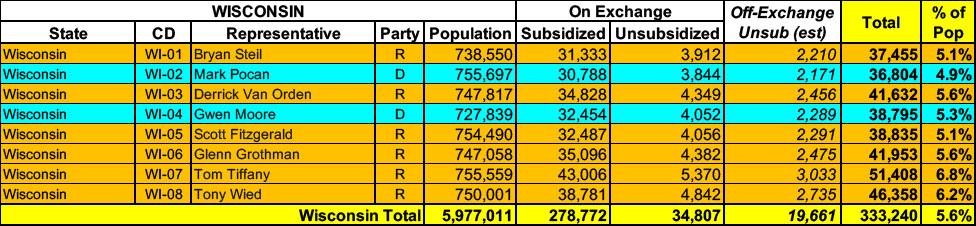

Wisconsin has around ~293,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~19,000 unsubsidized off-exchange enrollees.

West Virginia has ~67,000 residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most).

Colorado has around ~282,000 residents enrolled in ACA exchange plans, 80% of whom are currently subsidized. I estimate they also have another ~39,000 unsubsidized off-exchange enrollees.

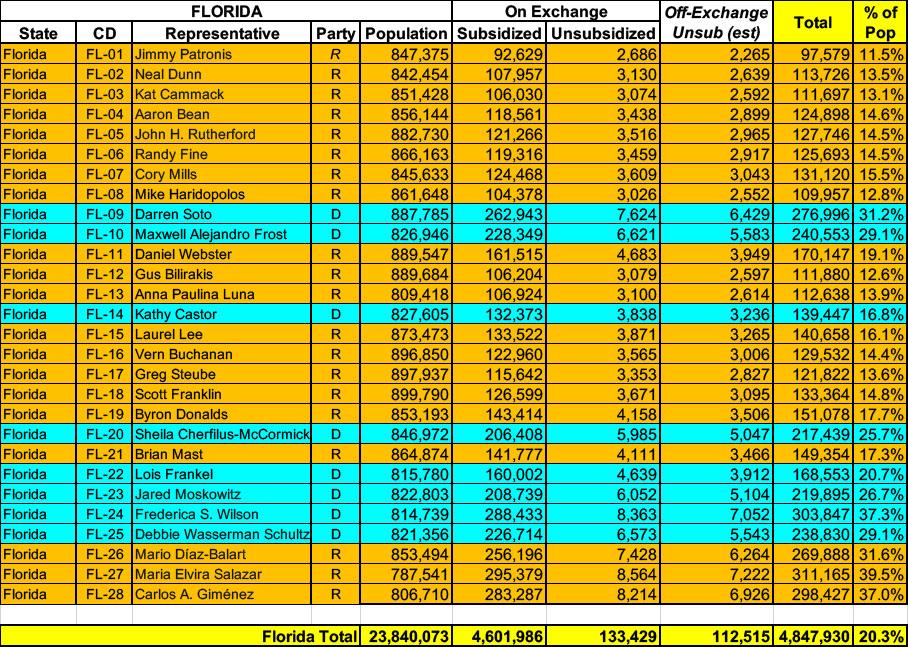

Florida has over ~4.7 MILLION residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. I also estimate they have perhaps ~112,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.8 million people, or a stunning 20.3% of their total population. 1 in 5 Floridians are enrolled in ACA exchange healthcare coverage (assuming CMS's 6.6% net national attrition rate applies to Florida specifically, the actual number of current enrollees is more like 4.5 million, or 19% of the state population).

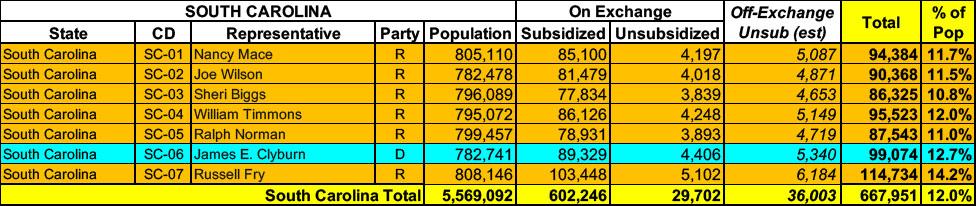

South Carolina has around ~632,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~36,000 unsubsidized off-exchange enrollees.

