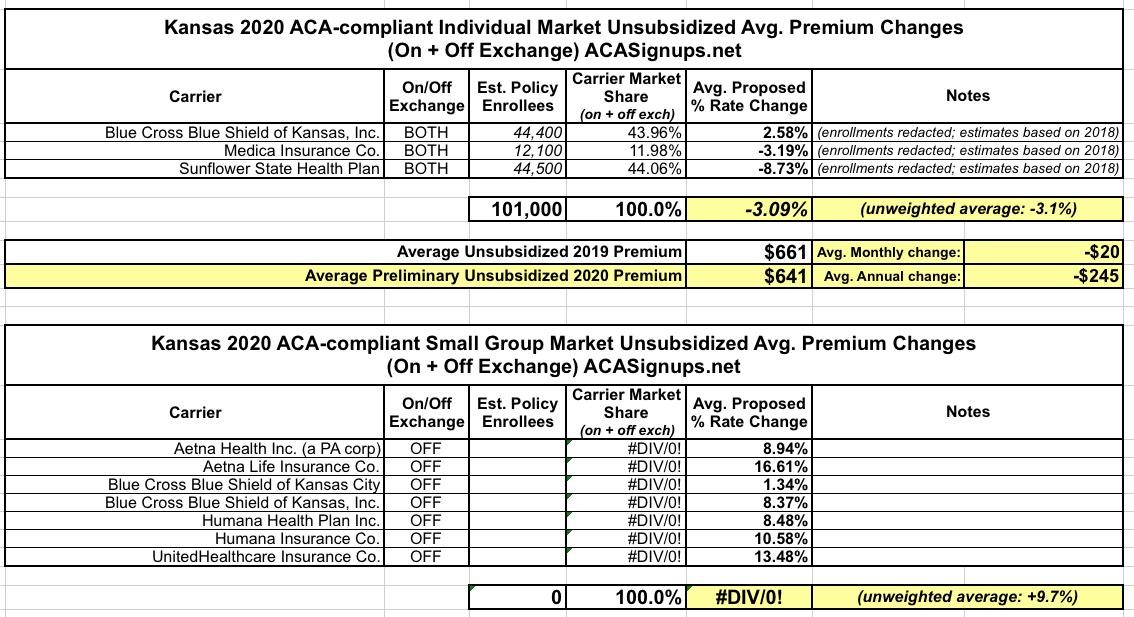

(sigh) Kansas is yet another state where the enrollment data for each of the carriers is redacted on the filing forms this year. To run the weighted average, I'm using last year's estimated enrollment numbers for each, which may have shifted around this year.

Assuming things haven't shfited around too much, unsubsidized Kansans will likely be looking at roughly a 3.1% average premium reduction in 2020...which also happens to be the same as the unweighted average change.

Meanwhile, the small group market is looking at an unweighted average increase of 9.7% statewide.

(sigh) As is common this year, the rate filings for Iowa's Individual and Small Group market are heavily redacted, making it impossible to calculate a weighted average premium rate change. On the Indy market, Medica is reducing their unsubsidized 2020 premiums by 11.3%, while Wellmark is raising theirs by around 4.8%.

Seeing how Wellmark only re-entered the ACA-compliant individual market this year, I'm assuming Medica has the lion's share of enrollees...but who knows? Also, Wellmark is offering two different types of policies; I'm assuming that at most the two combine to be similar to Medica's total. If so, that should mean an average premium reduction of around 3.3%.

For the small group market, I just ran an unweighted average of the 12 different companies offering policies, coming up woth an average 5.4% increase.

There is one interesting tidbit in the Wellmark filing, however: They expect 100% of their 2020 enrollees to do so on-exchange, which basically means that their unsubsidized premiums have gone up so much that they don't expect anyone to be willing to pay full price (off-exchange) for them.

Hawaii only has two carriers participating in the Individual health insurance market. For 2020, they're reducing unsubsidized premiums slightly.

The state's small group market has four carriers; unfortunately, only one of the four (Kaiser Foundation Health Plan) has posted their enrollment data; the other three are redacted. The unweighted average increase on the small group market is a mere 0.8%, however.

The good news is that as of August 2nd, the preliminary 2020 ACA premium rate changes are now available for every state at the RateReview.HealthCare.Gov website.

