South Dakota has around ~54,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~3,000 unsubsidized off-exchange enrollees.

Vermont has around ~32,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~2,000 unsubsidized off-exchange enrollees.

Combined, that's ~35,000 people, although the official carrier rate filings claim it's more like 36,000 statewide.

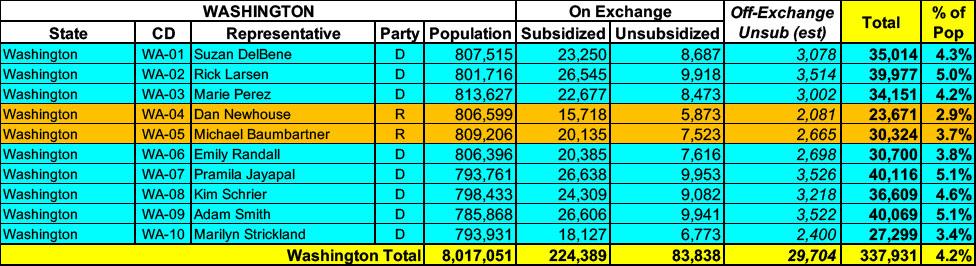

Washington State has around ~308,000 residents enrolled in ACA exchange plans, 73% of whom are currently subsidized. I estimate they also have another ~29,000 unsubsidized off-exchange enrollees.

Utah has around ~421,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~17,000 unsubsidized off-exchange enrollees.

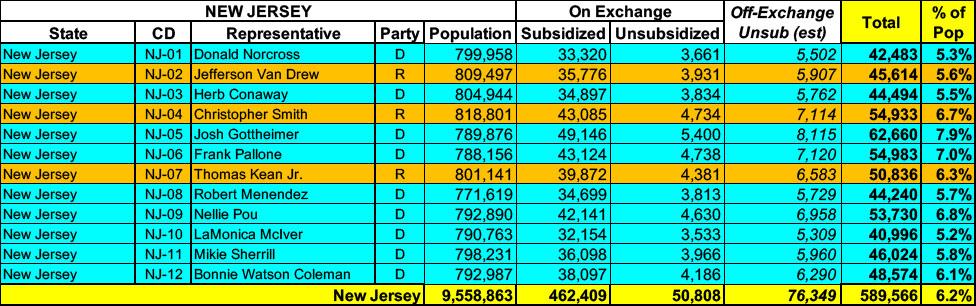

New Jersey has around ~513,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~76,000 unsubsidized off-exchange enrollees.

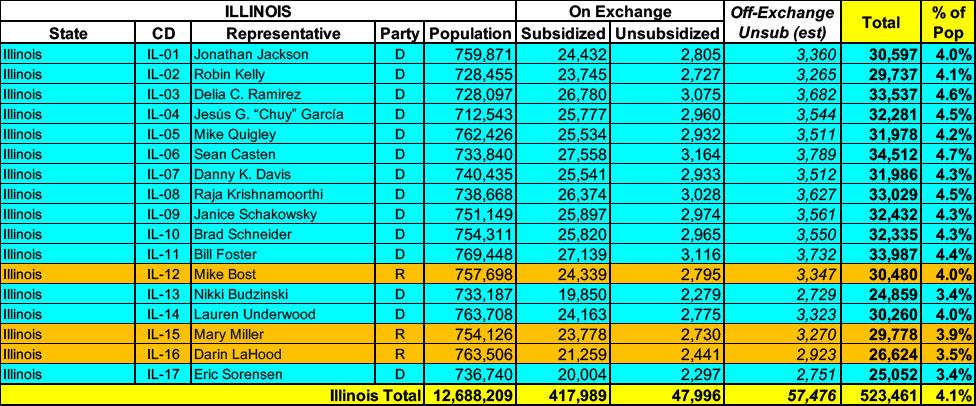

Illinois has around ~466,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~57,000 unsubsidized off-exchange enrollees.

Oregon has around ~140,000 residents enrolled in ACA exchange plans, 80% of whom are currently subsidized. I estimate they also have another ~34,000 unsubsidized off-exchange enrollees.

Oklahoma has around ~293,000 residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~7,000 unsubsidized off-exchange enrollees.

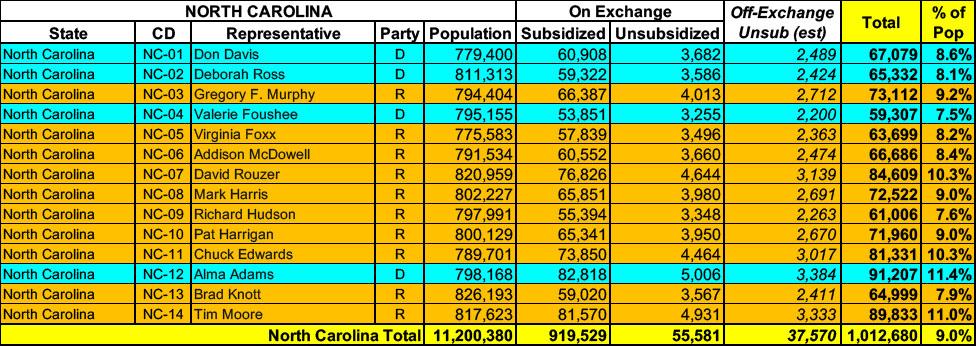

North Carolina has around ~975,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~37,000 unsubsidized off-exchange enrollees.

Montana has around ~77,000 residents enrolled in ACA exchange plans, 89% of whom are currently subsidized. I estimate they also have another ~8,400 unsubsidized off-exchange enrollees.