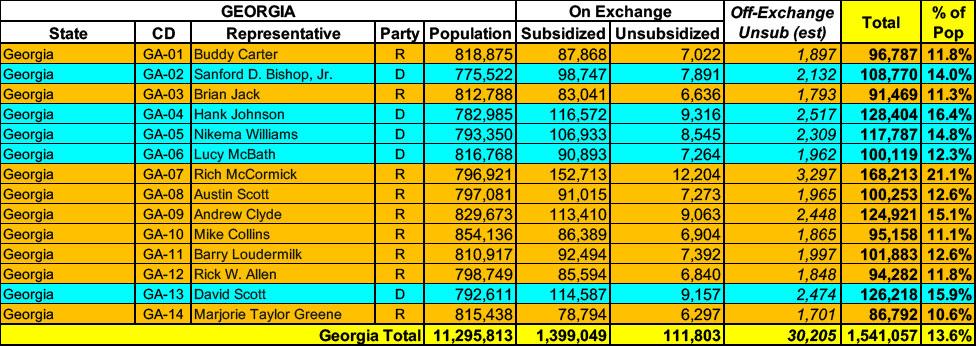

Georgia has around ~1.5 MILLION residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~30,000 unsubsidized off-exchange enrollees.

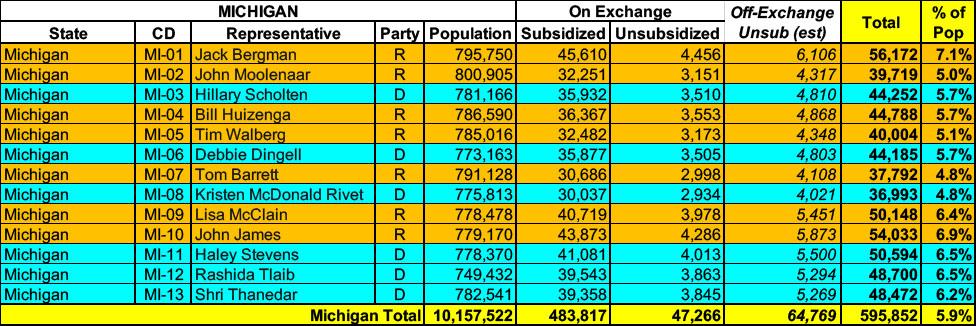

Michigan has around 531,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. I estimate they also have another ~64,000 unsubsidized off-exchange enrollees.