The bad news is that more carriers appear to be redacting their filings, making it more difficult to run weighted averages based on relative market share. In the case of Illinois, all five carriers on the individual market either redacted or not listed in the summary memos at all.

As a result, all I can do is run an unweighted average, which comes to a 1.4% premium increase statewide. My guess is that Blue Cross Blue Shield likely has the bulk of the market, which means the weighted average is likely just about flat.

For the small group market I didn't even bother trying to get the enrollment data; the unweighted average there is a 4.7% increase.

The good news is that as of August 2nd, the preliminary 2020 ACA premium rate changes are now available for every state at the RateReview.HealthCare.Gov website.

The bad news is that while it does make it extremely easy to look up the average rate changes being requested for every carrier on the Individual and Small Group markets, they appear to have made it somewhat harder to dig up the other key data I need to run weighted averages...namely, the actual enrollment numbers for each, along with other noteworthy items like special circumstances, breakouts of the reasons for the rate changes and so on.

Every year some rate filing forms are redacted, but it seems to be more prevalent for 2020. I don't know if that's something being done by the carriers or at HC.gov's end, but for whatever reason, it's more difficult for me to run weighted averages this year.

Alabama only has two carriers offering Individual Market policies. Unfortunately, the rate filing forms are redacted in some states, so I'm having to patch together bits & pieces of data to try and estimate the weighted average rate changes. In the case of Alabama, the filing for Blue Cross Blue Shield lists 179,500 total individual market enrollees in 2018, but there's no data for 2019...while the filing for Bright Health Insurance (a relative newcomer to the market) doesn't list any enrollment data at all.

I'm assuming that BCBSAL holds a solid 90% of the market and that their total enrollment is around the same year over year. If so, that would give Bright around 20.5K enrollees and make the total Alabama Individual Market around an even 200,000 people. Again, assuming all of this is accurate, that means a weighted average increase of 3.9%, which in turn means unsubsidized enrollees are looking at average premium increases of around $26/month or $312 for the year.

NOTE: This has been corrected from an earlier version.

The floodgates are now officially open for preliminary (not final) 2020 ACA rate filings for both the Individual and Small Group markets. There are several states which only have a single insurance carrier offering policies on the Individual Market, which makes it very easy to calculate the weighted average rate changes...seeing how a single carrier holds 100% of the market.

Among these states are Alaska, Nebraska and Wyoming, where the sole Indy Market carriers are once again Premera BCBS (AK), Medica (NE) and BCBS of Wyoming. Unfortunately, the rate filing forms for all three are partly redacted, making it impossible for me to determine how many total enrollees they have, although I have a pretty good estimate of the on-exchange number as of the end of March for each.

In Alaska, Premera's 2020 rates are virtually unchanged year over year. In Nebraska, Medica expects to reduce rates an average of 5.3%. And in Wyoming, BCBS is only looking to bump up average unsubsidized premiums by 1.6%.

I feel kind of stupid posting this in the aftermath of not one, but two massacres in El Paso, TX and Dayton, OH (at least one of which was a clear case of white nationalist terrorism inspired and encouraged by Donald Trump), but I was bout 80% done with this last night and this is part of my job, so here it is.

Gov. Tony Evers today announced that 2020 rates on Wisconsin’s individual health insurance market will be 3.2 percent lower on a weighted average compared to 2019 rates. This encouraging news further demonstrates that the individual market is stabilizing and Wisconsin residents are able to access more affordable coverage options.

The rate decrease also highlights the positive impact of that the Wisconsin Healthcare Stability Plan (WIHSP), or the state’s reinsurance program, is having on the individual market. WIHSP was fully funded in the recently signed 2019-2021 state biennial budget. Without the WIHSP, rates in the individual market were expected to increase by 9 percent in 2020.

Both evenings of the Detroit Democratic Debates earlier this week started off with half-hour segments on healthcare policy. I meant to do write-ups about both of them but for one reason or another never got around to it until now. Tons of other healthcare wonks have already written their own think pieces by now, so I'm not going to go back and rehash the whole thing at this point.

HOWEVER, there's one quote which made my jaw drop, and it doesn't come from any of the Big Four (Biden, Warren, Harris or Sanders). It comes from Hawaii Representative Tulsi Gabbard...and it didn't even come during the debate itself, but afterwards in the "Spin Room" (they actually call it that) with Anderson Cooper.