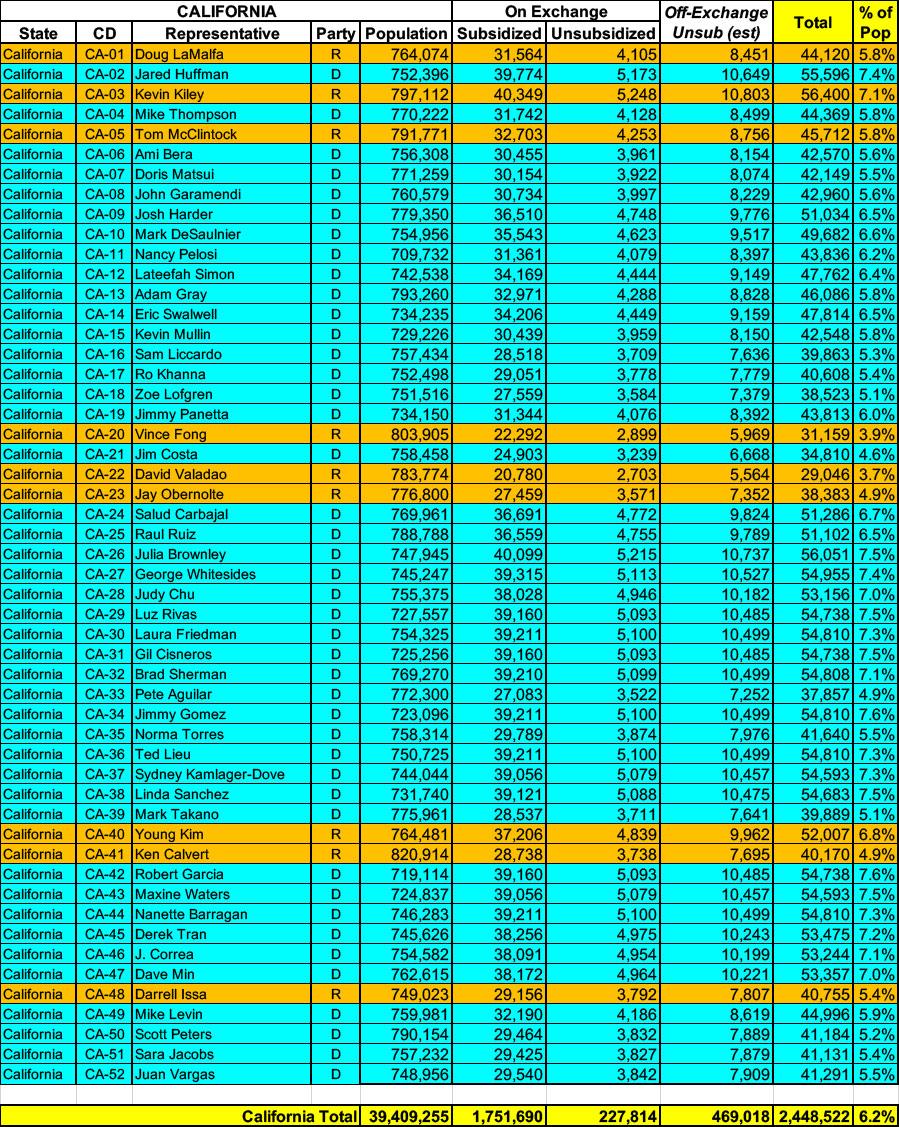

California has ~1.98 MILLION residents enrolled in ACA exchange plans, over 88% of whom are currently subsidized. They also have an estimated ~470,000 off-exchange enrollees. Combined, that's over 2.4 million people, or 6.2% of their total population.

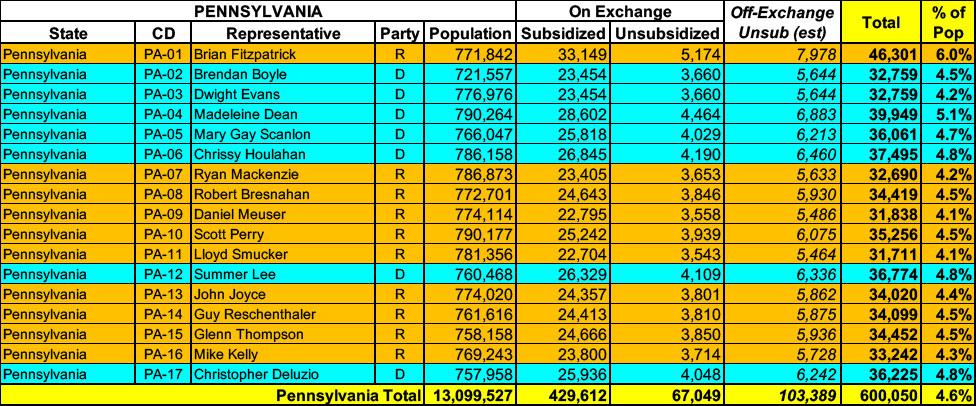

Pennsylvania has around ~496,000 residents enrolled in ACA exchange plans, 87% of whom are currently subsidized. I estimate they also have another ~103,000 unsubsidized off-exchange enrollees.

Idaho has around 117,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. I estimate they also have another ~9,000 unsubsidized off-exchange enrollees, although the actual rate filings (summarized later in this post) put the off-exchange total at a much higher ~47,000.

Combined, that's 6.2 - 8.0% of their total population.

{kind=link}